E-commerce software platform provider BigCommerce (NASDAQ: BIGC) reported Q1 CY2024 results beating Wall Street analysts' expectations, with revenue up 12% year on year to $80.36 million. The company expects next quarter's revenue to be around $80.8 million, in line with analysts' estimates. It made a non-GAAP profit of $0.06 per share, improving from its loss of $0.30 per share in the same quarter last year.

BigCommerce (BIGC) Q1 CY2024 Highlights:

- Revenue: $80.36 million vs analyst estimates of $77.26 million (4% beat)

- EPS (non-GAAP): $0.06 vs analyst estimates of $0.04 ($0.02 beat)

- Revenue Guidance for Q2 CY2024 is $80.8 million at the midpoint, roughly in line with what analysts were expecting (operating income guidance for Q2 missed)

- The company reconfirmed its revenue guidance for the full year of $332.7 million at the midpoint, also in line (operating income guidance for 2024 ahead)

- Gross Margin (GAAP): 77.1%, up from 75.7% in the same quarter last year

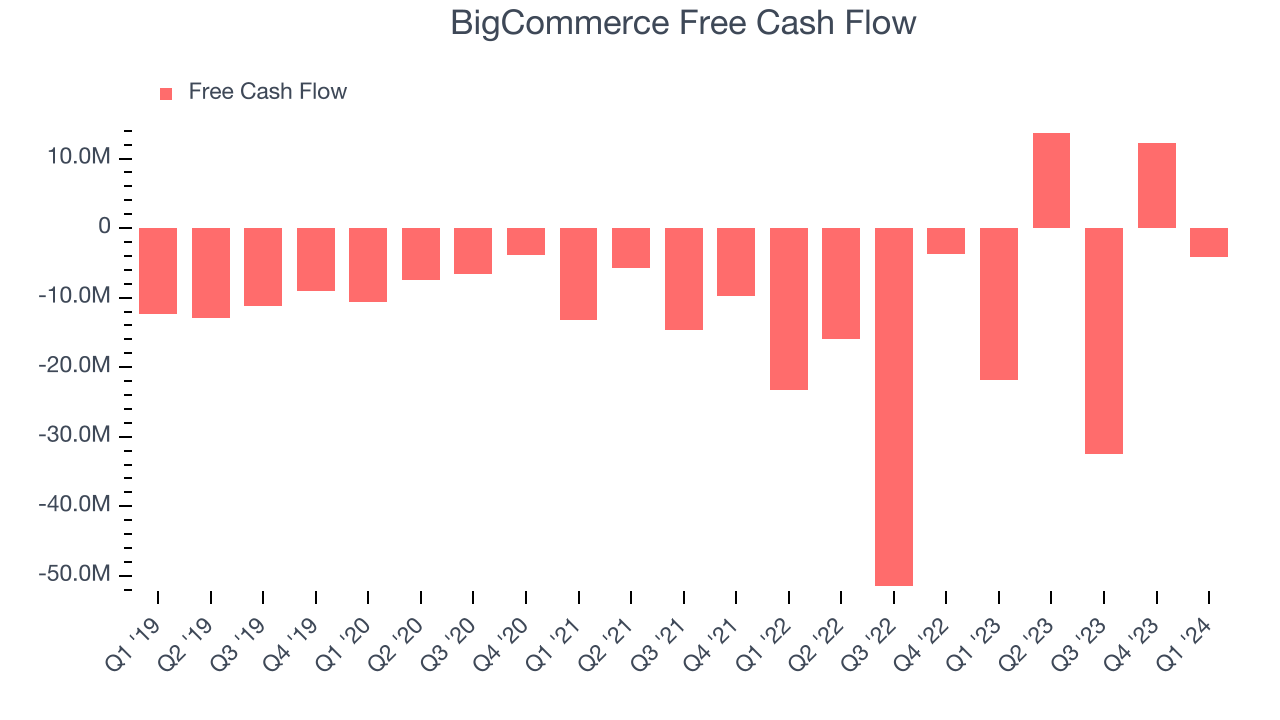

- Free Cash Flow was -$4.22 million, down from $12.24 million in the previous quarter

- Annual Recurring Revenue: $340.1 million at quarter end, up 7.4% year on year (in line)

- Market Capitalization: $513.8 million

Founded in Sydney, Australia in 2009 by Mitchell Harper and Eddie Machaalani, BigCommerce (NASDAQ:BIGC) provides software for businesses to easily create online stores.

Like Shopify, its platform includes tools to embed all the required functionality to host and design online shops. It provides modules to manage website features such as checkout, order management, reporting, and also third-party integrations for payment processing and tax management. It also provides cross-platform commerce by enabling its customers to link their online stores with top marketplaces around the world, such as Amazon, eBay, Facebook, and Instagram.

The e-commerce platform initially focused on providing cheap and simple solutions for small businesses. It has since evolved to also serve the needs of mid-sized companies and large enterprises. BigCommerce was able to meet the complex needs of large organizations via its open software approach to application development which has made it easy to integrate its software with third-party apps.

E-commerce Software

While e-commerce has been around for over two decades and enjoyed meaningful growth, its overall penetration of retail still remains low. Only around $1 in every $5 spent on retail purchases comes from digital orders, leaving over 80% of the retail market still ripe for online disruption. It is these large swathes of the retail where e-commerce has not yet taken hold that drives the demand for various e-commerce software solutions.

Competitors include Magento (an Adobe company), Salesforce Commerce Cloud (NYSE:CRM), Shopify (NYSE:SHOP), and WooCommerce.

Sales Growth

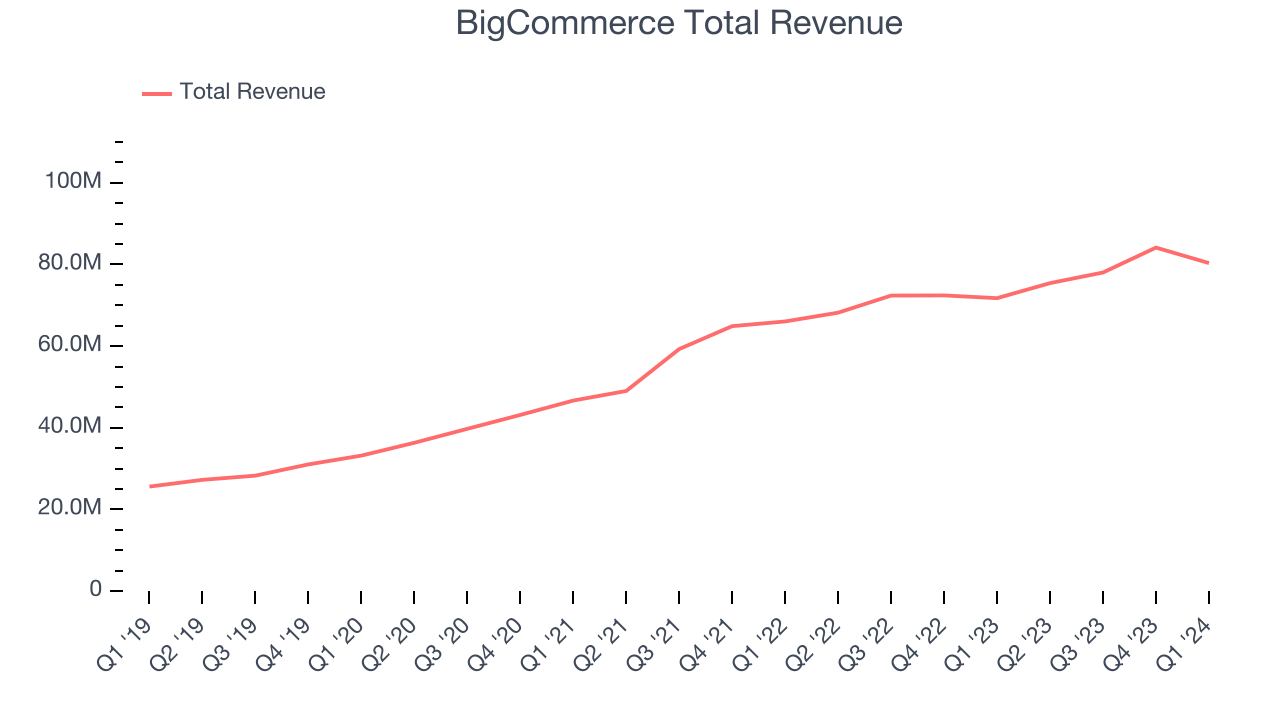

As you can see below, BigCommerce's revenue growth has been strong over the last three years, growing from $46.66 million in Q1 2021 to $80.36 million this quarter.

This quarter, BigCommerce's quarterly revenue was once again up 12% year on year. However, the company's revenue actually decreased by $3.79 million in Q1 compared to the $6.10 million increase in Q4 CY2023. Sales also dropped by a similar amount a year ago and management is guiding for revenue to rebound in the coming quarter, which might hint at an emerging seasonal pattern.

Next quarter's guidance suggests that BigCommerce is expecting revenue to grow 7.1% year on year to $80.8 million, slowing down from the 10.6% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 6.8% over the next 12 months before the earnings results announcement.

Profitability

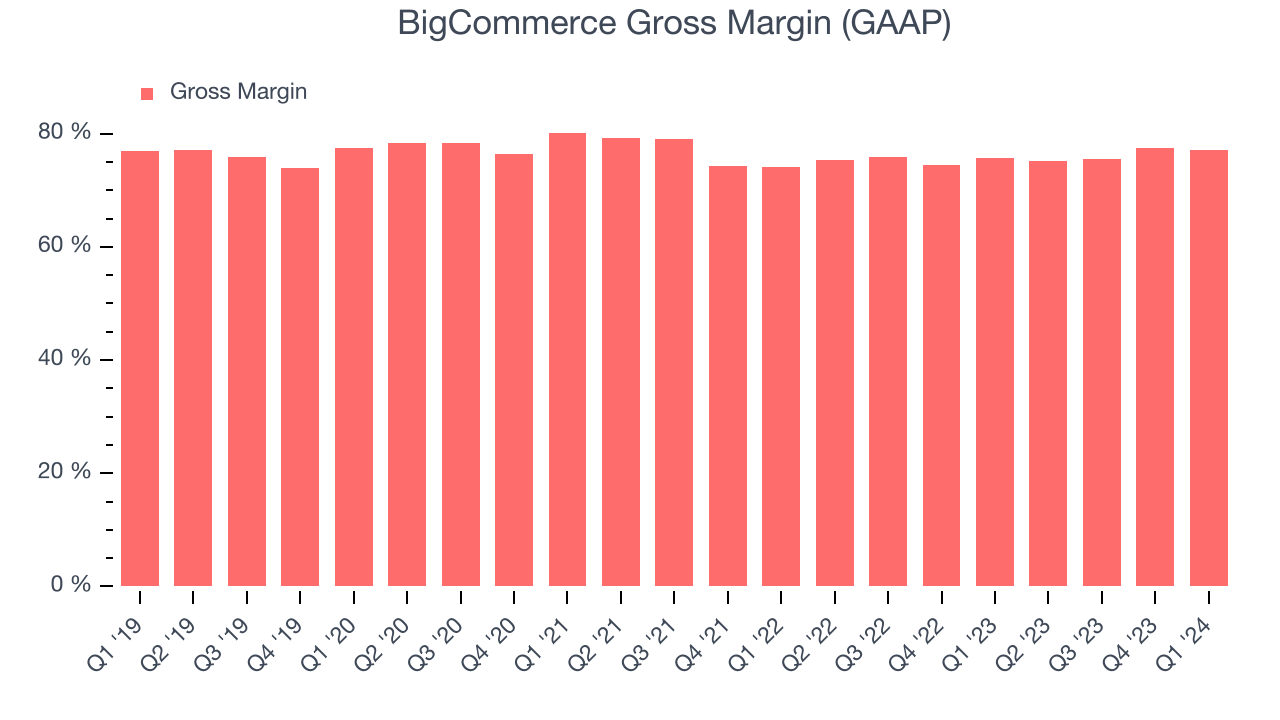

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. BigCommerce's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 77.1% in Q1.

That means that for every $1 in revenue the company had $0.77 left to spend on developing new products, sales and marketing, and general administrative overhead. BigCommerce's impressive gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity. It's also comforting to see its gross margin remain stable, indicating that BigCommerce is controlling its costs and not under pressure from its competitors to lower prices.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. BigCommerce burned through $4.22 million of cash in Q1 , increasing its cash burn by 80.7% year on year.

BigCommerce has burned through $10.75 million of cash over the last 12 months, resulting in a negative 3.4% free cash flow margin. This low FCF margin stems from BigCommerce's constant need to reinvest in its business to stay competitive.

Key Takeaways from BigCommerce's Q1 Results

It was good to see BigCommerce beat analysts' revenue expectations this quarter. However, ARR was only in line. Guidance was mixed, with revenue guidance for Q2 and the full year roughly in line while operating profit guidance for Q2 was slightly below expectations. Zooming out, we think this was a mixed quarter. The stock is flat after reporting and currently trades at $6.76 per share.

Is Now The Time?

When considering an investment in BigCommerce, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although BigCommerce isn't a bad business, it probably wouldn't be one of our picks. Although its revenue growth has been solid over the last three years, Wall Street expects growth to deteriorate from here. On top of that, its growth is coming at the cost of significant cash burn.

BigCommerce's price-to-sales ratio based on the next 12 months is 1.5x, suggesting the market has lower expectations for the business relative to the hottest tech stocks. In the end, beauty is in the eye of the beholder. While BigCommerce wouldn't be our first pick, if you like the business, it seems to be trading at an interesting price right now.

Wall Street analysts covering the company had a one-year price target of $9.50 right before these results (compared to the current share price of $6.76).

To get the best start with StockStory, check out our most recent Stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released. Especially for companies reporting pre-market, this often gives investors the chance to react to the results before everyone else has fully absorbed the information.