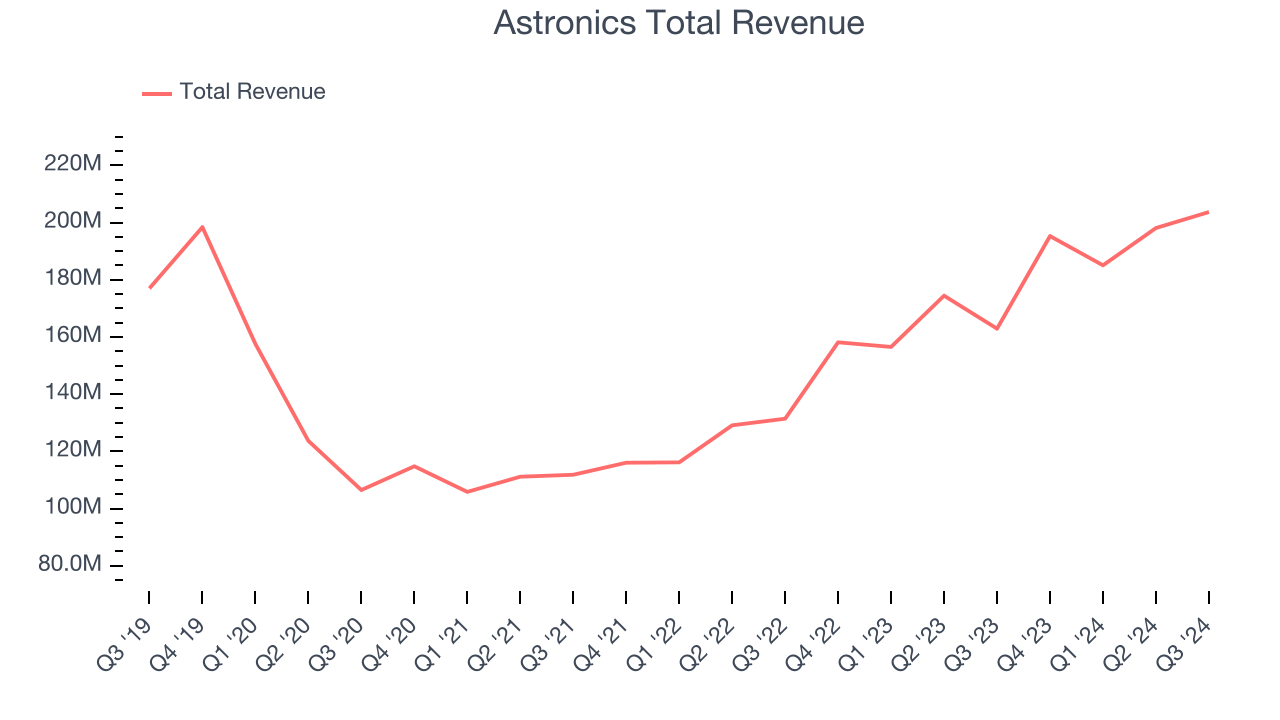

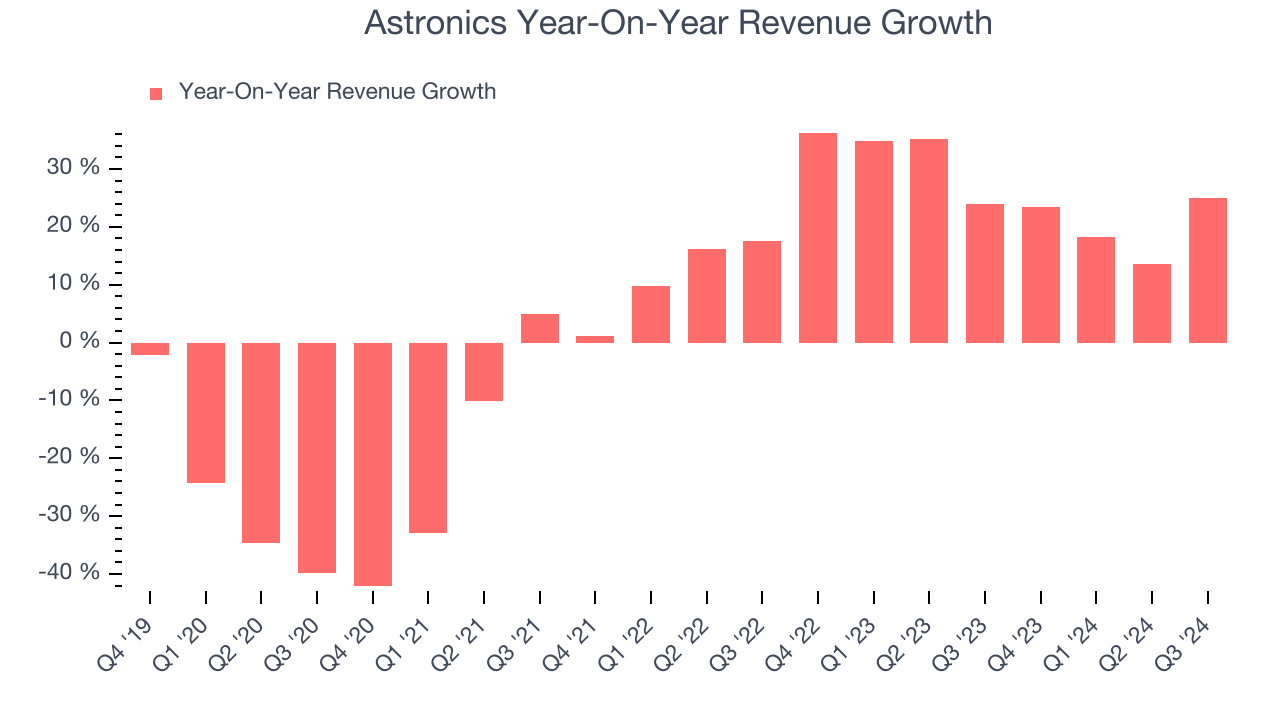

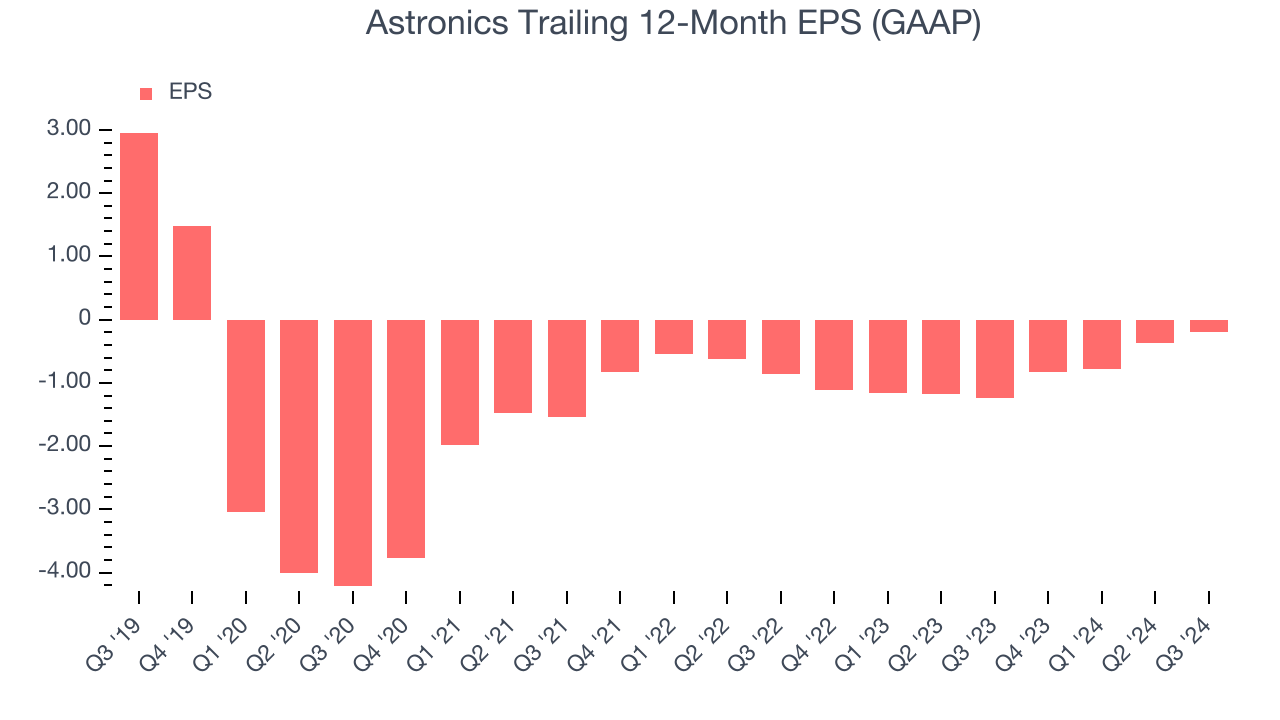

Aerospace and defense technology solutions provider Astronics Corporation (NASDAQ:ATRO) announced better-than-expected revenue in Q3 CY2024, with sales up 25% year on year to $203.7 million. The company expects next quarter’s revenue to be around $200 million, close to analysts’ estimates. Its GAAP loss of $0.34 per share was 1,600% below analysts’ consensus estimates.

Is now the time to buy Astronics? Find out by accessing our full research report, it’s free.

Astronics (ATRO) Q3 CY2024 Highlights:

- Revenue: $203.7 million vs analyst estimates of $198.6 million (2.6% beat)

- EPS: -$0.34 vs analyst estimates of -$0.02 (-$0.32 miss)

- EBITDA: $27.06 million vs analyst estimates of $25.18 million (7.5% beat)

- Revenue Guidance for Q4 CY2024 is $200 million at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 21%, up from 12.7% in the same quarter last year

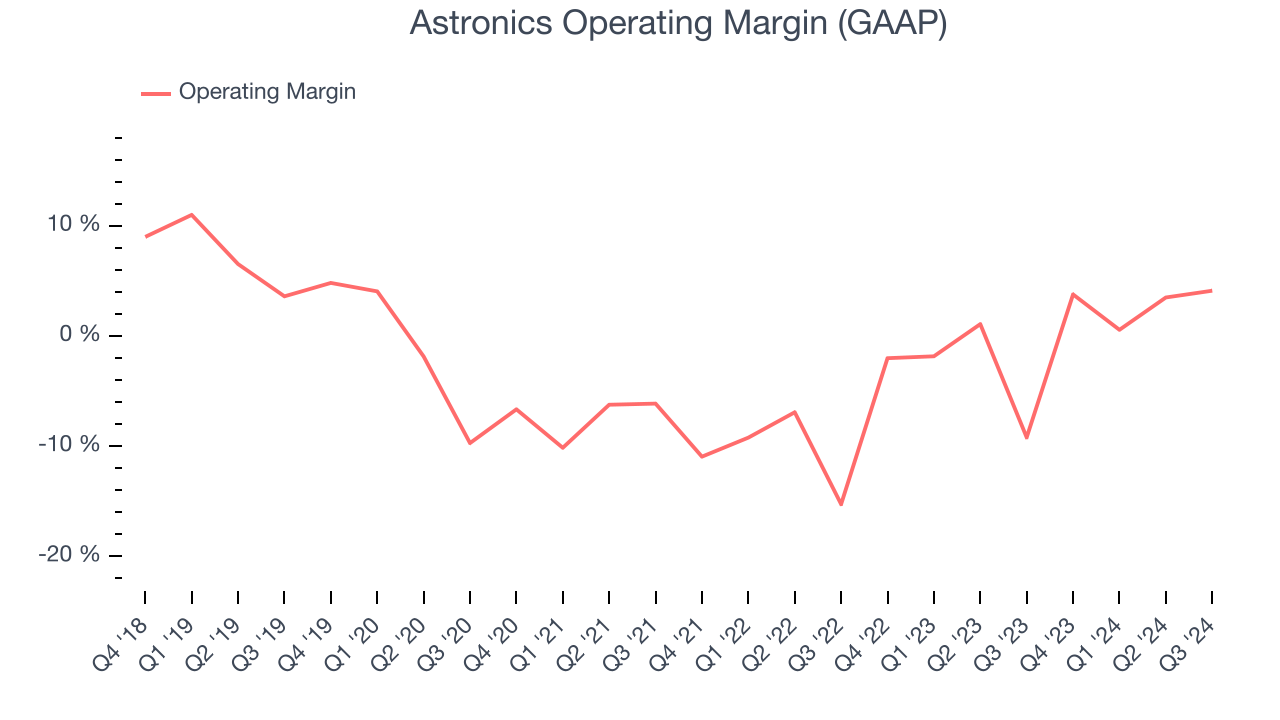

- Operating Margin: 4.1%, up from -9.2% in the same quarter last year

- EBITDA Margin: 13.3%, up from -7.4% in the same quarter last year

- Free Cash Flow was $6.52 million, up from -$3.36 million in the same quarter last year

- Backlog: $611.9 million at quarter end

- Market Capitalization: $642 million

Peter J. Gundermann, Chairman, President and Chief Executive Officer, commented, “We delivered a solid third quarter operationally. Revenue was at the high end of our range, up 25% over the comparator quarter. Adjusted EBITDA was $27.1 million for the quarter and $91 million for the trailing twelve months. Operating margins improved from both volume and the initiatives we have executed to drive profitability. Our Aerospace segment adjusted operating margin was 14.2%. We are clearly making progress towards our operational goals, though our results include the impact of expenses related to our July refinancing, a customer bankruptcy and a warranty reserve. All in all, we feel it was another quarter of progress as we continue to recover from the disruption of the past few years.”

Company Overview

Integrating power outlets into many Boeing aircraft, Astronics (NASDAQ:ATRO) is a provider of technologies and services to the global aerospace, defense, and electronics industries.

Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Astronics struggled to generate demand over the last five years as its sales were flat. This is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Astronics’s annualized revenue growth of 26% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Astronics reported robust year-on-year revenue growth of 25%, and its $203.7 million of revenue topped Wall Street estimates by 2.6%. Management is currently guiding for a 2.4% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and shows the market believes its products and services will see some demand headwinds.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Although Astronics was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 2.6% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Astronics’s annual operating margin rose by 2.5 percentage points over the last five years. Still, it will take much more for the company to show consistent profitability.

In Q3, Astronics generated an operating profit margin of 4.1%, up 13.3 percentage points year on year. This increase was a welcome development and shows it was recently more efficient because its expenses grew slower than its revenue.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Astronics, its EPS declined by 15.6% annually over the last five years while its revenue was flat. However, its operating margin actually expanded during this timeframe, telling us that non-fundamental factors affected its ultimate earnings.

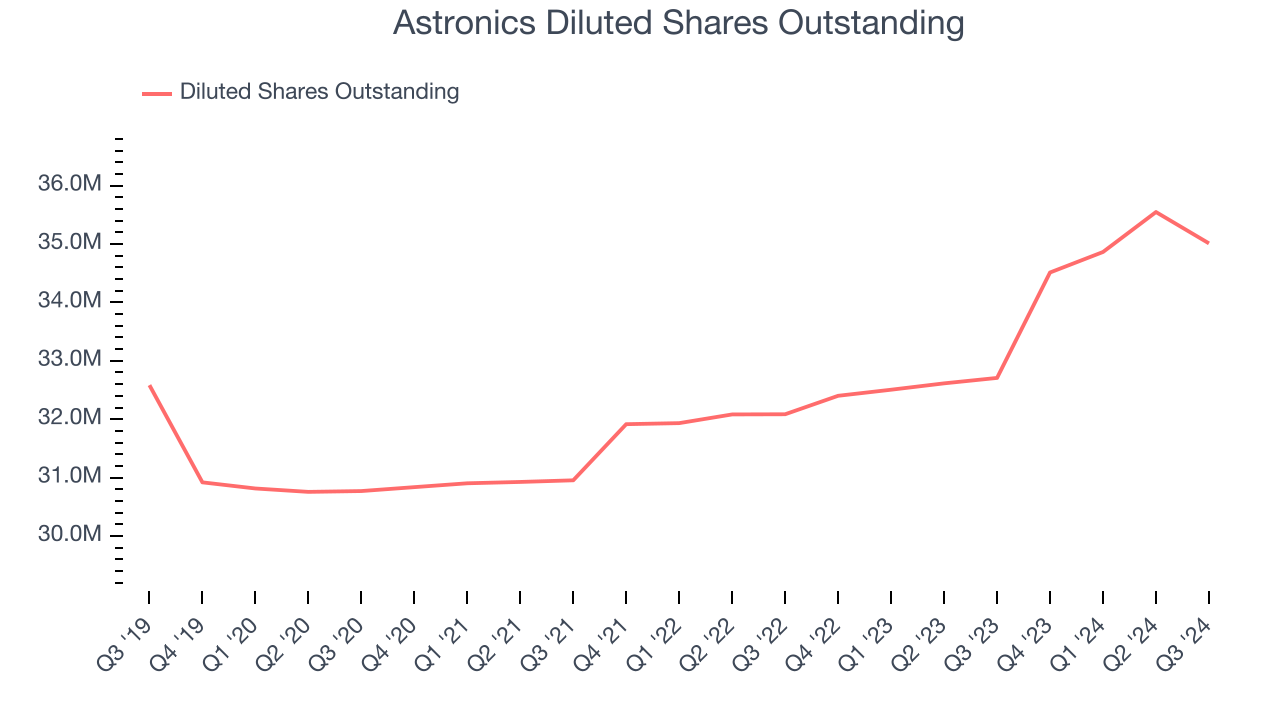

We can take a deeper look into Astronics’s earnings to better understand the drivers of its performance. A five-year view shows Astronics has diluted its shareholders, growing its share count by 7.5%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

For Astronics, its two-year annual EPS growth of 53% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.In Q3, Astronics reported EPS at negative $0.34, up from negative $0.52 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Astronics’s full-year EPS of negative $0.19 will flip to positive $0.63.

Key Takeaways from Astronics’s Q3 Results

We were impressed by how significantly Astronics blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed and its backlog fell. Overall, this quarter had some positives, but the weaker backlog is sending shares lower. ATRO traded down 12.6% to $18 immediately following the results.

So should you invest in Astronics right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.