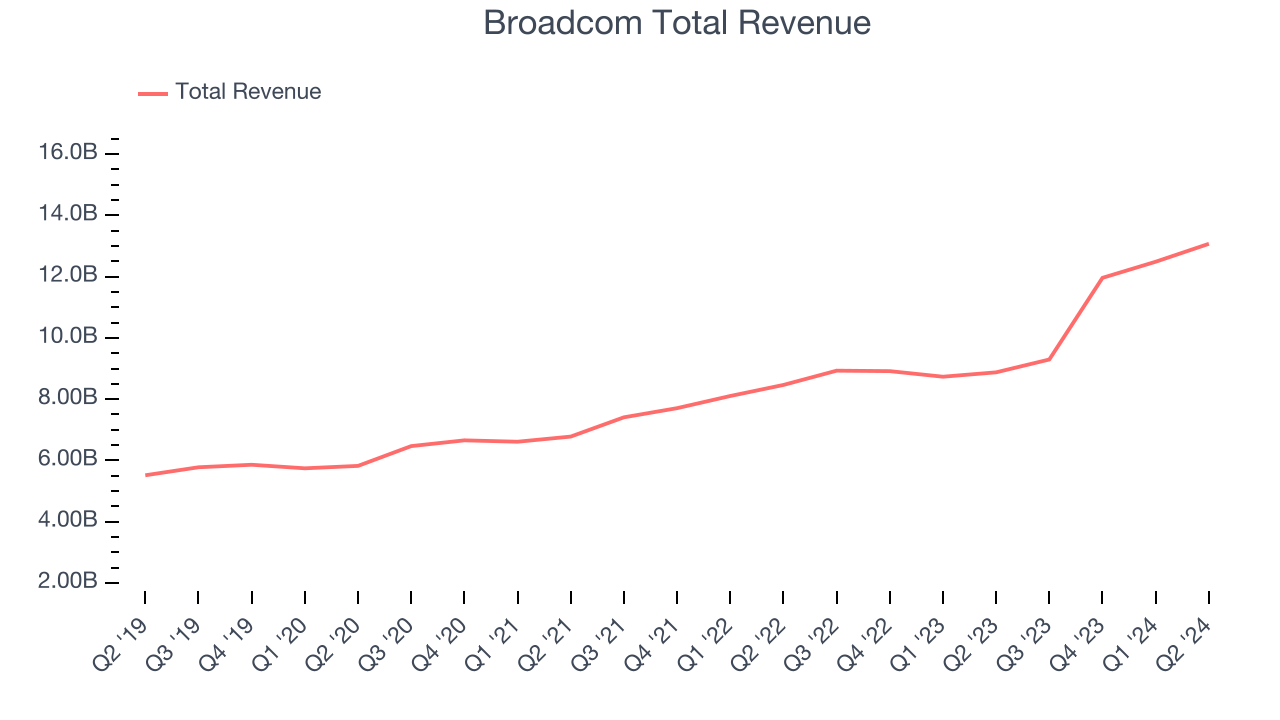

Fabless chip and software maker Broadcom (NASDAQ:AVGO) reported results ahead of analysts’ expectations in Q2 CY2024, with revenue up 47.3% year on year to $13.07 billion. The company expects next quarter’s revenue to be around $14 billion, in line with analysts’ estimates. It made a non-GAAP profit of $1.24 per share, improving from its profit of $1.05 per share in the same quarter last year.

Is now the time to buy Broadcom? Find out by accessing our full research report, it’s free.

Broadcom (AVGO) Q2 CY2024 Highlights:

- Revenue: $13.07 billion vs analyst estimates of $12.96 billion (small beat)

- Adjusted Operating Income: $7.95 billion vs analyst estimates of $7.68 billion (3.4% beat)

- EPS (non-GAAP): $1.24 vs analyst estimates of $1.21 (2.8% beat)

- Revenue Guidance for Q3 CY2024 is $14 billion at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 76%, up from 74.4% in the same quarter last year

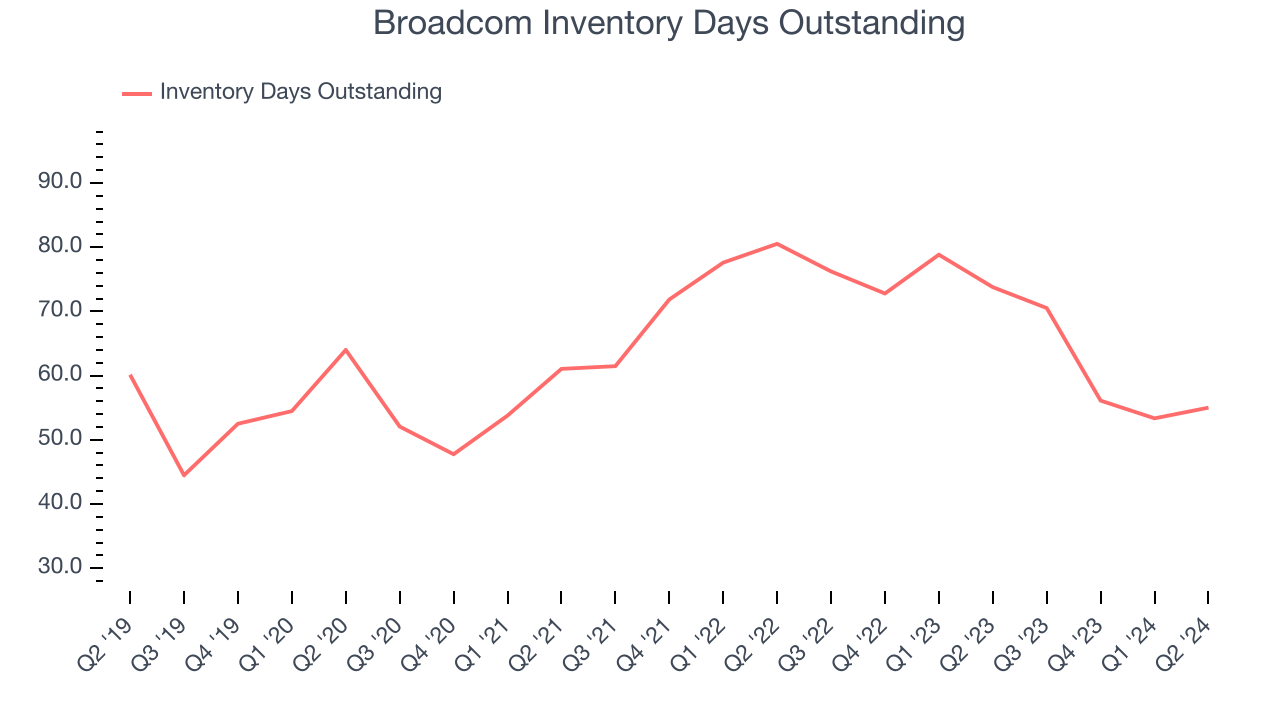

- Inventory Days Outstanding: 55, up from 53 in the previous quarter

- EBITDA Margin: 62.9%, down from 65.4% in the same quarter last year

- Free Cash Flow Margin: 36.7%, down from 51.8% in the same quarter last year

- Market Capitalization: $717.4 billion

"Broadcom's third quarter results reflect continued strength in our AI semiconductor solutions and VMware. We expect revenue from AI to be $12 billion for fiscal year 2024 driven by Ethernet networking and custom accelerators for AI data centers," said Hock Tan, President and CEO of

Originally the semiconductor division of Hewlett Packard, Broadcom (NASDAQ:AVGO) is a semiconductor conglomerate that spans wireless, networking, data storage, and industrial end markets along with an infrastructure software business focused on mainframes and cybersecurity.

Processors and Graphics Chips

The biggest demand drivers for processors (CPUs) and graphics chips at the moment are secular trends related to 5G and Internet of Things, autonomous driving, and high performance computing in the data center space, specifically around AI and machine learning. Like all semiconductor companies, digital chip makers exhibit a degree of cyclicality, driven by supply and demand imbalances and exposure to PC and Smartphone product cycles.

Sales Growth

Broadcom’s revenue growth over the last three years has been strong, averaging 21.3% annually. As you can see below, this quarter was especially strong, with revenue growing from $8.88 billion in the same quarter last year to $13.07 billion. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Broadcom had a great quarter as its 47.3% year-on-year revenue growth was in line with analysts’ estimates.

Broadcom’s management team believes its revenue growth will accelerate, guiding to 50.6% year-on-year growth next quarter. Wall Street expects the company to grow its revenue by 26.4% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Broadcom’s DIO came in at 55, which is 8 days below its five-year average. These numbers show that despite the recent increase, there’s no indication of an excessive inventory buildup.

Key Takeaways from Broadcom’s Q2 Results

It was good to see Broadcom beat analysts’ EPS expectations this quarter. We were also glad its gross margin improved. On the other hand, its revenue guidance for next quarter was underwhelming and its inventory levels slightly increased. Zooming out, we think this was a decent quarter featuring some areas of strength, but guidance is weighing on shares. The areas below expectations seem to be driving the stock move, and the stock traded down 4.3% to $146.39 immediately following the results.

So should you invest in Broadcom right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.