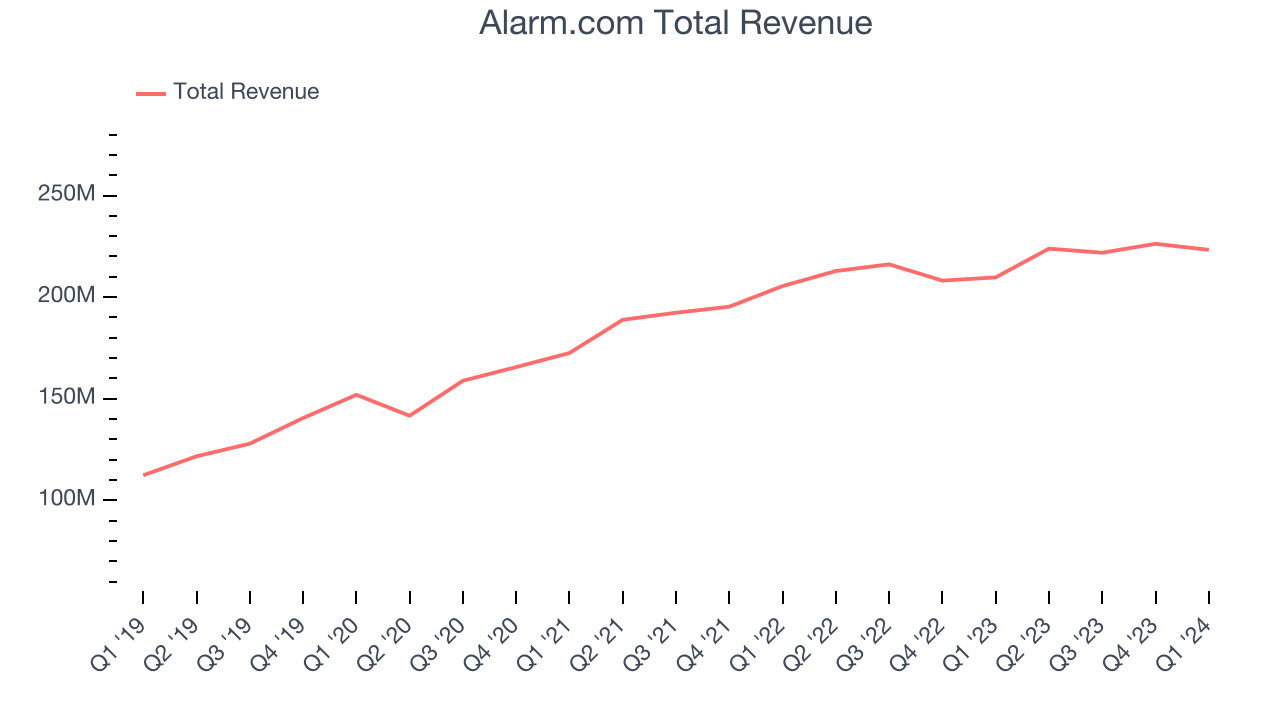

Home security and automation software provider Alarm.com (NASDAQ:ALRM) reported Q1 CY2024 results topping analysts' expectations, with revenue up 6.5% year on year to $223.3 million. The company expects the full year's revenue to be around $922.8 million, in line with analysts' estimates. It made a GAAP profit of $0.44 per share, improving from its profit of $0.28 per share in the same quarter last year.

Is now the time to buy Alarm.com? Find out by accessing our full research report, it's free.

Alarm.com (ALRM) Q1 CY2024 Highlights:

- Revenue: $223.3 million vs analyst estimates of $219.7 million (1.6% beat)

- EPS: $0.44 vs analyst estimates of $0.35 (24.3% beat)

- The company reconfirmed its revenue guidance for the full year of $922.8 million at the midpoint

- Gross Margin (GAAP): 65.7%, up from 63.7% in the same quarter last year

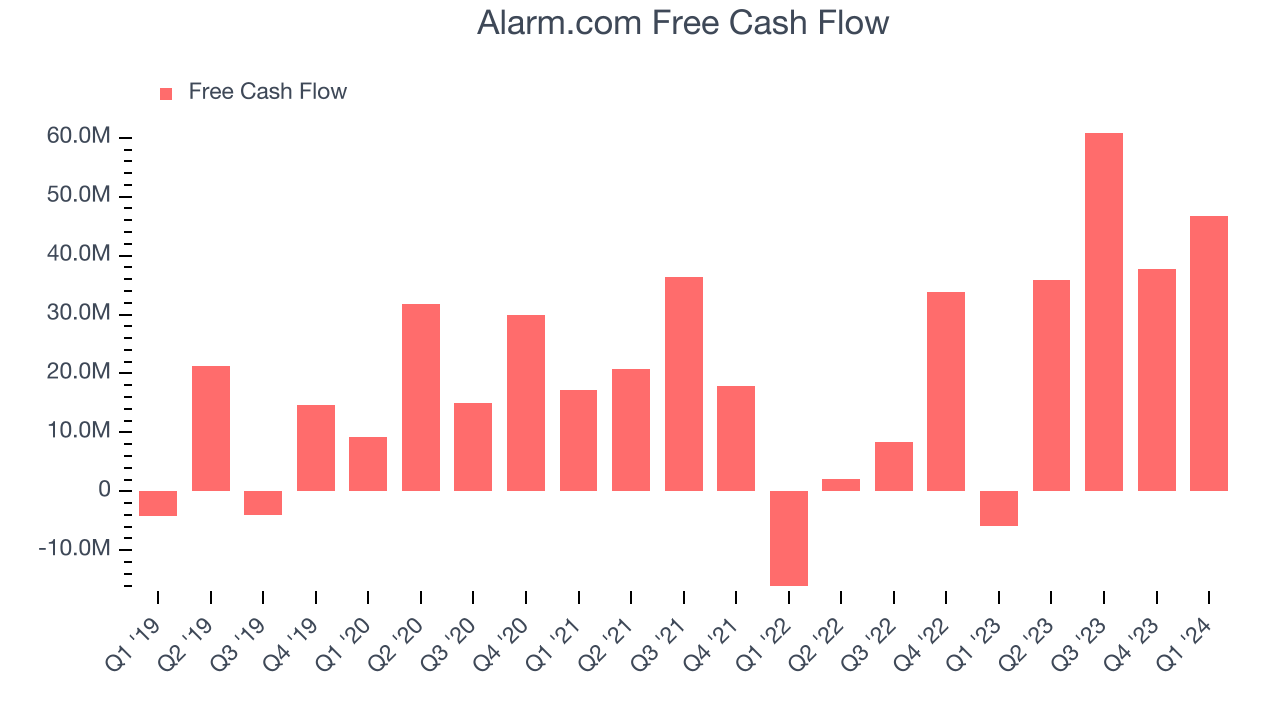

- Free Cash Flow of $46.79 million, up 24.1% from the previous quarter

- Market Capitalization: $3.44 billion

“We are pleased to report solid results and continued momentum across the business in the first quarter,” said Steve Trundle, CEO of Alarm.com.

Founded in 2000 as a business unit within MicroStrategy, Alarm.com (NASDAQ:ALRM) is a software-as-a-service platform that enables users to control their security systems and smart home appliances from a single app.

Vertical Software

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, some have very specific needs. As a result, vertical software, which addresses industry-specific workflows, is growing and fueled by the pressures to improve productivity, whether it be for a life sciences, education, or banking company.

Sales Growth

As you can see below, Alarm.com's revenue growth has been unremarkable over the last three years, growing from $172.5 million in Q1 2021 to $223.3 million this quarter.

Alarm.com's quarterly revenue was only up 6.5% year on year, which might disappoint some shareholders. On top of that, the company's revenue actually decreased by $2.95 million in Q1 compared to the $4.38 million increase in Q4 CY2023.

Looking ahead, analysts covering the company were expecting sales to grow 5.5% over the next 12 months before the earnings results announcement.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Alarm.com's free cash flow came in at $46.79 million in Q1, turning positive over the last year.

Alarm.com has generated $181.2 million in free cash flow over the last 12 months, an impressive 20.2% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from Alarm.com's Q1 Results

It was good to see Alarm.com beat analysts' billings, revenue, and EPS expectations this quarter. We were also glad its gross margin improved. On the other hand, its full-year revenue guidance missed Wall Street's estimates. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 1.9% after reporting and currently trades at $69.99 per share.

So should you invest in Alarm.com right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.