Web content delivery and security company Akamai (NASDAQ:AKAM) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 7.8% year on year to $987 million. On the other hand, next quarter's revenue guidance of $976.5 million was less impressive, coming in 2.5% below analysts' estimates. It made a GAAP profit of $1.11 per share, improving from its profit of $0.62 per share in the same quarter last year.

Is now the time to buy Akamai? Find out by accessing our full research report, it's free.

Akamai (AKAM) Q1 CY2024 Highlights:

- Revenue: $987 million vs analyst estimates of $989.2 million (small miss)

- EPS: $1.11 vs analyst estimates of $1.00 (11.1% beat)

- Revenue Guidance for Q2 CY2024 is $976.5 million at the midpoint, below analyst estimates of $1.00 billion

- Gross Margin (GAAP): 60%, down from 60.7% in the same quarter last year

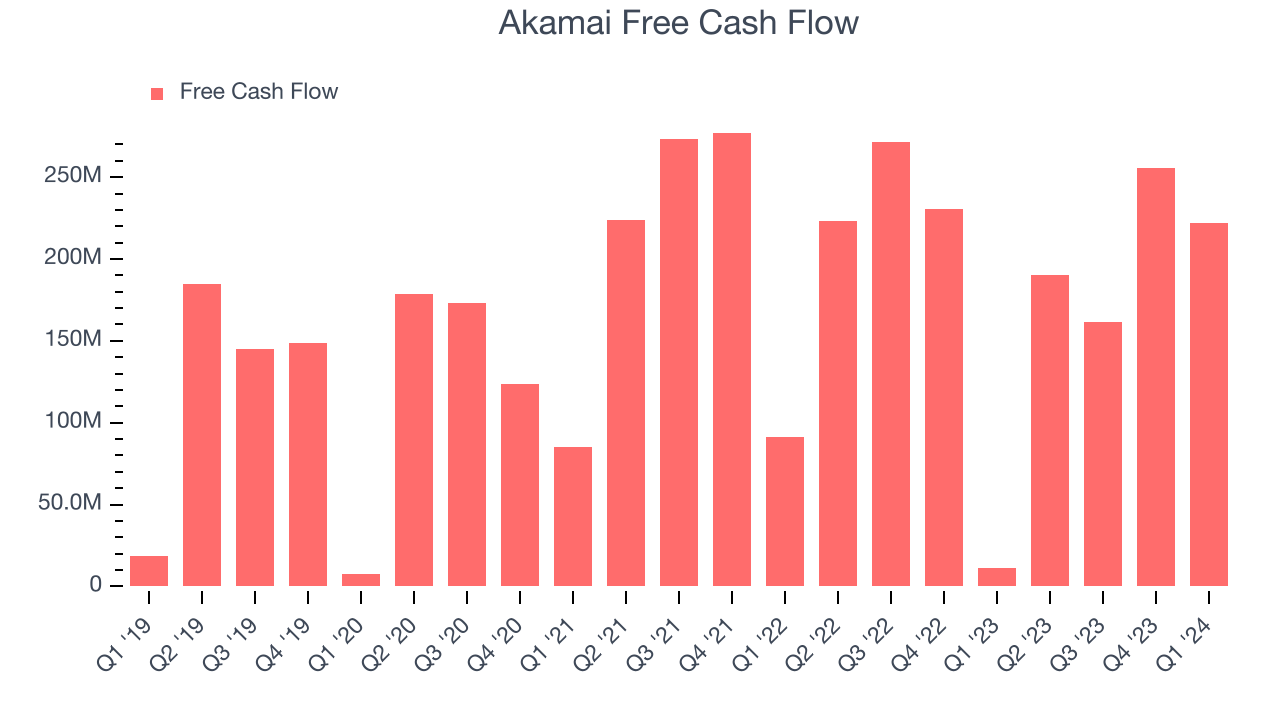

- Free Cash Flow of $221.8 million, down 13.1% from the previous quarter

- Market Capitalization: $15.65 billion

"We are pleased with our continuing execution on our long-term strategy to drive revenue growth in our security and compute solutions," said Dr. Tom Leighton, Akamai's Chief Executive Officer.

Founded in 1999 by two engineers from MIT, Akamai (NASDAQ:AKAM) provides software for organizations to efficiently deliver web content to their customers.

Content Delivery

The amount of content on the internet is exploding, whether it is music, movies and or e-commerce stores. Consumer demand for this content creates network congestion, much like a digital traffic jam which drives demand for specialized content delivery networks (CDN) services that alleviate potential network bottlenecks.

Sales Growth

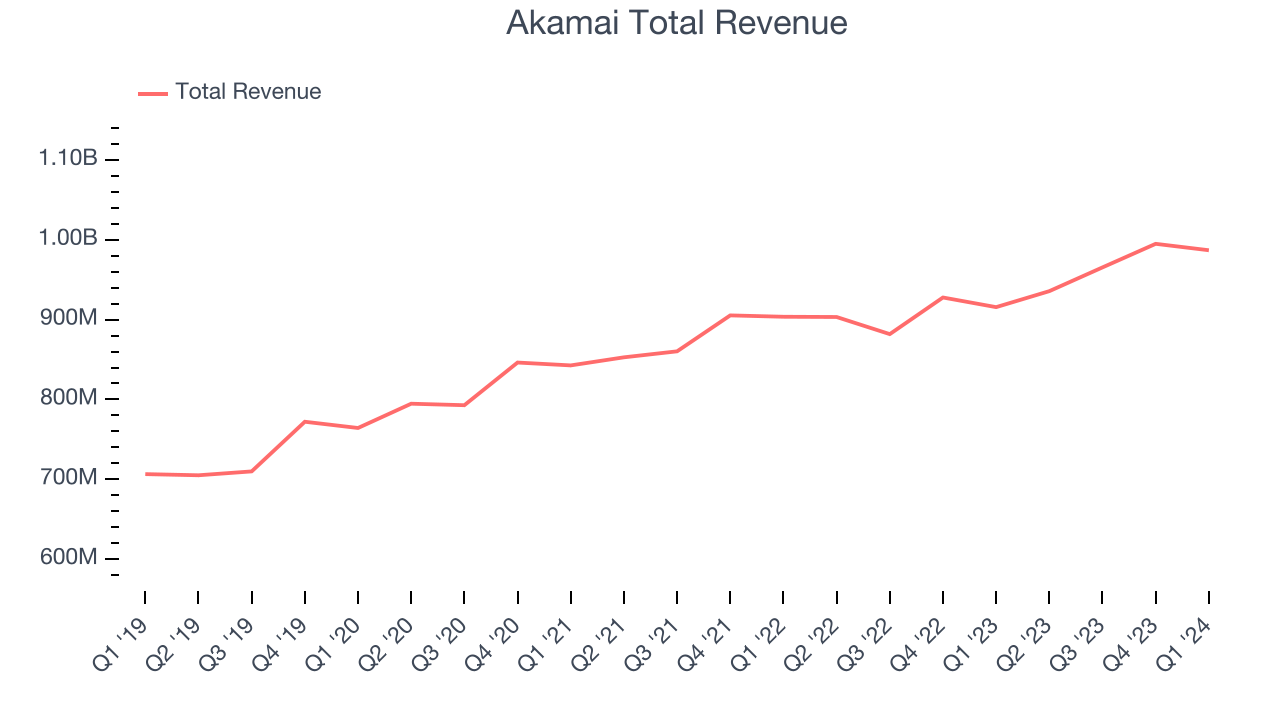

As you can see below, Akamai's revenue growth has been unimpressive over the last three years, growing from $842.7 million in Q1 2021 to $987 million this quarter.

Akamai's quarterly revenue was only up 7.8% year on year, which might disappoint some shareholders. On top of that, the company's revenue actually decreased by $8.05 million in Q1 compared to the $29.53 million increase in Q4 CY2023. This situation is worth monitoring as Akamai's sales have historically followed a seasonal pattern but management is guiding for a further revenue drop in the next quarter.

Next quarter's guidance suggests that Akamai is expecting revenue to grow 4.4% year on year to $976.5 million, improving on the 3.6% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 6.9% over the next 12 months before the earnings results announcement.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Akamai's free cash flow came in at $221.8 million in Q1, up 1,870% year on year.

Akamai has generated $828.9 million in free cash flow over the last 12 months, an impressive 21.3% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from Akamai's Q1 Results

We struggled to find many strong positives in these results. Although its EPS beat Wall Street's estimates, its full-year revenue guidance missed analysts' expectations, sending the stock down. Company outlooks have been the big focus this earnings season. On the bright side, the Board authorized a new three-year, $2.0 billion share repurchase program. Overall, the results could have been better. The company is down 8.9% on the results and currently trades at $93.5 per share.

Akamai may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.