Mobile app advertising platform AppLovin (NASDAQ: APP) fell short of analyst expectations in Q2 FY2022 quarter, with revenue up 16% year on year to $776.2 million. AppLovin made a GAAP loss of $21.7 million, down on its profit of $14.3 million, in the same quarter last year.

Is now the time to buy AppLovin? Access our full analysis of the earnings results here, it's free.

AppLovin (APP) Q2 FY2022 Highlights:

- Revenue: $776.2 million vs analyst estimates of $827.7 million (6.22% miss)

- EPS (GAAP): -$0.06

- Free cash flow of $104 million, up from negative free cash flow of $32 million in previous quarter

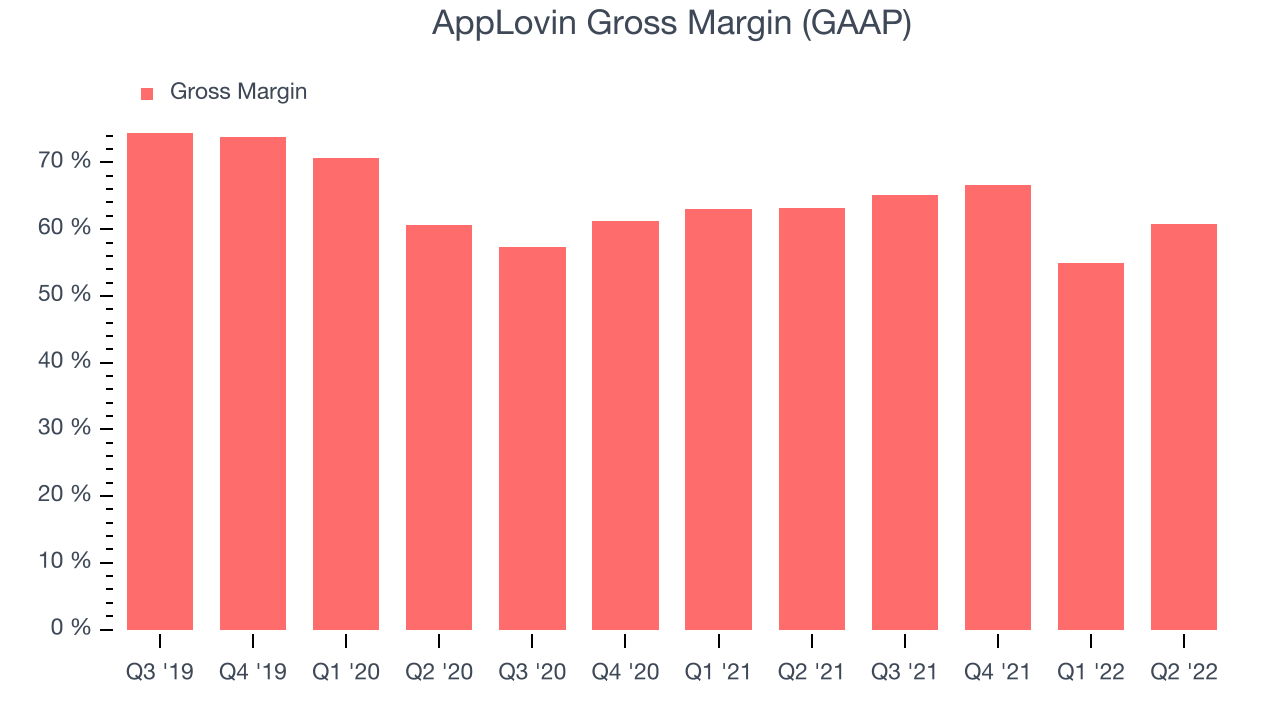

- Gross Margin (GAAP): 60.8%, down from 63.2% same quarter last year

- AppLovin made an offer to buy Unity Software in a $17.54 billion all-stock deal

Co-founded by Adam Foroughi who was frustrated with not being able to find a good solution to market his own dating app, AppLovin (NASDAQ:APP) is a provider of marketing and monetization tools for mobile app developers and also operates a portfolio of mobile games.

The digital advertising market is large, growing and becoming more diverse, both in terms of audiences and media. This as a result drives a growing need for a software that enables advertisers to use data to automate and optimize ad placements.

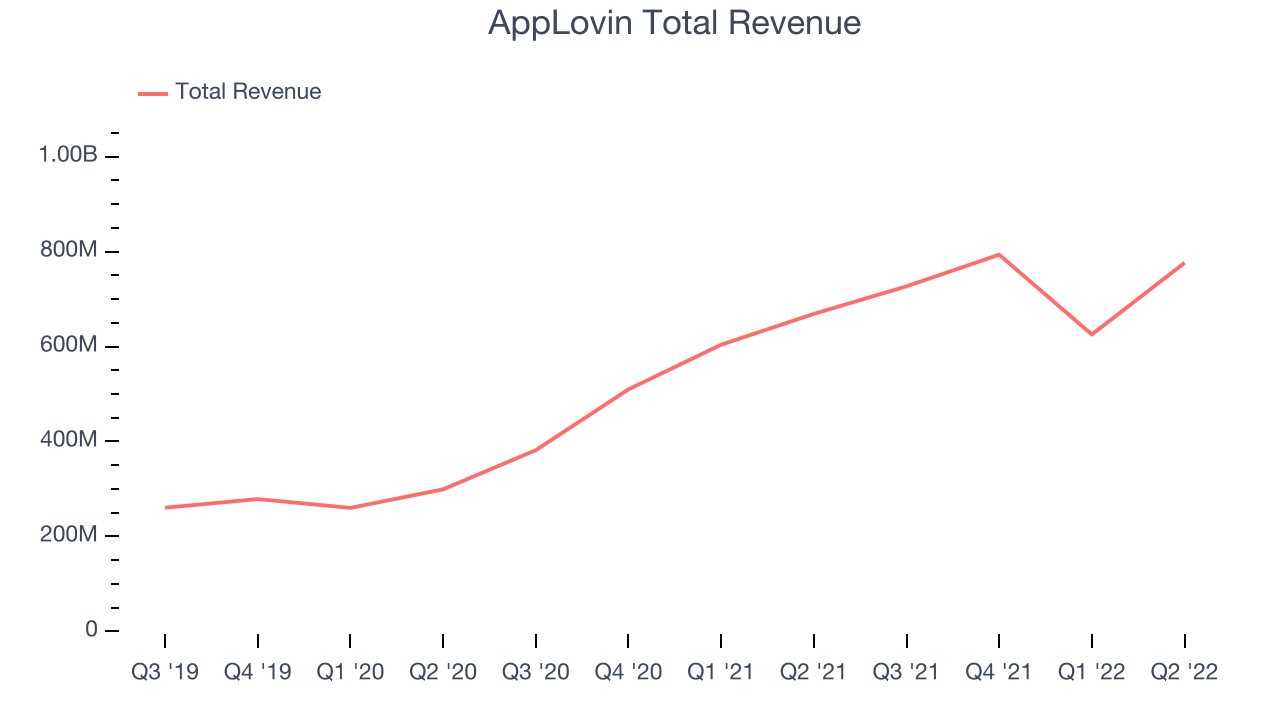

Sales Growth

As you can see below, AppLovin's revenue growth has been impressive over the last year, growing from quarterly revenue of $668.8 million, to $776.2 million.

Even though AppLovin fell short of revenue estimates, its quarterly revenue growth was still up 16% year on year. On top of that, revenue increased $150.8 million quarter on quarter, a strong improvement on the $168 million decrease in Q1 2022, and a sign of acceleration of growth, which is very nice to see indeed.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 27% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. AppLovin's gross profit margin, an important metric measuring how much money there is left after paying for servers, licenses, technical support and other necessary running expenses was at 60.8% in Q2.

That means that for every $1 in revenue the company had $0.60 left to spend on developing new products, marketing & sales and the general administrative overhead. While it improved significantly from the previous quarter this would still be considered a low gross margin for a SaaS company and we would like to see the improvements continue.

Key Takeaways from AppLovin's Q2 Results

With a market capitalization of $13.6 billion, more than $951.5 million in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

We were very impressed by the strong improvements in AppLovin’s gross margin this quarter. That feature of these results really stood out as a positive. On the other hand, it was unfortunate to see that AppLovin missed analysts' revenue expectations. Overall, this quarter's results were not the best we've seen from AppLovin. The company is down 12.3% on the results and currently trades at $35.46 per share.

AppLovin may have had a tough quarter, but does that actually create an opportunity to invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.