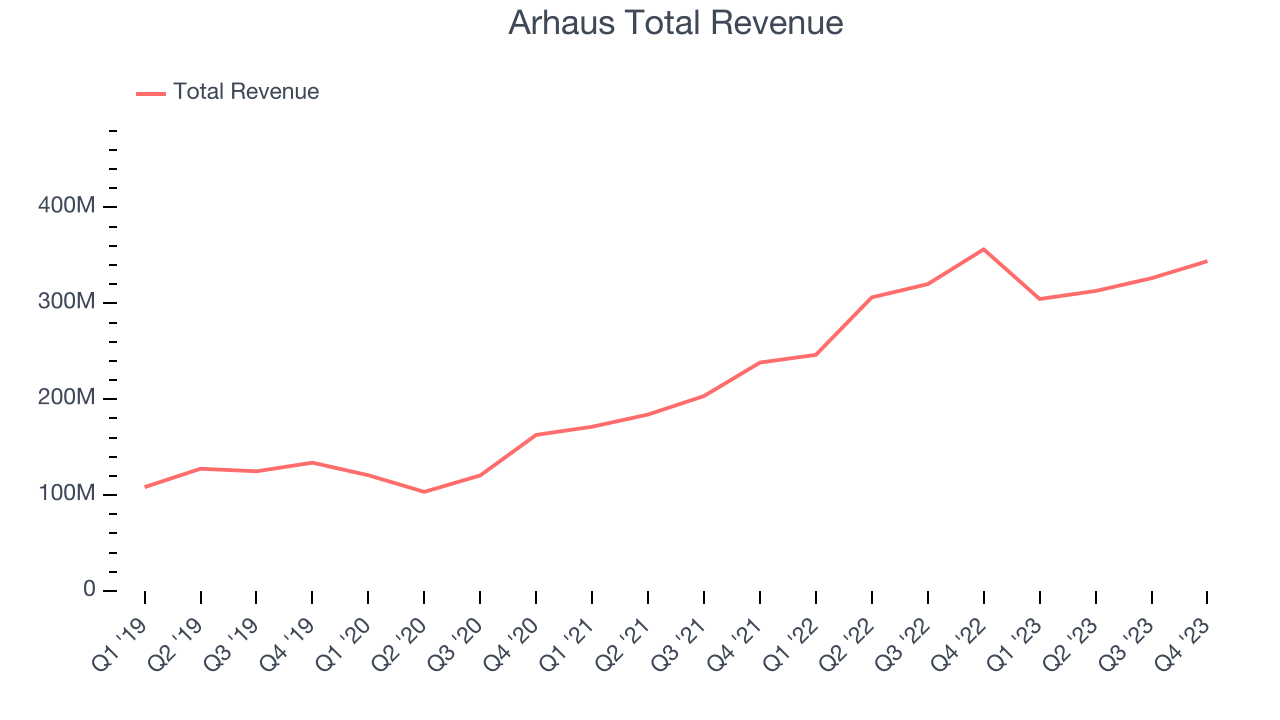

Luxury furniture retailer Arhaus (NASDAQ:ARHS) reported Q4 FY2023 results beating Wall Street analysts' expectations, with revenue down 3.5% year on year to $344 million. Revenue guidance for the full year also exceeded analysts' estimates but next quarter's guidance of $265 million was less impressive, coming in 9.4% below expectations. It made a non-GAAP profit of $0.22 per share, down from its profit of $0.34 per share in the same quarter last year.

Arhaus (ARHS) Q4 FY2023 Highlights:

- Revenue: $344 million vs analyst estimates of $335.5 million (2.5% beat)

- EPS (non-GAAP): $0.22 vs analyst estimates of $0.16 (34.1% beat)

- Revenue Guidance for Q1 2024 is $265 million at the midpoint, below analyst estimates of $292.3 million

- Management's revenue guidance for the upcoming financial year 2024 is $1.35 billion at the midpoint, beating analyst estimates by 1.8% and implying 4.8% growth (vs 6.1% in FY2023)

- Free Cash Flow was -$13.82 million, down from $509,000 in the same quarter last year

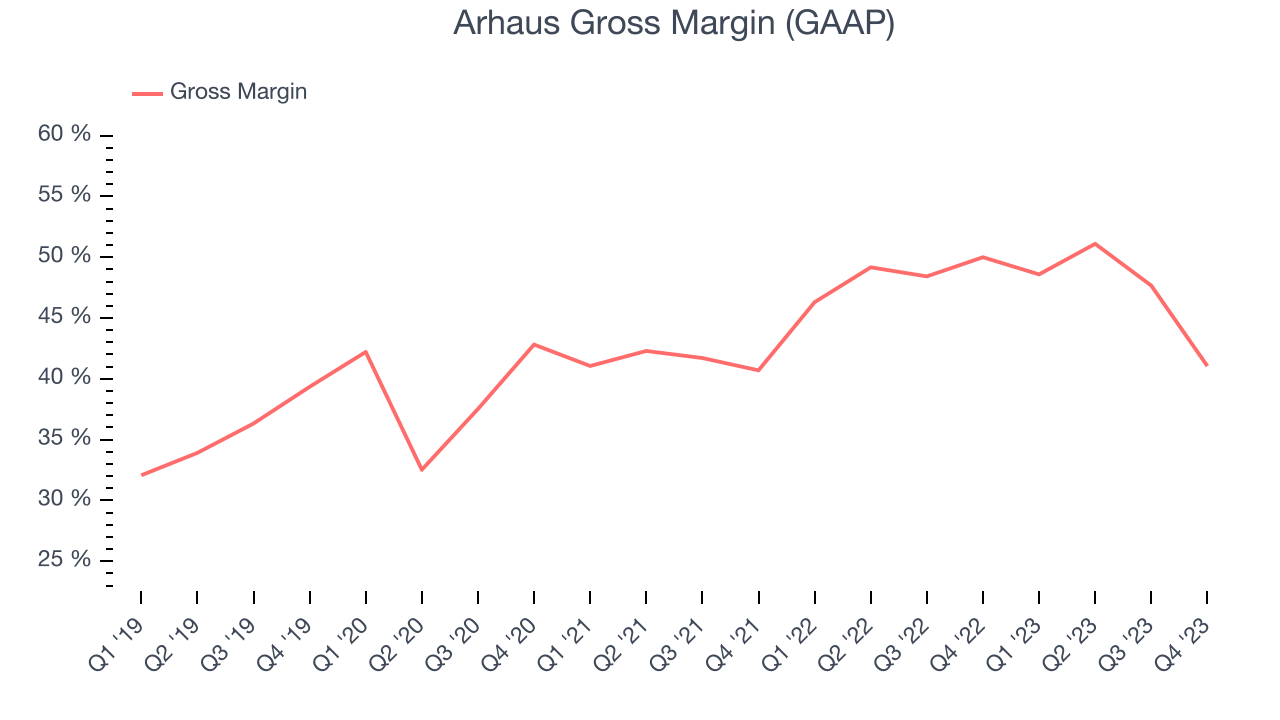

- Gross Margin (GAAP): 41%, down from 50% in the same quarter last year

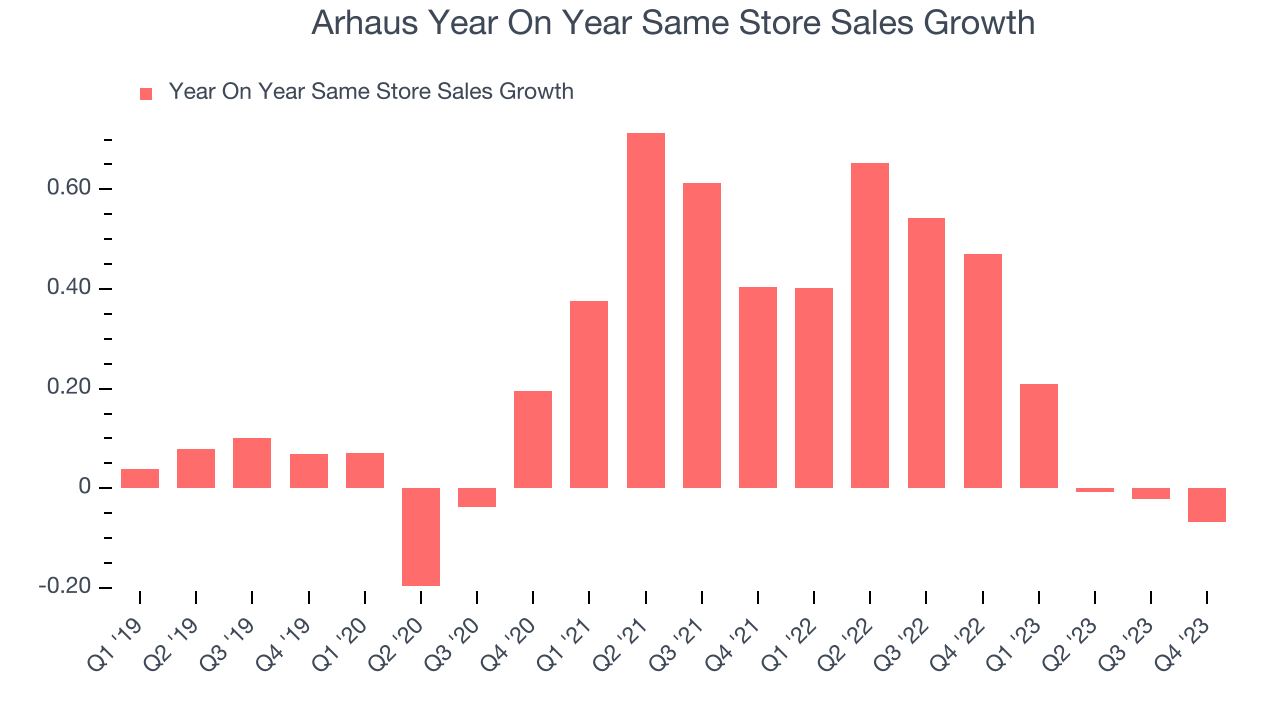

- Same-Store Sales were down 6.8% year on year

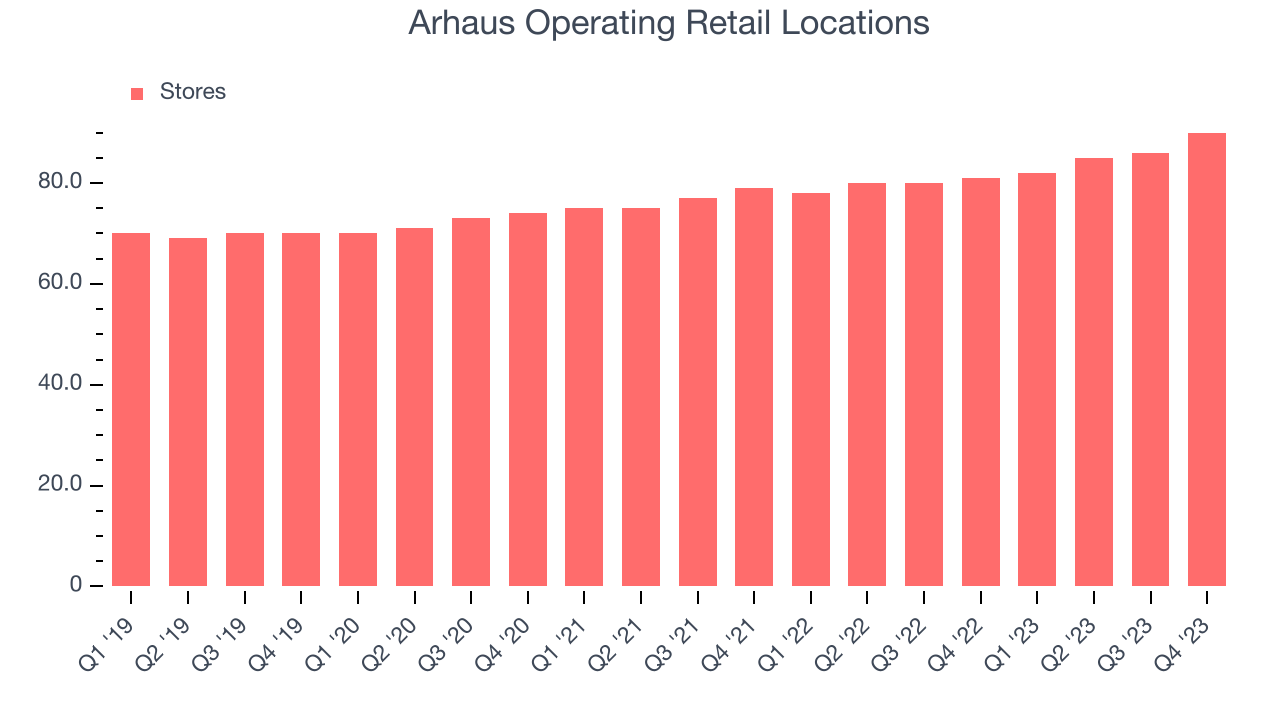

- Store Locations: 90 at quarter end, increasing by 9 over the last 12 months

- Market Capitalization: $1.80 billion

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ:ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

The Arhaus core customer is affluent and values quality and a style that is not cookie-cutter. Arhaus’s aesthetic can be described as having rich, warm finishes and textures, such as handcrafted woodwork, natural stone, and organic fabrics. Some products are hand-crafted or one-of-a-kind, which speaks to customers who value uniqueness. The company also offers a range of eco-friendly products such as reclaimed wood products and other recycled materials for the customer who is especially concerned about the environment.

The average Arhaus store is around 20,000 square feet in size and is typically located in upscale shopping centers or lifestyle centers alongside other luxury brands. The stores are designed to feel like a home, with cozy seating areas and a relaxed, inviting atmosphere where customers are free to lounge and experience the products directly. Arhaus also has an e-commerce platform, launched in 2005, allowing customers to shop online and have products delivered directly to their homes. The company’s online platform also offers virtual design consultations.

Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Competitors offering higher-end furniture include public companies Restoration Hardware (NYSE:RH), MillerKnoll (NASDAQ:MLKN), and Williams Sonoma (NYSE:WSM). Private company West Elm is also a competitor.Sales Growth

Arhaus is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 27% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was incredible as it added more brick-and-mortar locations and increased sales at existing, established stores.

This quarter, Arhaus's revenue fell 3.5% year on year to $344 million but beat Wall Street's estimates by 2.5%. The company is guiding for a 13% year-on-year revenue decline next quarter to $265 million, a reversal from the 23.7% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 2.2% over the next 12 months, an acceleration from this quarter.

Number of Stores

When a retailer like Arhaus is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, Arhaus's store count increased by 9 locations, or 11.1%, to 90 total retail locations in the most recently reported quarter.

Over the last two years, the company has opened new stores quickly and averaged 5.9% annual growth in new locations, meaningfully higher than other consumer retail businesses. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Arhaus has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing stores. On average, the company has posted exceptional year-on-year same-store sales growth of 27.3%. This performance suggests that its steady rollout of new stores could be beneficial for shareholders. When a company has strong demand, more locations should help it reach more customers seeking its products.

In the latest quarter, Arhaus's same-store sales fell 6.8% year on year. This decline was a reversal from the 47% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Gross Margin & Pricing Power

Arhaus has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent to stay one step ahead of the competition. As you can see below, it's averaged an exceptional 47.8% gross margin over the last two years. This means the company makes $0.48 for every $1 in revenue before accounting for its operating expenses.

Arhaus produced a 41% gross profit margin in Q4, marking a 9 percentage point decrease from 50% in the same quarter last year. Although the company could've performed better, we care more about its long-term trends rather than just one quarter. Additionally, a retailer's gross margin can often change due to factors outside its control, such as product discounting and dynamic input costs (think distribution and freight expenses to move goods). We'll keep a close eye on this.

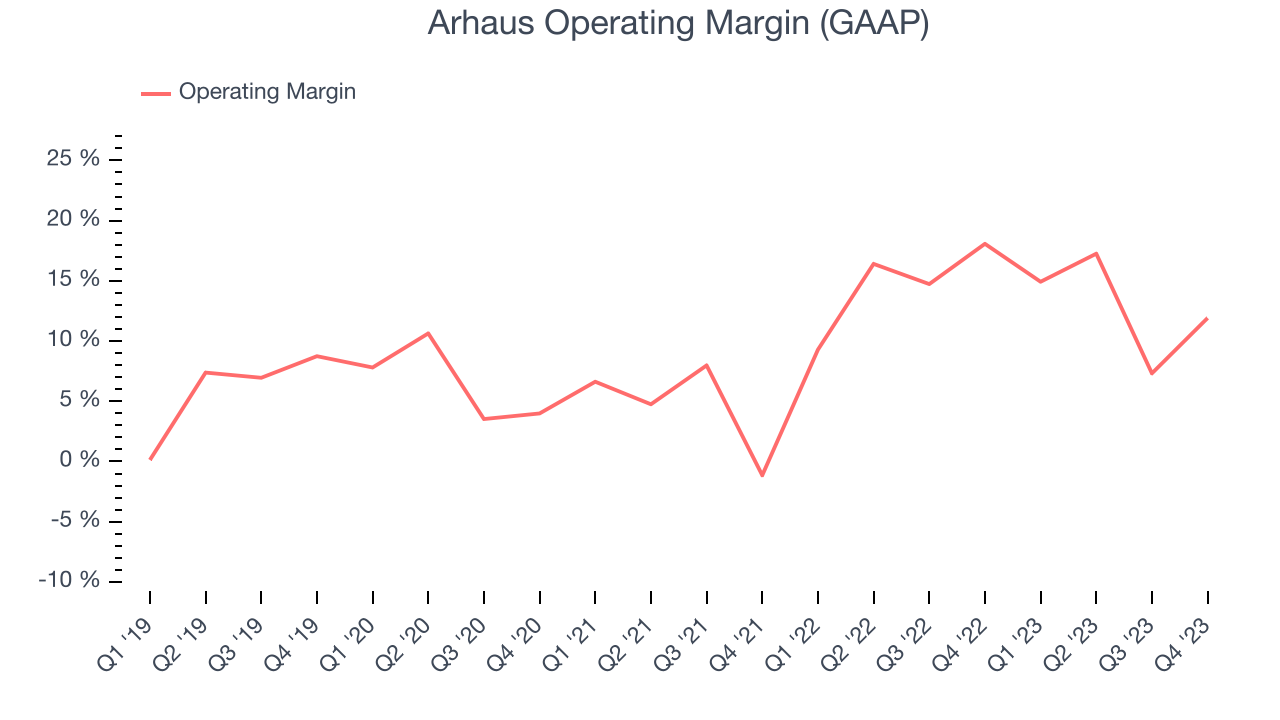

Operating Margin

Operating margin is an important measure of profitability for retailers as it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

In Q4, Arhaus generated an operating profit margin of 11.9%, down 6.2 percentage points year on year. This reduction was driven by weaker pricing power, as indicated by the company's larger drop in gross margin.

Zooming out, Arhaus has exercised operational efficiency over the last eight quarters. The company has demonstrated it can be wildly profitable for a consumer retail business, boasting an average operating margin of 13.9%. However, Arhaus's margin has slightly declined by 2.3 percentage points year on year (on average). This shows the company has faced some small speed bumps along the way.

Zooming out, Arhaus has exercised operational efficiency over the last eight quarters. The company has demonstrated it can be wildly profitable for a consumer retail business, boasting an average operating margin of 13.9%. However, Arhaus's margin has slightly declined by 2.3 percentage points year on year (on average). This shows the company has faced some small speed bumps along the way. EPS

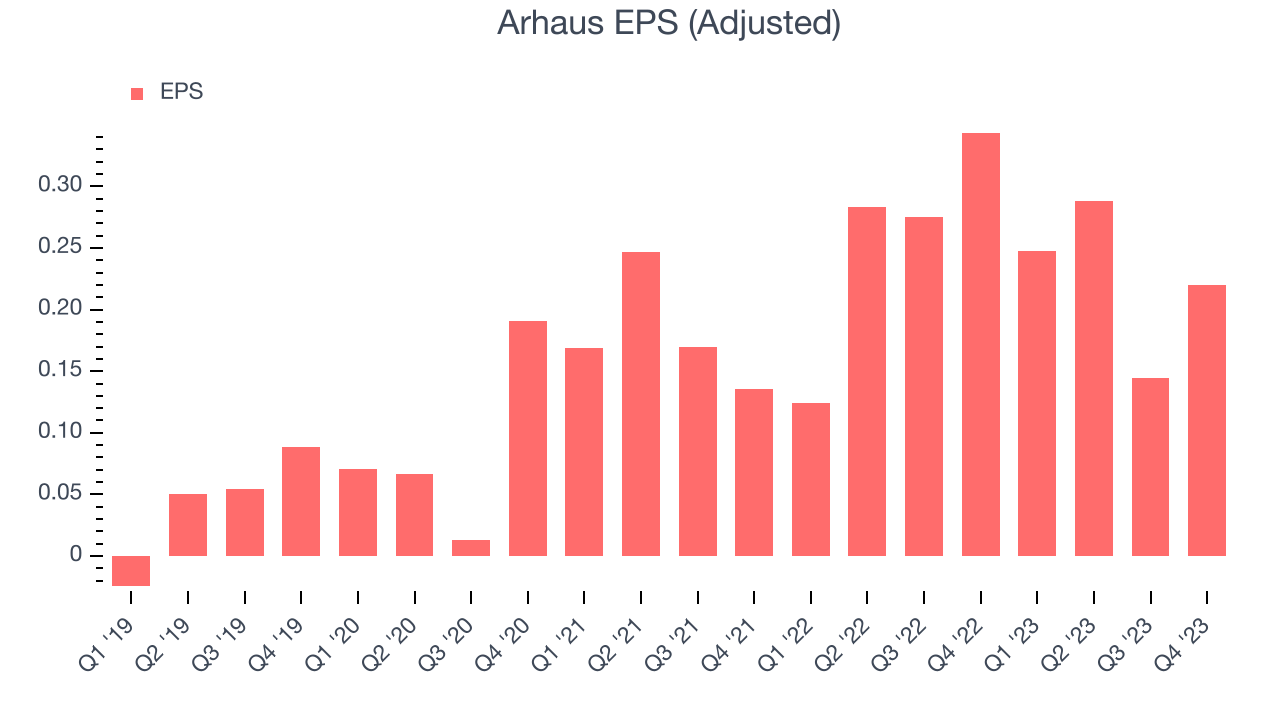

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q4, Arhaus reported EPS at $0.22, down from $0.34 in the same quarter a year ago. This print beat Wall Street's estimates by 34.1%.

Between FY2019 and FY2023, Arhaus's adjusted diluted EPS grew 433%, translating into an astounding 51.9% compounded annual growth rate. This growth is materially higher than its revenue growth over the same period, showing that Arhaus has excelled in managing its expenses.

Over the next 12 months, however, Wall Street is projecting an average 18.5% year-on-year decline in EPS.

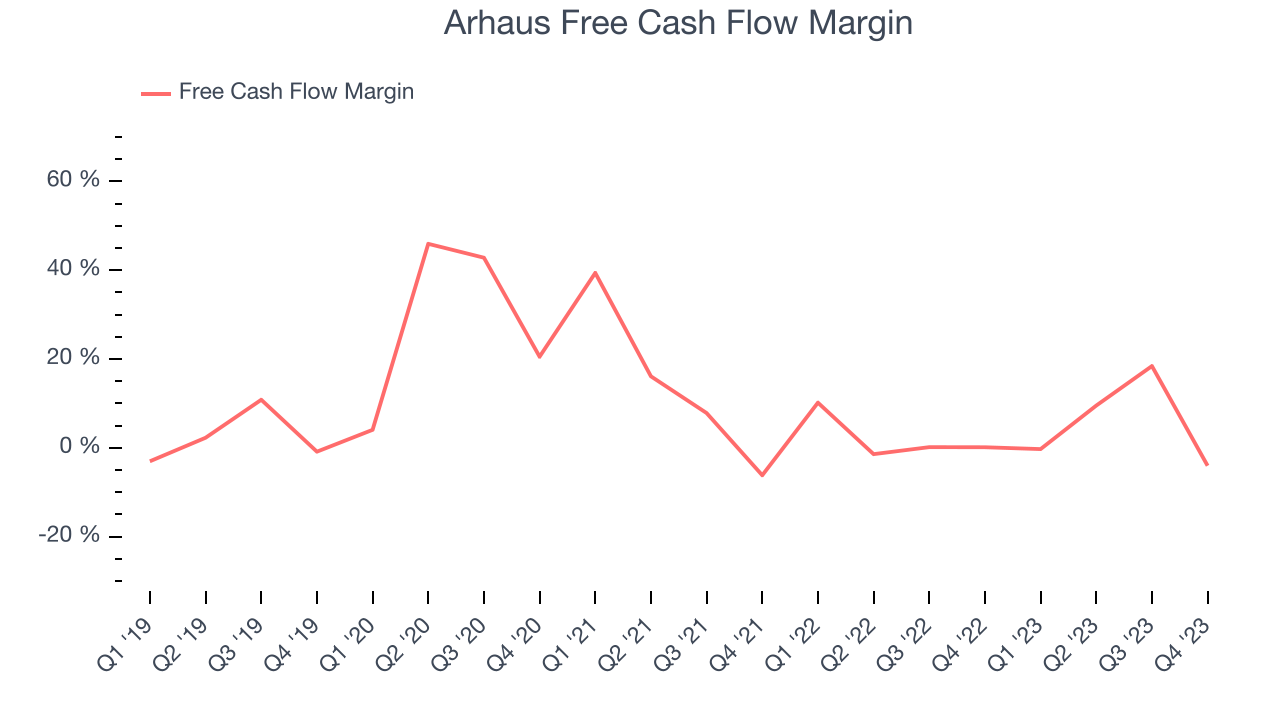

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe in the end, cash is king, and you can't use accounting profits to pay the bills.

Arhaus burned through $13.82 million of cash in Q4, representing a negative 4% free cash flow margin. The company shifted to cash flow negative from cash flow positive in the same quarter last year, which happened for several reasons including (but not limited to) the stockpiling of inventory in anticipation of higher demand or unforeseen, one-time events.

Over the last two years, Arhaus has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 3.9%, slightly better than the broader consumer retail sector. Furthermore, its margin has averaged year-on-year increases of 4.1 percentage points. This likely pleases the company's investors.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Arhaus's five-year average ROIC was negative 0.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer retail sector.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last two years, Arhaus's ROIC averaged 87.2 percentage point increases each year. This is a good sign, and if the company's returns keep rising, there's a chance it could evolve into an investable business.

Key Takeaways from Arhaus's Q4 Results

We were impressed by how significantly Arhaus blew past analysts' operating income and EPS forecasts this quarter. We were also excited its revenue outperformed Wall Street's estimates. Those two beats were driven by better-than-expected same-store sales performance (6.8% decline compared to an estimated 10.4% decline). Given the strong quarter, management shared upbeat revenue and EBITDA guidance for the full year 2024, easily topping analysts' estimates.

Because its free cash flow for the full year 2023 beat its internal projections, Arhaus is declaring a special, one-time cash dividend of $0.50 per share - this represents a ~4% yield on the current share price. The dividend will be payable on April 4, 2024, to shareholders of record on March 21, 2024.

Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is flat after reporting and currently trades at $12.75 per share.

Is Now The Time?

Arhaus may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We have other favorites, but we understand the arguments that Arhaus isn't a bad business. First off, its revenue growth has been exceptional over the last four years. And while its relatively low ROIC suggests it has struggled to grow profits historically, its EPS growth over the last four years has been fantastic.

Arhaus's price-to-earnings ratio based on the next 12 months is 17.4x. There are things to like about Arhaus and there's no doubt it's a bit of a market darling, at least for some investors. But it seems there's a lot of optimism already priced in and we wonder if there are better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $13.85 per share right before these results (compared to the current share price of $12.75).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.