Array's (NASDAQ:ARRY) Q2 Sales Top Estimates But Stock Drops

Anthony Lee /

August 8, 2024

Solar tracking systems manufacturer Array (NASDAQ:ARRY) reported Q2 CY2024 results topping analysts' expectations, with revenue down 49.6% year on year to $255.8 million. On the other hand, the company's full-year revenue guidance of $950 million at the midpoint came in 28.2% below analysts' estimates. It made a non-GAAP profit of $0.20 per share, down from its profit of $0.26 per share in the same quarter last year.

Is now the time to buy Array? Find out in our full research report.

Array (ARRY) Q2 CY2024 Highlights:

- Revenue: $255.8 million vs analyst estimates of $234.3 million (9.2% beat)

- EPS (non-GAAP): $0.20 vs analyst estimates of $0.11 ($0.09 beat)

- The company dropped its revenue guidance for the full year from $1.33 billion to $950 million at the midpoint, a 28.3% decrease

- EPS (non-GAAP) guidance for the full year is $0.69 at the midpoint, missing analyst estimates by 36.3%

- EBITDA guidance for the full year is $197.5 million at the midpoint, below analyst estimates of $295.6 million

- Gross Margin (GAAP): 33.6%, up from 29.6% in the same quarter last year

- EBITDA Margin: 21.7%, down from 22.8% in the same quarter last year

- Free Cash Flow of $1.83 million, down 96% from the previous quarter

- Market Capitalization: $1.31 billion

“We finished the second quarter with strong performance and execution and are pleased with the continued demand we’re seeing in our high-probability pipeline. Our orderbook remains healthy at over $2 billion and we’re encouraged by our customers’ interest in our portfolio of products and services and the longer-term tailwinds supporting utility-scale solar as one of the lowest cost options to satisfy rapidly growing energy needs,” said Chief Executive Officer, Kevin Hostetler.

Going public in October 2020, Array (NASDAQ:ARRY) is a global manufacturer of ground-mounting tracking systems for utility and distributed generation solar energy projects.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

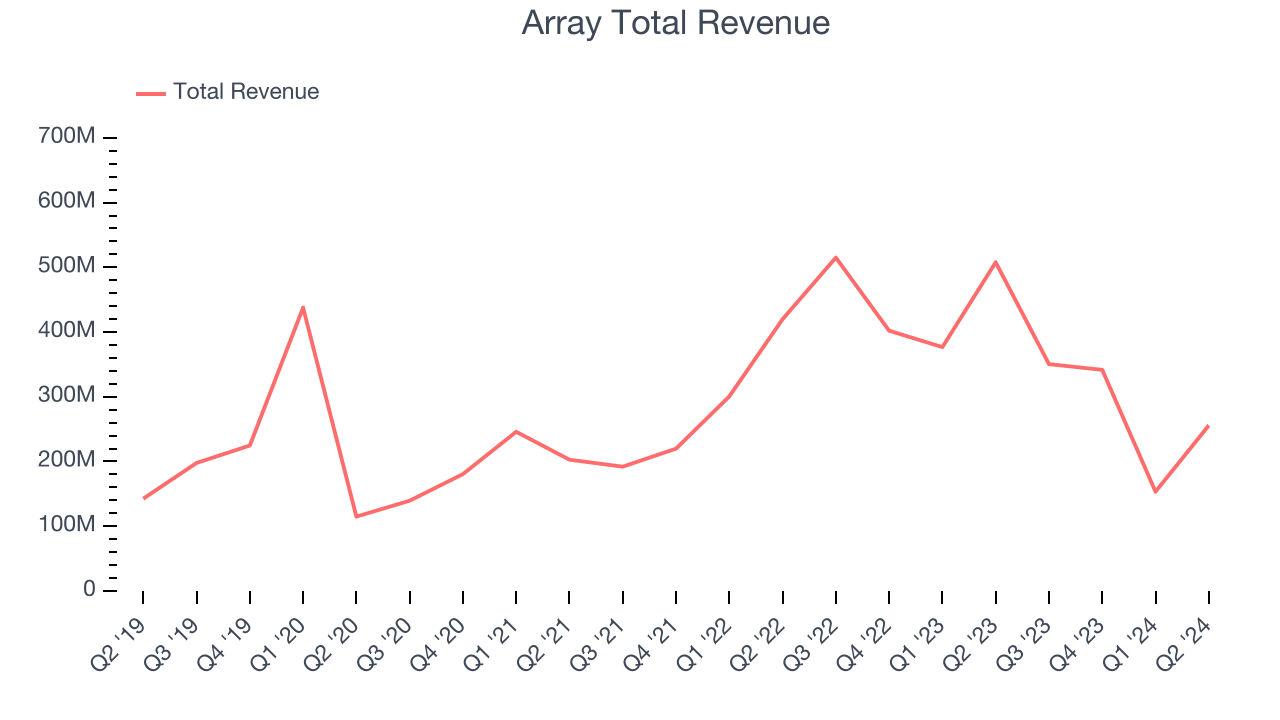

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Thankfully, Array's 23.8% annualized revenue growth over the last five years was incredible. This shows it expanded quickly, a useful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Array's recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.4% over the last two years.

This quarter, Array's revenue fell 49.6% year on year to $255.8 million but beat Wall Street's estimates by 9.2%. Looking ahead, Wall Street expects sales to grow 43.2% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

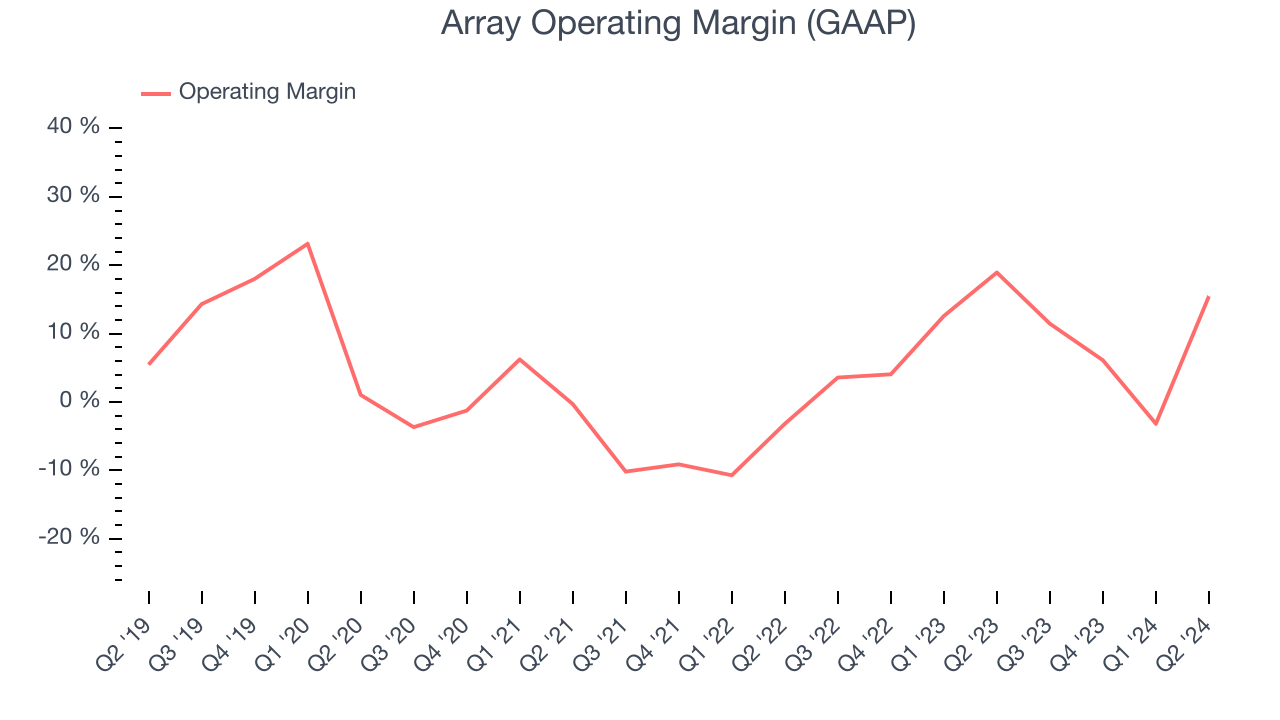

Array was profitable over the last five years but held back by its large expense base. It demonstrated paltry profitability for an industrials business, producing an average operating margin of 6.4%. This result isn't too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Array's annual operating margin decreased by 8.9 percentage points over the last five years. The company's performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn't pass those costs onto its customers.

In Q2, Array generated an operating profit margin of 15.5%, down 3.5 percentage points year on year. Conversely, the company's gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like sales, marketing, R&D, and administrative overhead.

EPS

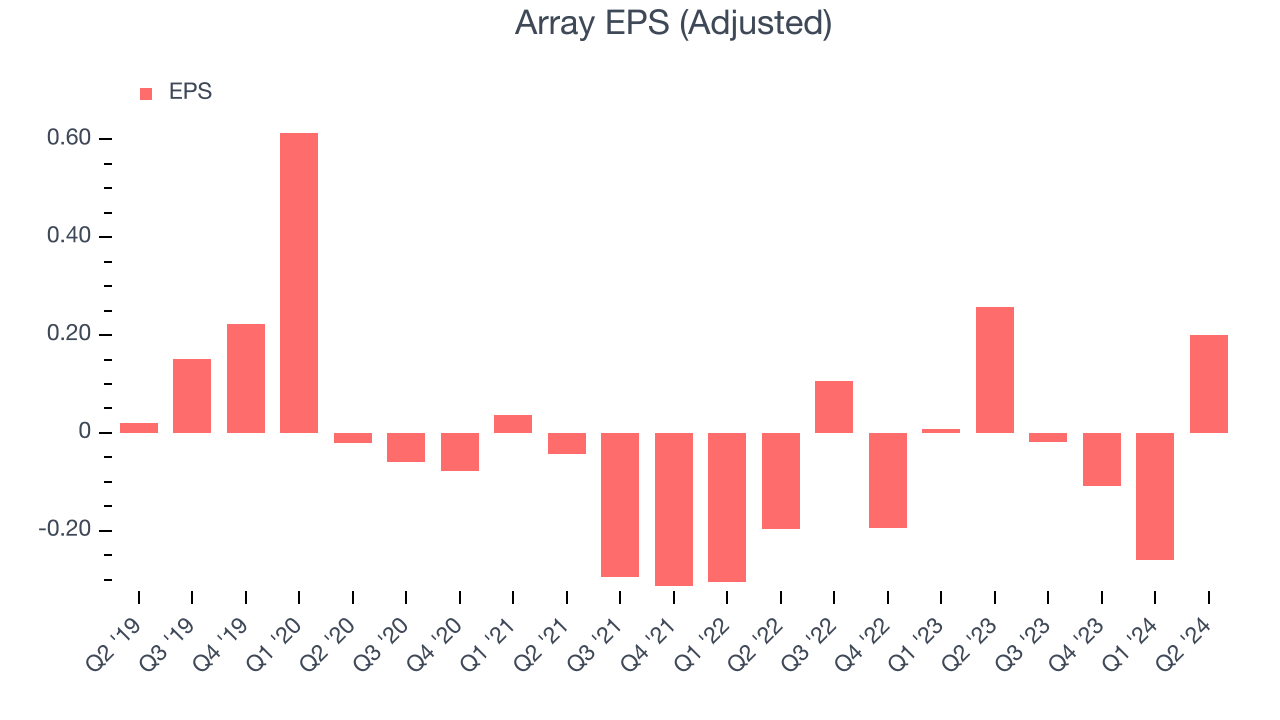

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Array's earnings losses deepened over the last five years as its EPS dropped 13.8% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Array's low margin of safety could leave its stock price susceptible to large downswings.

In Q2, Array reported EPS at $0.20, down from $0.26 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. Over the next 12 months, Wall Street is optimistic. Analysts are projecting Array's EPS of negative $0.19 in the last year to flip to positive $1.38.

Key Takeaways from Array's Q2 Results

We were impressed by how significantly Array blew past analysts' EPS expectations this quarter. We were also excited its revenue outperformed Wall Street's estimates. On the other hand, its full-year revenue guidance missed and its EBITDA guidance for the full year fell short of Wall Street's estimates. Overall, this was a mixed but overall mediocre quarter for Array. The stock traded down 5.7% to $8.50 immediately following the results.

Array may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.