Booking (NASDAQ:BKNG) Reports Q1 In Line With Expectations But Stock Drops

Petr Huřťák /

May 4, 2023

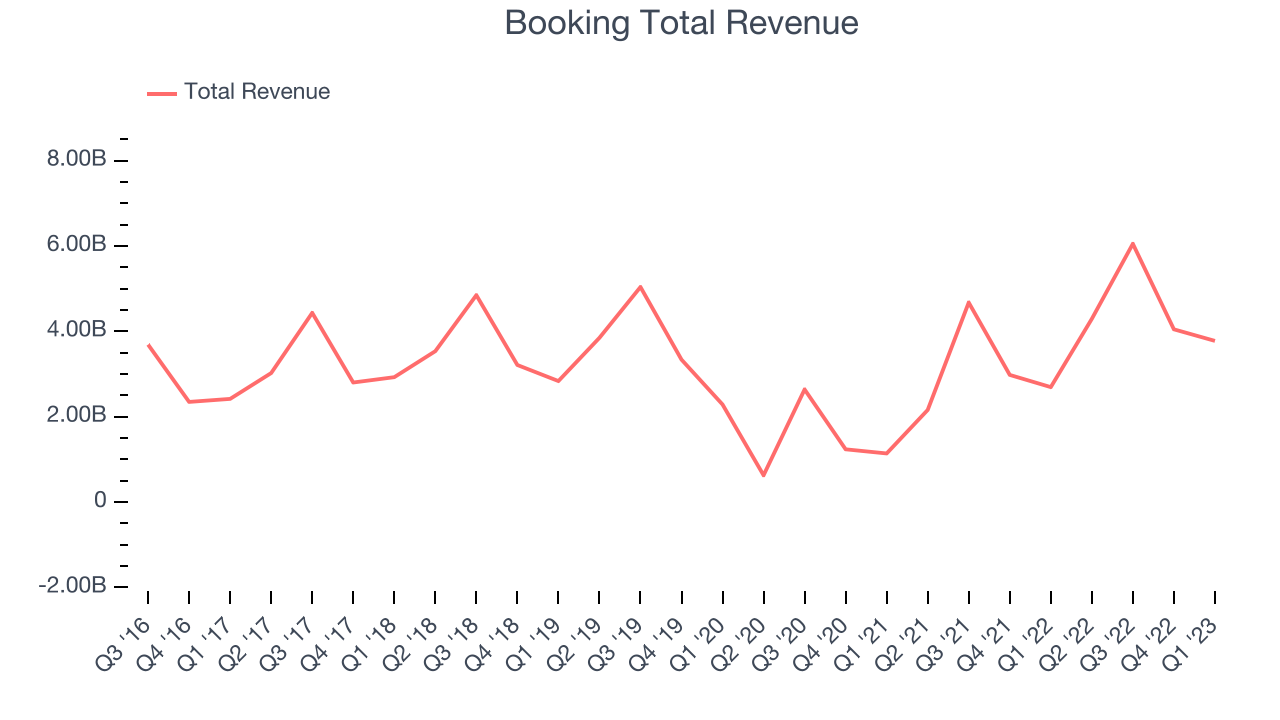

Online travel agency Booking Holdings (NASDAQ:BKNG) reported results in line with analyst expectations in Q1 FY2023 quarter, with revenue up 40.2% year on year to $3.78 billion. Booking made a GAAP profit of $266 million, improving on its loss of $700 million, in the same quarter last year.

Is now the time to buy Booking? Access our full analysis of the earnings results here, it's free.

Booking (BKNG) Q1 FY2023 Highlights:

- Revenue: $3.78 billion vs analyst estimates of $3.75 billion (0.87% beat)

- EPS (non-GAAP): $11.60 vs analyst estimates of $10.74 (8% beat)

- Free cash flow of $2.8 billion, up 33.5% from previous quarter

- Room Nights Booked: 274 million, up 76 million year on year

Formerly known as The Priceline Group, Booking Holdings (NASDAQ: BKNG) is the world’s largest online travel agency.

Because of the enormous number of flights, hotels, and accommodations available, travel is a natural fit for marketplaces that aggregate suppliers, simplifying the shopping process for consumers. Online travel platforms today make up over 50% of the industry’s bookings, a percentage that has been rising for 20 years, and will likely continue in the years ahead.

Sales Growth

Booking's revenue growth over the last three years has been impressive, averaging 46.4% annually. This quarter, Booking reported an excellent 40.2% year on year revenue growth, roughly in line with what analysts expected.

Ahead of the earnings results the analysts covering the company were estimating sales to grow 12.1% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Usage Growth

As an online travel company, Booking generates revenue growth by a combination of increasing the number of stays (or experiences) booked, as well as the level of commission charged on those bookings.

Over the last two years the number of Booking's nights booked, a key usage metric for the company, grew 109% annually to 274 million. This is among the fastest growth of any consumer internet company, indicating that users are excited about the offering.

In Q1 the company added 76 million nights booked, translating to a 38.4% growth year on year.

Key Takeaways from Booking's Q1 Results

With a market capitalization of $98.2 billion, more than $14.5 billion in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

We were very impressed by Booking’s strong user growth this quarter. And we were also excited to see the really strong revenue growth, and all units sold (room nights, airline tickets, rental car days) exceeded expectations. However, operating income missed. The company did not issue guidance. Zooming out, we think this was a solid quarter, but the market might have been expecting more and the company is down 5.35% on the results and currently trades at $2,463.19 per share.

Booking may have had a good quarter, so should you invest right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.