Braze (NASDAQ:BRZE) Exceeds Q2 Expectations, Gross Margin Improves

Jabin Bastian /

September 5, 2024

Customer engagement software provider Braze (NASDAQ:BRZE) reported results ahead of analysts’ expectations in Q2 CY2024, with revenue up 26.4% year on year to $145.5 million. The company expects next quarter’s revenue to be around $148 million, in line with analysts’ estimates. It made a non-GAAP profit of $0.09 per share, improving from its loss of $0.04 per share in the same quarter last year.

Is now the time to buy Braze? Find out in our full research report.

Braze (BRZE) Q2 CY2024 Highlights:

- Revenue: $145.5 million vs analyst estimates of $141.3 million (3% beat)

- Adjusted Operating Income: $4.17 million vs analyst estimates of -$6.91 million (160% beat)

- EPS (non-GAAP): $0.09 vs analyst estimates of -$0.03 ($0.12 beat)

- The company slightly lifted its revenue guidance for the full year to $584 million at the midpoint from $579 million

- EPS (non-GAAP) guidance for the full year is $0.07 at the midpoint, beating analyst estimates by 195%

- Gross Margin (GAAP): 70.2%, in line with the same quarter last year

- Free Cash Flow Margin: 5%, down from 8.4% in the previous quarter

- Net Revenue Retention Rate: 114%, down from 117% in the previous quarter

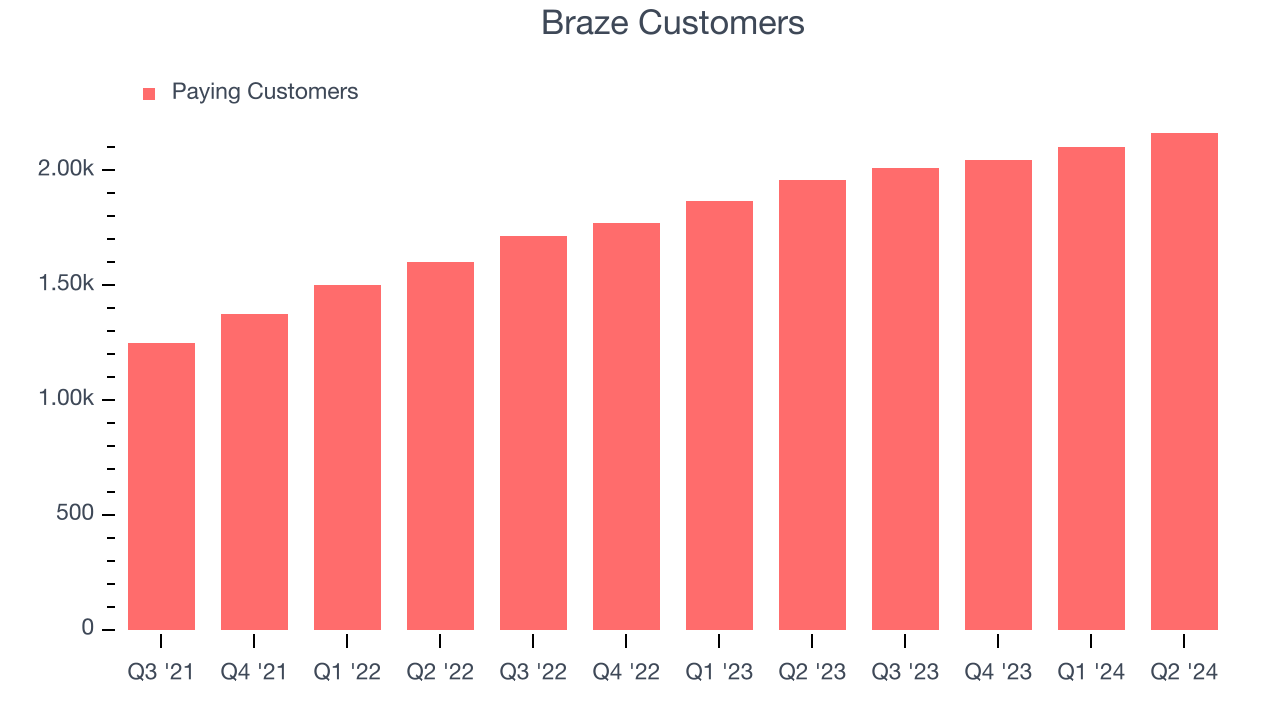

- Customers: 2,163, up from 2,102 in the previous quarter

- Billings: $128 million at quarter end, up 15.7% year on year

- Market Capitalization: $4.39 billion

“We delivered a great second quarter, demonstrating strong top-line growth while driving efficiency in our business, achieving our first quarter of non-GAAP operating income profitability and non-GAAP net income profitability. Our results demonstrate our effective execution and continued demand for the Braze Customer Engagement Platform,” said Bill Magnuson, cofounder and CEO of Braze.

Founded in 2011 after the co-founders met at NYC Disrupt Hackathon, Braze (NASDAQ:BRZE) is a customer engagement software platform that allows brands to connect with customers through data-driven and contextual marketing campaigns.

Marketing Software

Whether or not companies market their products through social media, all businesses need to meet customers where they are; and increasingly, that is social media. As more and more people use a greater number of social media platforms, social media management software become more valuable to their customers.

Sales Growth

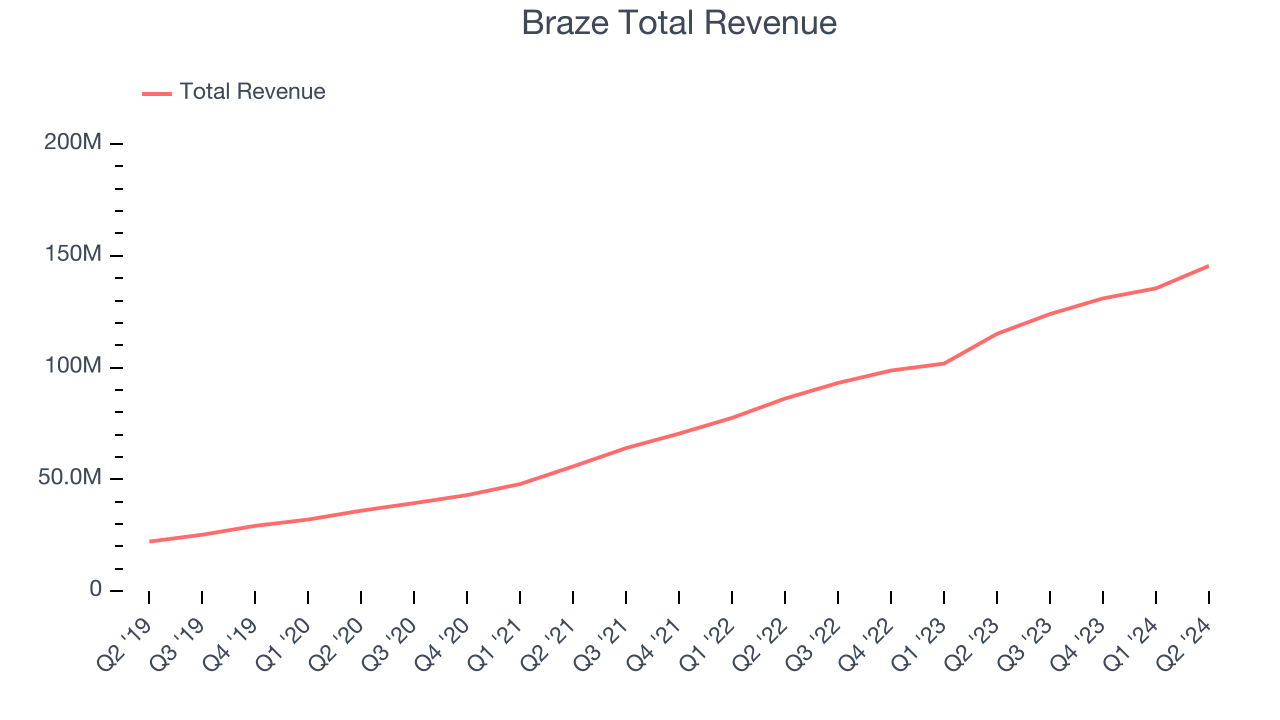

As you can see below, Braze’s 42.3% annualized revenue growth over the last three years has been incredible, and its sales came in at $145.5 million this quarter.

This quarter, Braze’s quarterly revenue was once again up a very solid 26.4% year on year. On top of that, its revenue increased $10.04 million quarter on quarter, a very strong improvement from the $4.50 million increase in Q1 CY2024. This is a sign of acceleration of growth and great to see.

Next quarter’s guidance suggests that Braze is expecting revenue to grow 19.4% year on year to $148 million, slowing down from the 33.1% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 18.6% over the next 12 months before the earnings results announcement.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Customer Growth

Braze reported 2,163 customers at the end of the quarter, an increase of 61 from the previous quarter. That’s in line with the customer growth we’ve observed over the last couple of quarters, suggesting that the company can maintain its current sales momentum.

Key Takeaways from Braze’s Q2 Results

We were glad Braze's revenue, adjusted operating income, and EPS outperformed Wall Street’s estimates. It was also good to see its full-year revenue and EPS guidance top expectations. On the other hand, its billings unfortunately missed and its net revenue retention decreased. Overall, this was a mixed quarter, and the market seems to be homing in on the negatives. The stock traded down 2.7% to $43 immediately following the results.

Braze may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.