Communications platform-as-a-service company Bandwidth (NASDAQ: BAND) reported Q1 CY2024 results exceeding Wall Street analysts' expectations, with revenue up 24.1% year on year to $171 million. On top of that, next quarter's revenue guidance ($173 million at the midpoint) was surprisingly good and 4.1% above what analysts were expecting. It made a non-GAAP profit of $0.27 per share, improving from its profit of $0.04 per share in the same quarter last year.

Bandwidth (BAND) Q1 CY2024 Highlights:

- Revenue: $171 million vs analyst estimates of $165.1 million (3.6% beat)

- EPS (non-GAAP): $0.27 vs analyst estimates of $0.20 (33.3% beat)

- Revenue Guidance for Q2 CY2024 is $173 million at the midpoint, above analyst estimates of $166.1 million

- The company lifted its revenue guidance for the full year from $700 million to $715 million at the midpoint, a 2.1% increase

- Gross Margin (GAAP): 38.3%, down from 40.4% in the same quarter last year

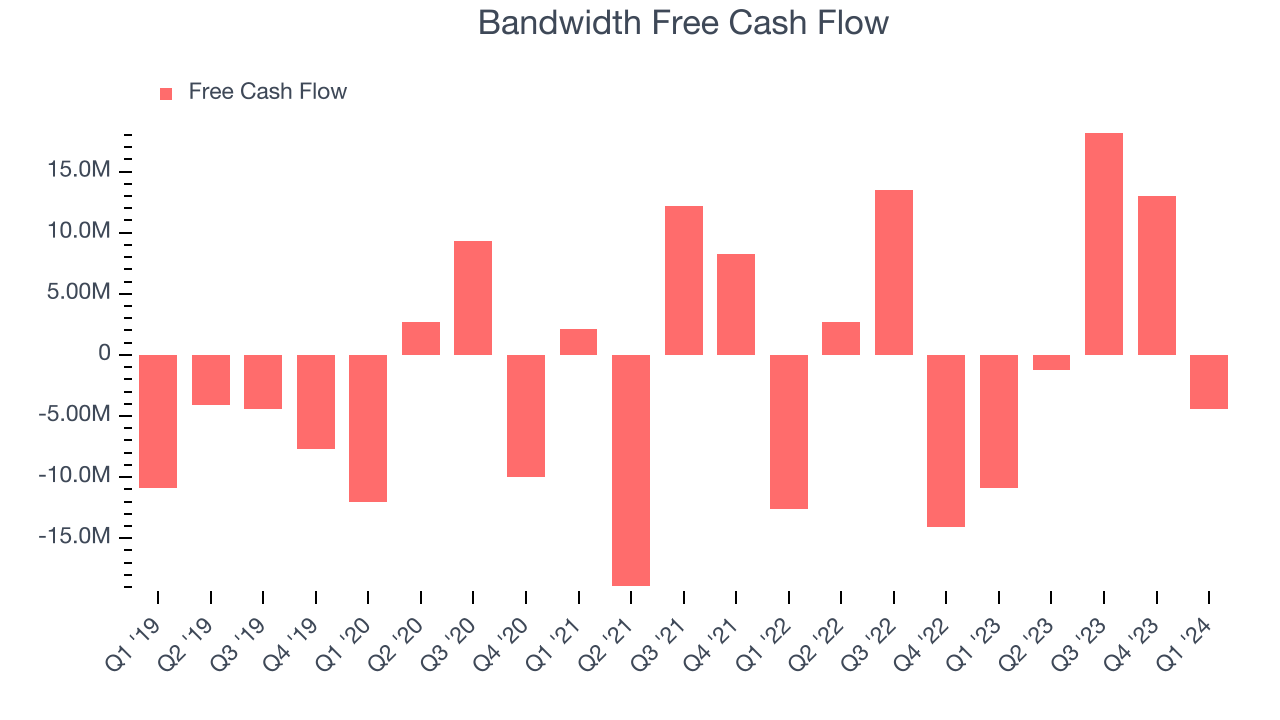

- Free Cash Flow was -$4.41 million, down from $13.04 million in the previous quarter

- Market Capitalization: $553.3 million

Started in 1999 by David Morken who was later joined by Henry Kaestner as co-founder in 2001, Bandwidth (NASDAQ:BAND) provides thousands of customers with a software platform that uses its own global network to provide phone numbers, voice, and text connectivity.

Founder David Morken started Bandwidth while on 90 days of paid leave from the Marine Corps. He moved into his parent’s house with his three children and wife to bootstrap the company.

Bandwidth might not be well known to consumers, but most of us would have used their services unknowingly either using online conferencing software or contacting customer service representatives through a company’s website. Bandwidth’s core advantage is that it provides a software platform over its own telecommunications network, and is therefore able to better control the quality of the connection, all while providing cheaper prices than a legacy voice connection.

Communications Platform

The first shift towards voice communication over the internet (VOIP), rather than traditional phone networks, happened when the enterprises started replacing business phones with the cheaper VOIP technology. Today, the rise of the consumer internet has increased the need for two way audio and video functionality in applications, driving demand for software tools and platforms that enable this utility.

Even though Bandwidth competes with other well known CPaaS companies like Twilio (NYSE:TWLO), it mostly competes with legacy telecommunications companies such as Verizon (NYSE:VZ) and AT&T (NYSE:T), which lack the equivalent software layer over their own networks.

Sales Growth

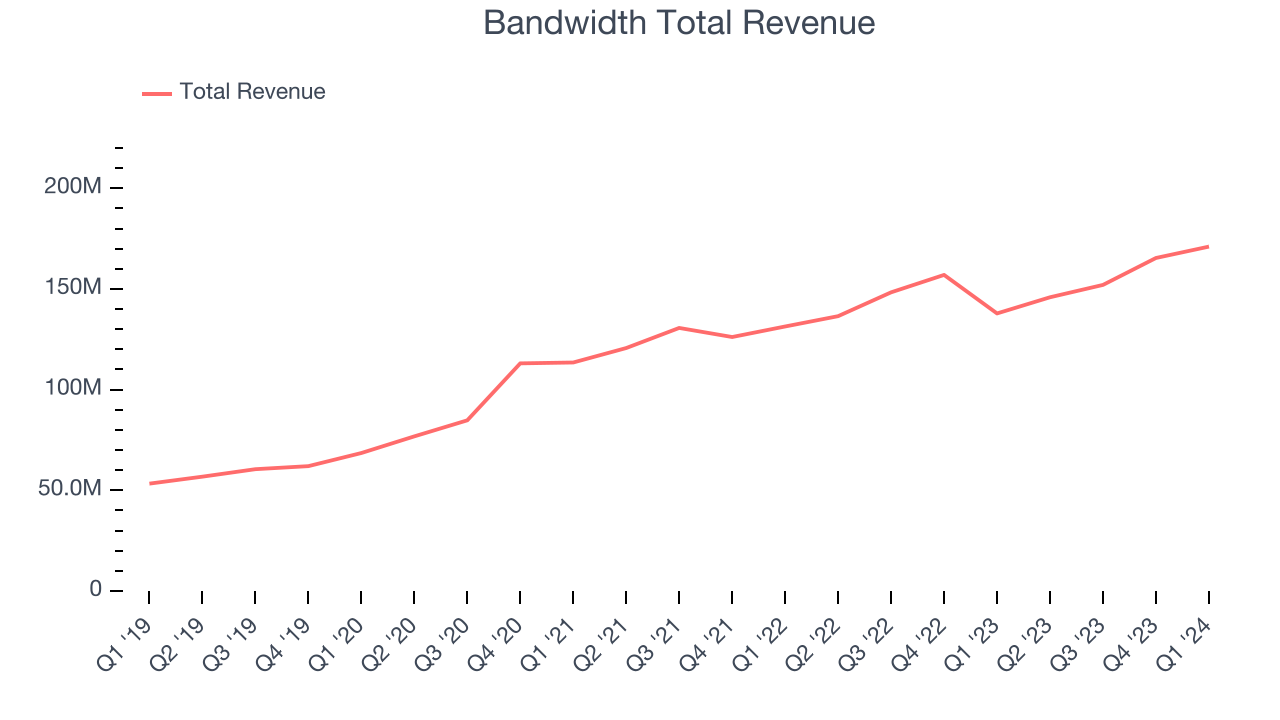

As you can see below, Bandwidth's revenue growth has been mediocre over the last three years, growing from $113.5 million in Q1 2021 to $171 million this quarter.

This quarter, Bandwidth's quarterly revenue was up a very solid 24.1% year on year, above the company's historical trend. However, its growth did slow down compared to last quarter as the company's revenue increased by just $5.65 million in Q1 compared to $13.37 million in Q4 CY2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Bandwidth is expecting revenue to grow 18.6% year on year to $173 million, improving on the 6.9% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 12.3% over the next 12 months before the earnings results announcement.

Profitability

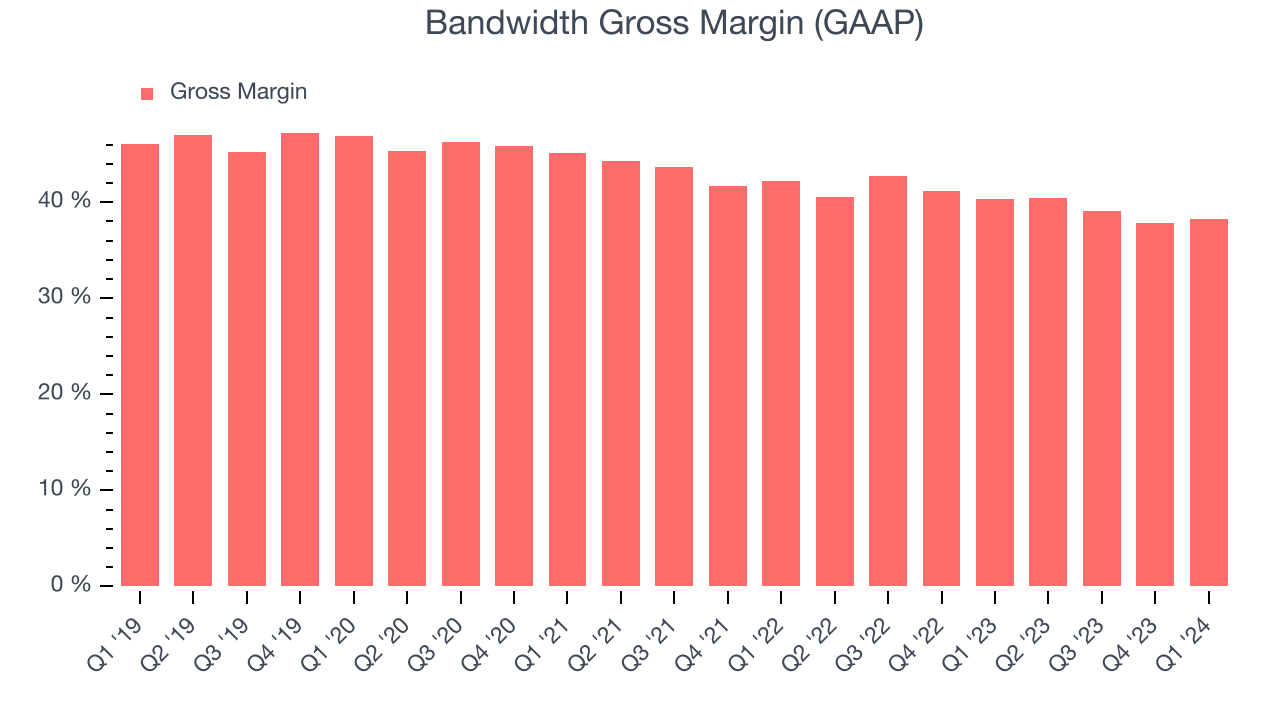

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Bandwidth's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 38.3% in Q1.

That means that for every $1 in revenue the company had $0.38 left to spend on developing new products, sales and marketing, and general administrative overhead. While its gross margin has improved significantly since the previous quarter, Bandwidth's gross margin is still poor for a SaaS business. It's vital that the company continues to improve this key metric.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Bandwidth burned through $4.41 million of cash in Q1 , increasing its cash burn by 59.6% year on year.

Bandwidth has generated $25.6 million in free cash flow over the last 12 months, or 4% of revenue. This FCF margin enables it to reinvest in its business without depending on the capital markets.

Key Takeaways from Bandwidth's Q1 Results

This was a rare beat and raise quarter. Specifically, it was great to see Bandwidth's optimistic revenue guidance for next quarter, which exceeded analysts' expectations. Full year revenue guidance was raised. We were also glad its revenue outperformed Wall Street's estimates. Overall, we think this was a strong quarter that should satisfy shareholders. The stock is up 7.1% after reporting and currently trades at $22 per share.

Is Now The Time?

When considering an investment in Bandwidth, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although Bandwidth isn't a bad business, it probably wouldn't be one of our picks. Its revenue growth has been a little slower over the last three years, and analysts expect growth to deteriorate from here. And while its efficient customer acquisition hints at the potential for strong profitability, the downside is its gross margins show its business model is much less lucrative than the best software businesses. On top of that, its low free cash flow margins give it little breathing room.

Wall Street analysts covering the company had a one-year price target of $23.71 right before these results (compared to the current share price of $22).

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.