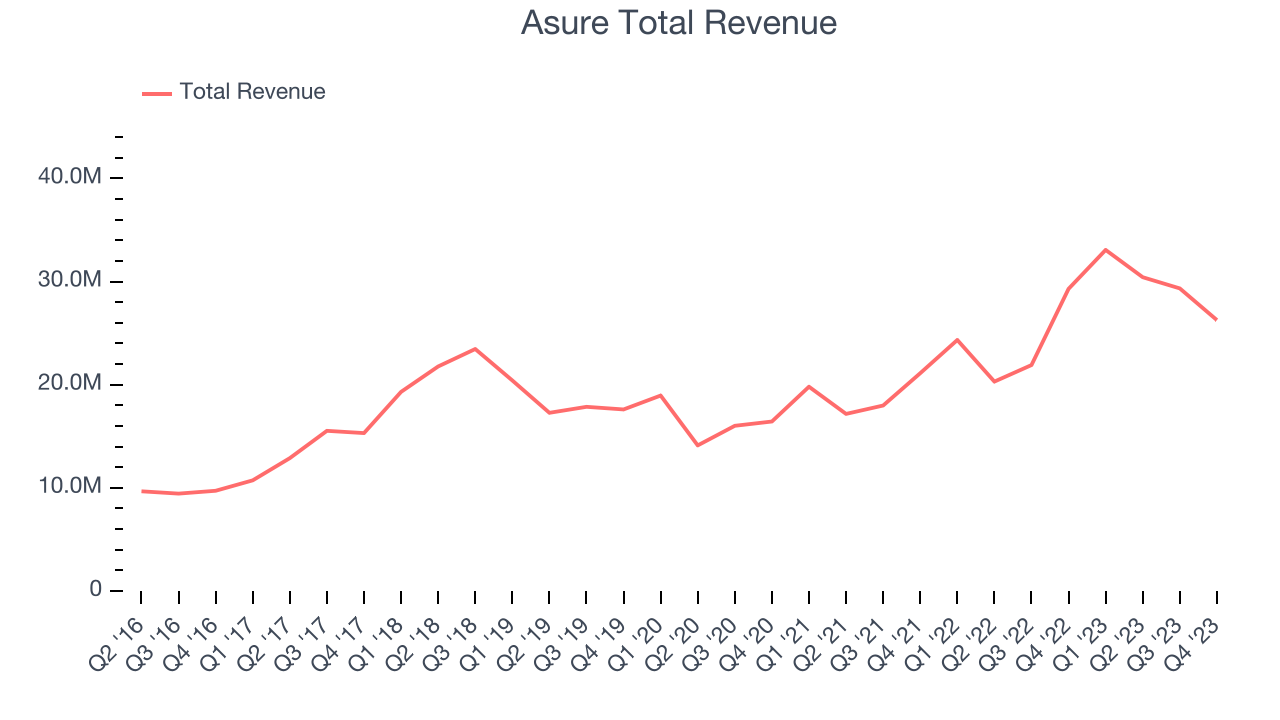

Online payroll and human resource software provider Asure (NASDAQ:ASUR) reported results in line with analysts' expectations in Q4 FY2023, with revenue down 10.3% year on year to $26.26 million. On the other hand, next quarter's revenue guidance of $31 million was less impressive, coming in 4.5% below analysts' estimates. It made a GAAP loss of $0.14 per share, down from its profit of $0.17 per share in the same quarter last year.

Asure (ASUR) Q4 FY2023 Highlights:

- Revenue: $26.26 million vs analyst estimates of $26.32 million (small miss)

- EPS: -$0.14 vs analyst expectations of -$0.13 (7.7% miss)

- Revenue Guidance for Q1 2024 is $31 million at the midpoint, below analyst estimates of $32.46 million

- Management's revenue guidance for the upcoming financial year 2024 is $127 million at the midpoint, beating analyst estimates by 4.3% and implying 6.6% growth (vs 27.3% in FY2023)

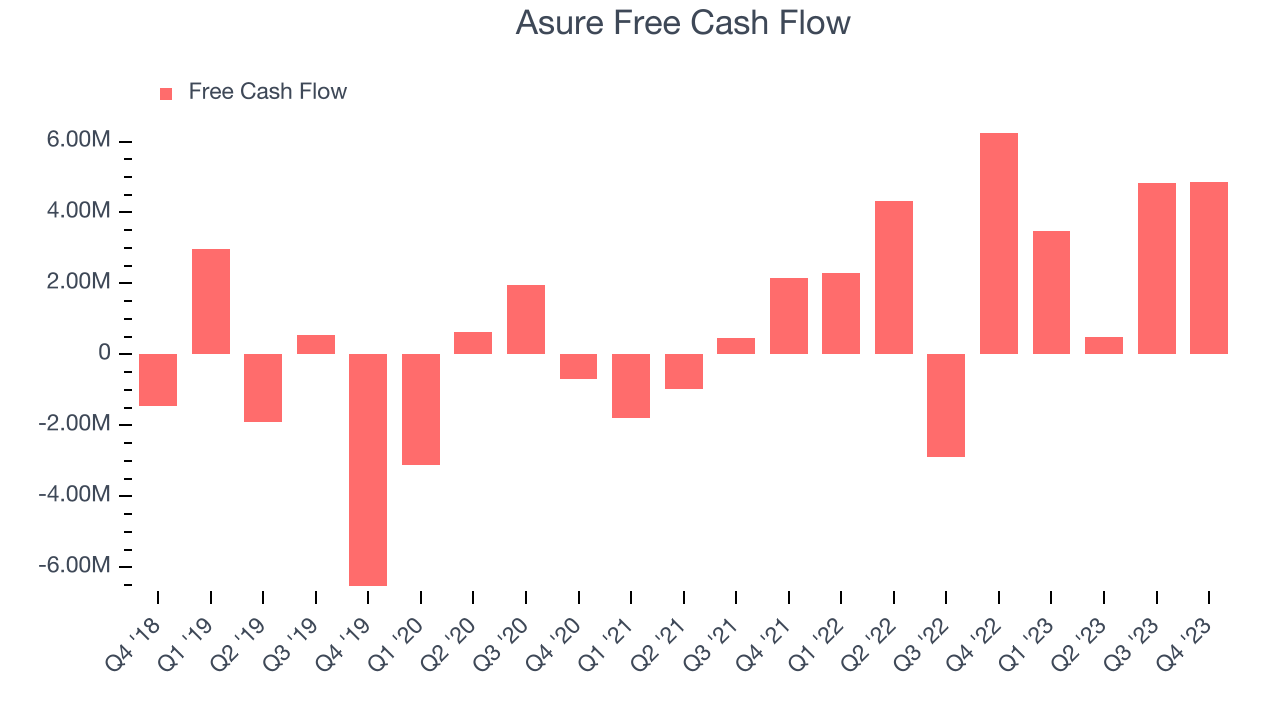

- Free Cash Flow of $4.85 million, similar to the previous quarter

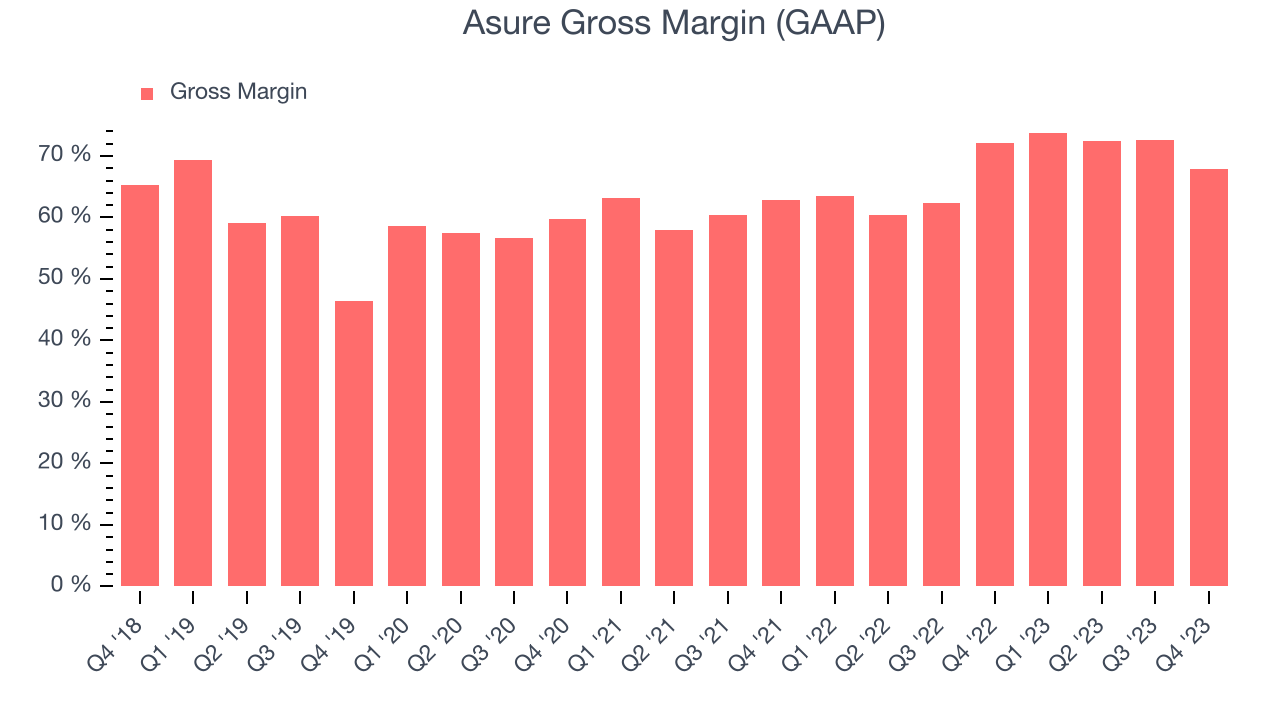

- Gross Margin (GAAP): 67.9%, down from 72.2% in the same quarter last year

- Market Capitalization: $247.3 million

Created from the merger of two small workforce management companies in 2007, Asure (NASDAQ:ASUR) provides cloud based payroll and HR software for small and medium-sized businesses (SMBs).

Human Capital Management (HCM) software is meant to streamline mundane, but vital, business functions like keeping attendance, running payroll, and keeping compliant with shifting Federal and local government taxes and labor laws. For many small and medium sized businesses, these are often handled by their accountant which is an unnecessarily expensive use of resources, or QuickBooks style spreadsheets which don’t have sufficient functionality.

Enter Asure, who offers inexpensive cloud-based subscription software that automates the full spectrum of HR tasks, from handling payroll to managing benefits or submitting leave requests.

The company has a unique go-to-market strategy that focuses on underserved customers, specifically SMBs located outside the Top 10 US metropolitan markets. In addition to a direct sales force, Asure leans heavily on resellers (e.g. regional payroll providers focused on a specific vertical) and referral partners (e.g. regional banks and benefits brokers) who will resell Asure's products under their own brand.

HR Software

Modern HR software has two powerful benefits: cost savings and ease of use. For cost savings, businesses large and small much prefer the flexibility of cloud-based, web-browser-delivered software paid for on a subscription basis rather than the hassle and complexity of purchasing and managing on-premise enterprise software. On the usability side, the consumerization of business software creates seamless experiences whereby multiple standalone processes like payroll processing and compliance are aggregated into a single, easy-to-use platform.

Asure’s main competitors are legacy providers ADP (NASDAQ:ADP) and Paychex (NASDAQ:PAYX), as churn from these two represent a large part of Asure’s new clients annually. Other cloud-first providers of HR solutions for small and medium-sized businesses include Ceridian (NYSE:CDAY), Paycom (NYSE:PAYC), Paycor (NASDAQ:PYCR), Paylocity (NASDAQ:PCTY), and Workday (NASDAQ:WDAY).

Sales Growth

As you can see below, Asure's revenue growth has been strong over the last two years, growing from $21.11 million in Q4 FY2021 to $26.26 million this quarter.

This quarter, Asure's revenue was down 10.3% year on year, which might disappointment some shareholders.

Next quarter, Asure is guiding for a 6.2% year-on-year revenue decline to $31 million, a further deceleration from the 35.9% year-on-year decrease it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $127 million at the midpoint, growing 6.6% year on year compared to the 24.3% increase in FY2023.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Asure's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 67.9% in Q4.

That means that for every $1 in revenue the company had $0.68 left to spend on developing new products, sales and marketing, and general administrative overhead. Asure's gross margin is poor for a SaaS business and it's dropped significantly since the previous quarter. This is probably the exact opposite of what shareholders would like to see.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Asure's free cash flow came in at $4.85 million in Q4, down 22.5% year on year.

Asure has generated $13.64 million in free cash flow over the last 12 months, or 11.5% of revenue. This FCF margin stems from its asset-lite business model and enables it to reinvest in its business without depending on the capital markets.

Key Takeaways from Asure's Q4 Results

It was good to see Asure's full-year 2024 sales and EBITDA outlook exceed analysts' expectations. On the other hand, this quarter's revenue and EPS missed Wall Street's estimates and its revenue outlook for next quarter was soft, suggesting slower demand to start the year. Overall, the results could have been better. The company is down 1.2% on the results and currently trades at $10.12 per share.

Is Now The Time?

When considering an investment in Asure, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We cheer for everyone who's making the lives of others easier through technology, but in case of Asure, we'll be cheering from the sidelines. Although its , Wall Street expects growth to deteriorate from here. On top of that, its customer acquisition is less efficient than many comparable companies.

Asure's price-to-sales ratio based on the next 12 months is 2.1x, suggesting that the market does have lower expectations of the business, relative to the high growth tech stocks. While we have no doubt one can find things to like about the company, we think there might be better opportunities in the market and at the moment don't see many reasons to get involved.

Wall Street analysts covering the company had a one-year price target of $14.63 per share right before these results (compared to the current share price of $10.12).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.