Home security and automation software provider Alarm.com (NASDAQ:ALRM) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 8.7% year on year to $226.2 million. The company's outlook for the full year was also close to analysts' estimates with revenue guided to $923 million at the midpoint. It made a GAAP profit of $0.58 per share, improving from its profit of $0.52 per share in the same quarter last year.

Alarm.com (ALRM) Q4 FY2023 Highlights:

- Revenue: $226.2 million vs analyst estimates of $224.9 million (small beat)

- EPS: $0.58 vs analyst estimates of $0.21 (big beat)

- Management's revenue guidance for the upcoming financial year 2024 is $923 million at the midpoint, in line with analyst expectations and implying 4.7% growth (vs 4.7% in FY2023)

- Management's adjusted EBITDA guidance for the upcoming financial year 2024 is $162 million at the midpoint, above analyst expectations of $151 million

- Free Cash Flow of $37.7 million, down 38.1% from the previous quarter

- Gross Margin (GAAP): 64.1%, up from 61.8% in the same quarter last year

- Market Capitalization: $3.45 billion

Founded in 2000 as a business unit within MicroStrategy, Alarm.com (NASDAQ:ALRM) is a software-as-a-service platform that enables users to control their security systems and smart home appliances from a single app.

Alarm.com's platform is a response to the proliferation of smart or connected consumer devices and electronics. The company's current flagship product is its cloud-based platform that enables users to control a range of connected devices such as door locks, thermostats, and security cameras through a single digital interface. After leaving home to head to the office, for example, a homeowner can lower the blinds, turn down the heat, and monitor external cameras to see that packages have been delivered.

The key customers of Alarm.com are homeowners, property managers, and business owners who are looking for a reliable and secure solution to manage their properties remotely. Alarm.com generates revenue primarily through service provider partners, who are experts at selling, installing, and supporting the company’s products. In turn, these service provider partners pay Alarm.com monthly fees. For example, Alarm.com partners with leading security companies such as ADT, which sells and installs Alarm.com’s hardware. ADT also sells Alarm.com’s software solutions and may cross-sell ADT products and services as well. Alarm.com in turn receives recurring payments from ADT.

Vertical Software

Software is eating the world, and while a large number of solutions such as project management or video conferencing software can be useful to a wide array of industries, some have very specific needs. As a result, vertical software, which addresses industry-specific workflows, is growing and fueled by the pressures to improve productivity, whether it be for a life sciences, education, or banking company.

Competitors in home automation and security services include ADT (NYSE:ADT) and private companies Vivint and SimpliSafe.Sales Growth

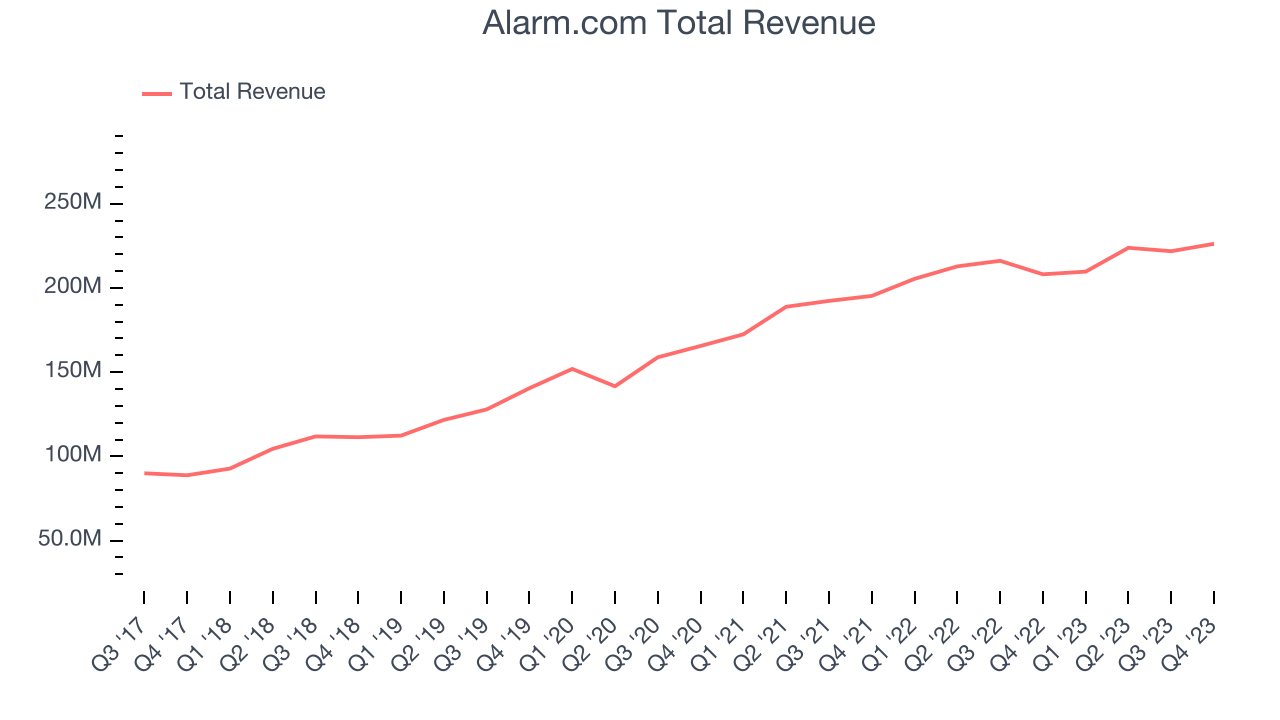

As you can see below, Alarm.com's revenue growth has been unremarkable over the last two years, growing from $195.3 million in Q4 FY2021 to $226.2 million this quarter.

Alarm.com's quarterly revenue was only up 8.7% year on year, which might disappoint some shareholders. However, its revenue increased $4.38 million quarter on quarter, a strong improvement from the $2.02 million decrease in Q3 2023. This is a sign of acceleration of growth and very nice to see indeed.

For the upcoming financial year, management expects revenue to be $923 million at the midpoint, growing 4.7% year on year compared to the 4.6% increase in FY2023.

Profitability

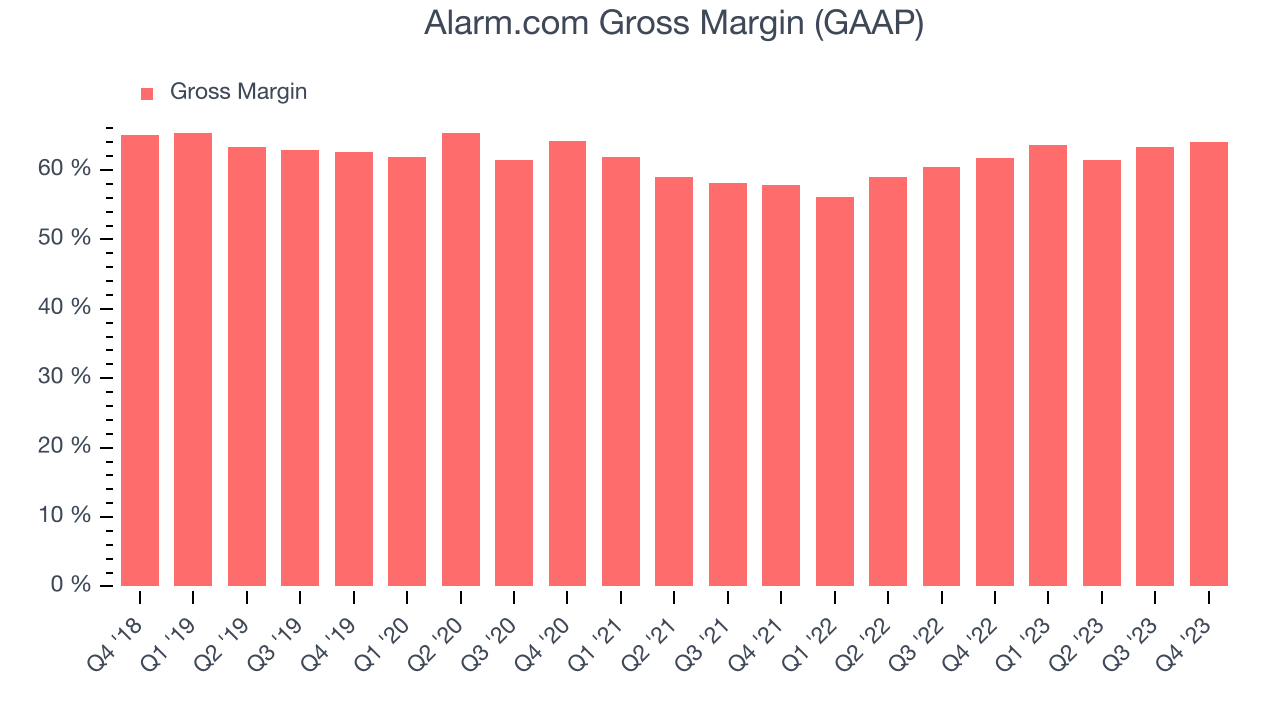

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Alarm.com's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 64.1% in Q4.

That means that for every $1 in revenue the company had $0.64 left to spend on developing new products, sales and marketing, and general administrative overhead. While its gross margin has improved significantly since the previous quarter, Alarm.com's gross margin is still poor for a SaaS business. It's vital that the company continues to improve this key metric.

Cash Is King

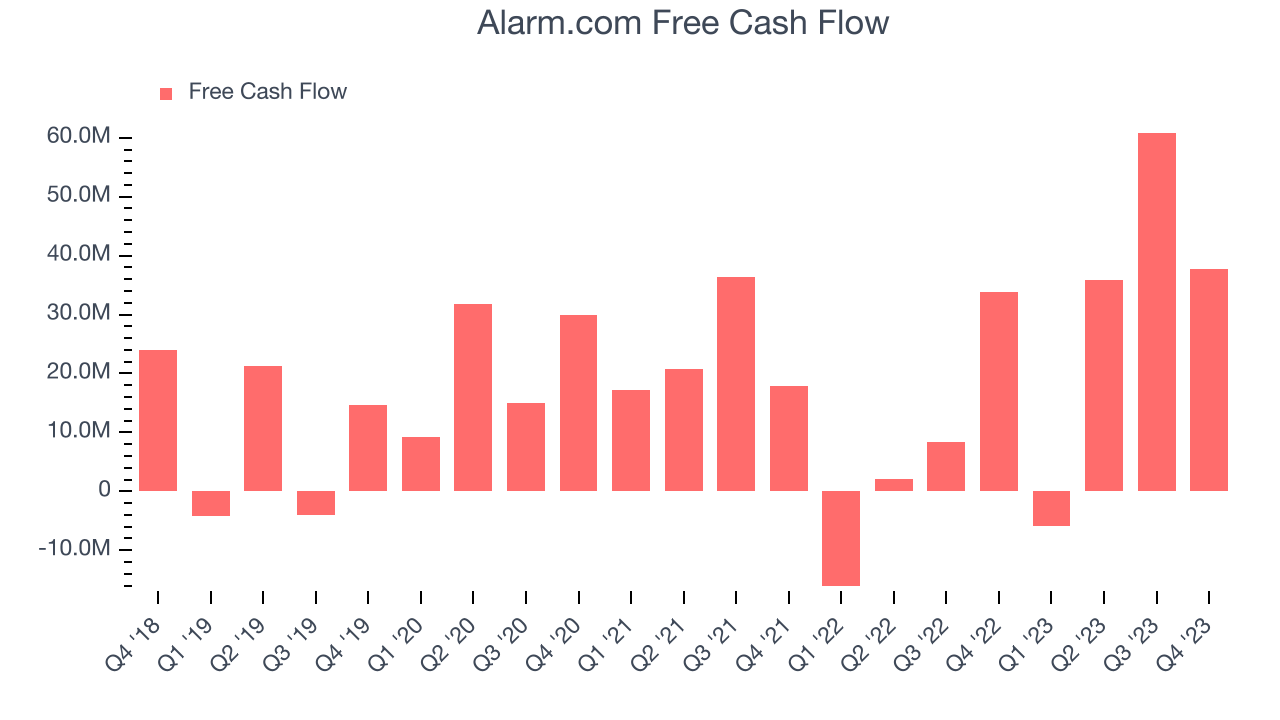

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Alarm.com's free cash flow came in at $37.7 million in Q4, up 11.3% year on year.

Alarm.com has generated $128.4 million in free cash flow over the last 12 months, a decent 14.6% of revenue. This FCF margin stems from its asset-lite business model and gives it a decent amount of cash to reinvest in its business.

Key Takeaways from Alarm.com's Q4 Results

This was a solid quarter, with revenue and profits beating expectations. Looking forward, while revenue for next quarter is in line with expectations, adjusted EBITDA guidance was better. Zooming out, we think that the company is staying on target. The stock is up 3.3% after reporting and currently trades at $72.1 per share.

Is Now The Time?

When considering an investment in Alarm.com, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in case of Alarm.com, we'll be cheering from the sidelines. Its , and analysts expect growth to deteriorate from here. And while its very efficient customer acquisition hints at the potential for strong profitability, unfortunately, its gross margins show its business model is much less lucrative than the best software businesses.

Alarm.com's price-to-sales ratio based on the next 12 months is 4.1x, suggesting that the market does have lower expectations of the business, relative to the high growth tech stocks. While we have no doubt one can find things to like about the company, we think there might be better opportunities in the market and at the moment don't see many reasons to get involved.

Wall Street analysts covering the company had a one-year price target of $68.57 per share right before these results (compared to the current share price of $72.10), implying they didn't see much short-term potential in the Alarm.com.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.