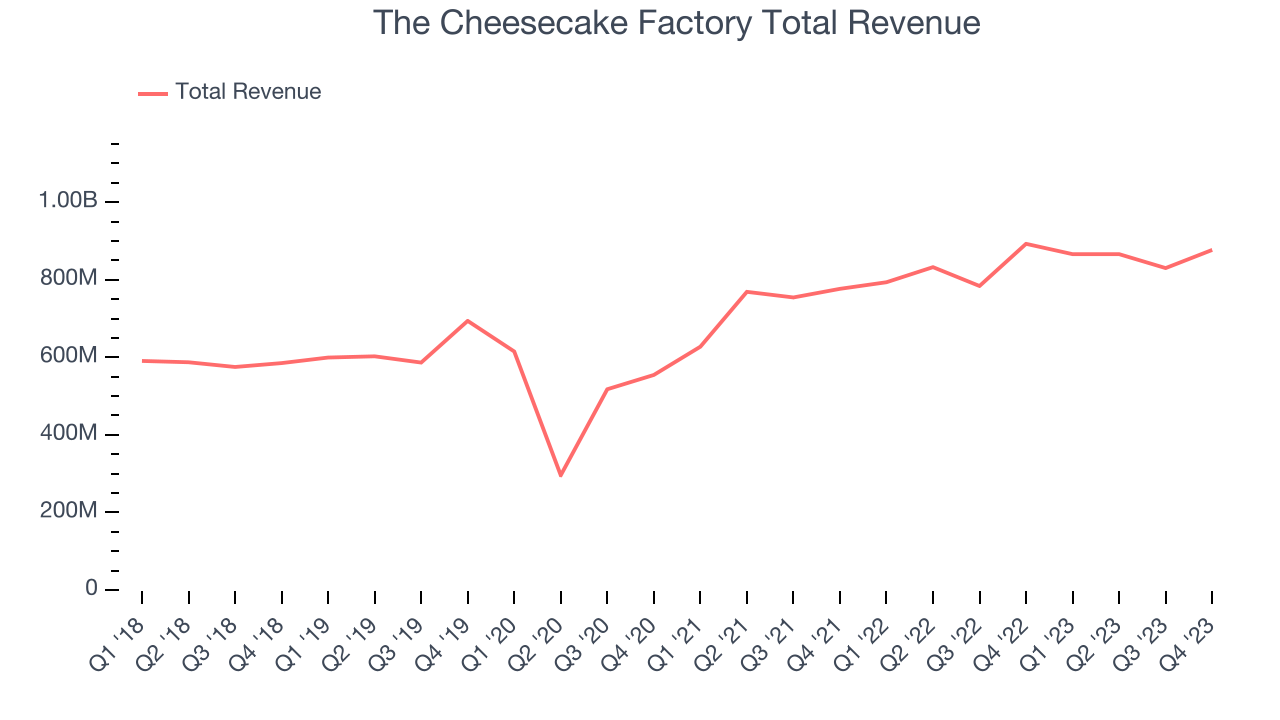

Restaurant company Cheesecake Factory (NASDAQ:CAKE) reported results in line with analysts' expectations in Q4 FY2023, with revenue down 1.8% year on year to $877 million. It made a non-GAAP profit of $0.80 per share, improving from its profit of $0.56 per share in the same quarter last year.

The Cheesecake Factory (CAKE) Q4 FY2023 Highlights:

- Revenue: $877 million vs analyst estimates of $876.2 million (small beat)

- EPS (non-GAAP): $0.80 vs analyst estimates of $0.73 (9.5% beat)

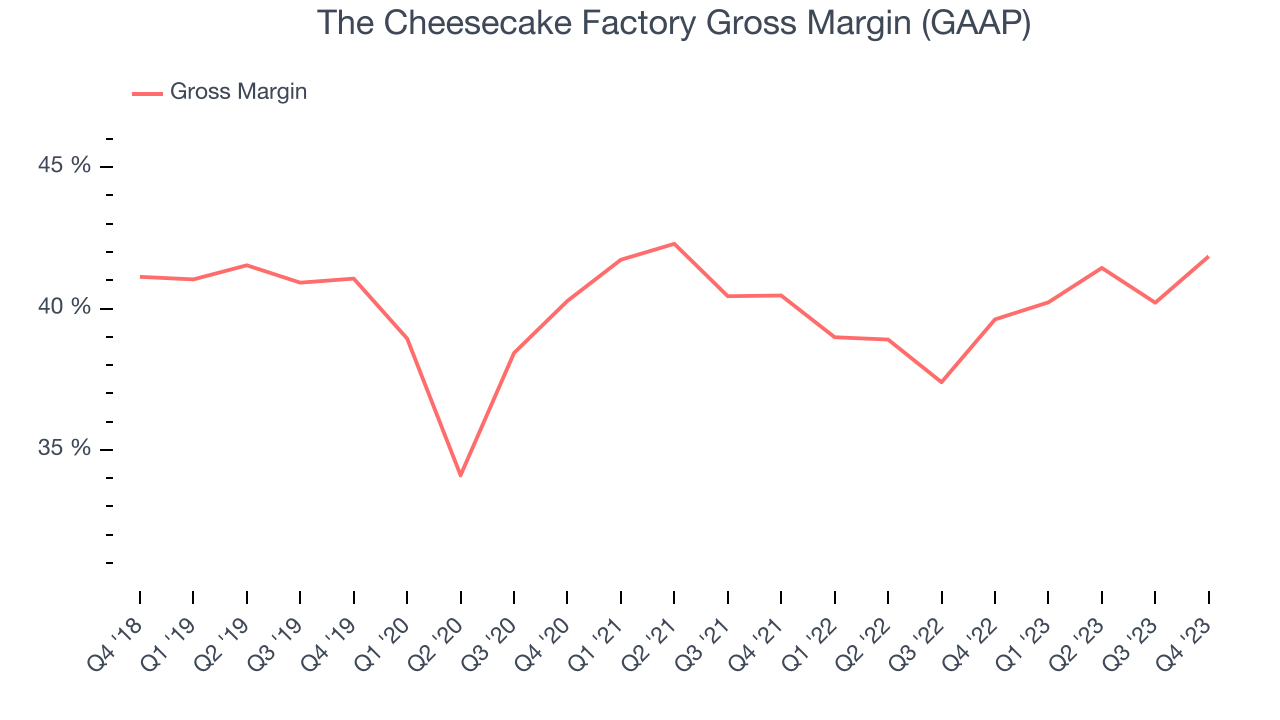

- Gross Margin (GAAP): 41.8%, up from 39.6% in the same quarter last year

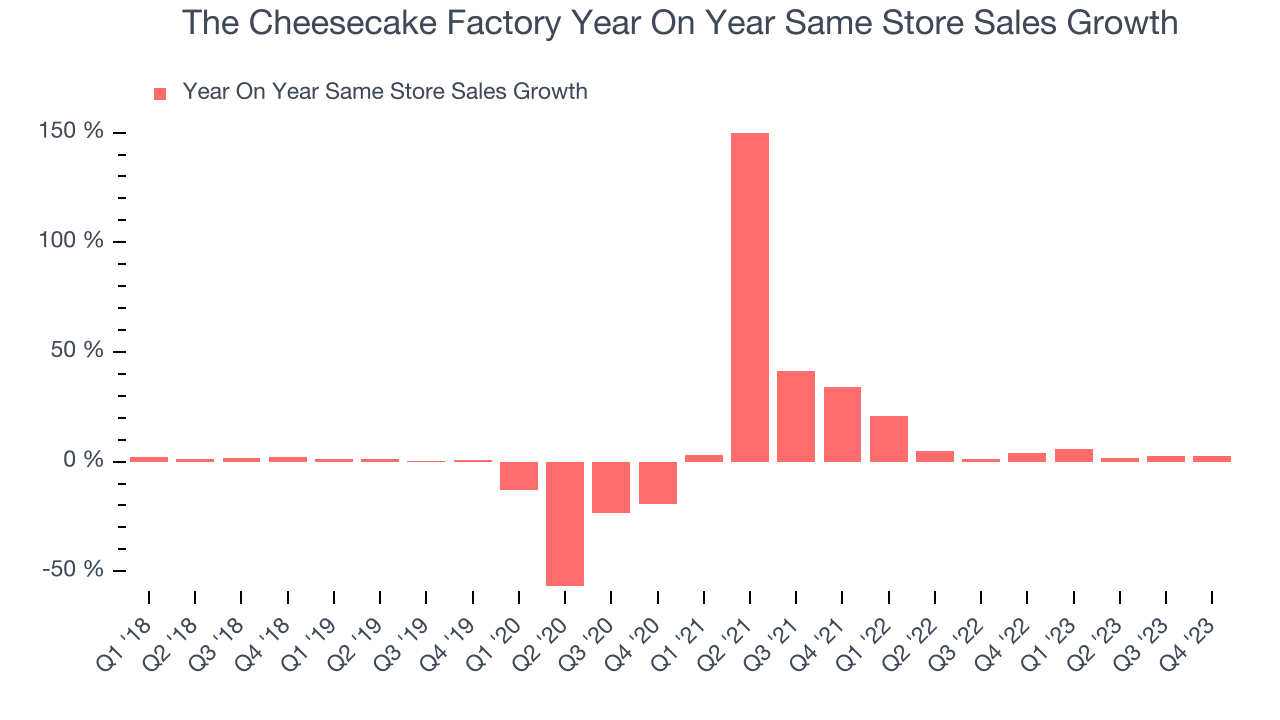

- Same-Store Sales were up 2.5% year on year

- Store Locations: 331 at quarter end, decreasing by 17 over the last 12 months

- Market Capitalization: $1.76 billion

Celebrated for its delicious (and free) brown bread, gigantic portions, and delectable desserts, Cheesecake Factory (NASDAQ:CAKE) is an iconic American restaurant chain that also owns and operates a portfolio of separate restaurant brands.

Cheesecake Factory’s origins trace back to 1972 when founder David Overton opened The Cheesecake Factory Bakery, where he produced cheesecakes and other desserts for local restaurants. The company was officially founded when David opened his first restaurant in Beverly Hills, California, expanding its menu to include sandwiches and salads.

Since its humble beginnings, Cheesecake Factory has stretched its menu (typically over 21 pages) to accommodate a wide range of tastes and preferences. Diners can indulge in anything from the Macaroni and Cheese Burger to Shrimp and Chicken Gumbo or even Orange Chicken. Most importantly, there are now over 40 different types of cheesecake creations to choose from, including Ultimate Red Velvet and Chocolate Caramelicious.

As Cheesecake Factory has grown to include over 200 locations across the United States, it’s also used its profits to acquire complementary restaurant banners. These include Italian eatery North Italia, upscale American-inspired Grand Lux Cafe, and holding company Fox Restaurant Concepts, which owns over 10 unique restaurant chains.

The target market for restaurants in the Cheesecake Factory family is suburban areas, and each is designed to create an inviting ambiance for its guests regardless of the occasion.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Multi-brand full-service restaurant competitors include Bloomin’ Brands (NASDAQ:BLMN), Brinker International (NYSE:EAT), Darden (NYSE:DRI), Dine Brands (NYSE:DIN), and Texas Roadhouse (NASDAQ:TXRH).Sales Growth

The Cheesecake Factory is one of the larger restaurant chains in the industry and benefits from a strong brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 8.5% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new restaurants and grew sales at existing, established dining locations.

This quarter, The Cheesecake Factory reported a rather uninspiring 1.8% year-on-year revenue decline to $877 million in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 6.4% over the next 12 months, an acceleration from this quarter.

Number of Stores

When a chain like The Cheesecake Factory is opening new restaurants, it usually means it's investing for growth because there's healthy demand for its meals and there are markets where the concept has few or no locations. The last 12 months have been an exception, however, as The Cheesecake Factory closed 17 locations, bringing its total restaurant count to 331 in the most recently reported quarter.

Over the last two years, The Cheesecake Factory has opened new restaurants and averaged 2.3% annual growth in new locations, higher than other restaurant businesses. Comparisons, however, should be taken with a grain of salt as the industry is quite mature. Analyzing a restaurant's location growth is important because expansion means The Cheesecake Factory has more opportunities to feed customers and generate sales.

Same-Store Sales

The Cheesecake Factory's demand within its existing restaurants has generally risen over the last two years but lagged behind the broader sector. On average, the company's same-store sales have grown by 5.4% year on year. With positive same-store sales growth amid an increasing number of restaurants, The Cheesecake Factory is reaching more diners and growing sales.

In the latest quarter, The Cheesecake Factory's same-store sales rose 2.5% year on year. This growth was a deceleration from the 4.1% year-on-year increase it posted 12 months ago, showing the business is still performing well but lost a bit of steam.

Gross Margin & Pricing Power

Gross profit margins tell us how much money a restaurant gets to keep after paying for the direct costs of the meals it sells.

The Cheesecake Factory's gross profit margin came in at 41.8% this quarter. up 2.2 percentage points year on year. This means the company makes $0.40 for every $1 in revenue before accounting for its operating expenses.

The Cheesecake Factory has great unit economics for a restaurant company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see above, it's averaged an impressive 39.9% gross margin over the last eight quarters. Its margin has also been trending up over the last 12 months, averaging 5.7% year-on-year increases each quarter. If this trend continues, it could suggest a less competitive environment where the company has better pricing power and more stable input costs (such as ingredients and transportation expenses).

Operating Margin

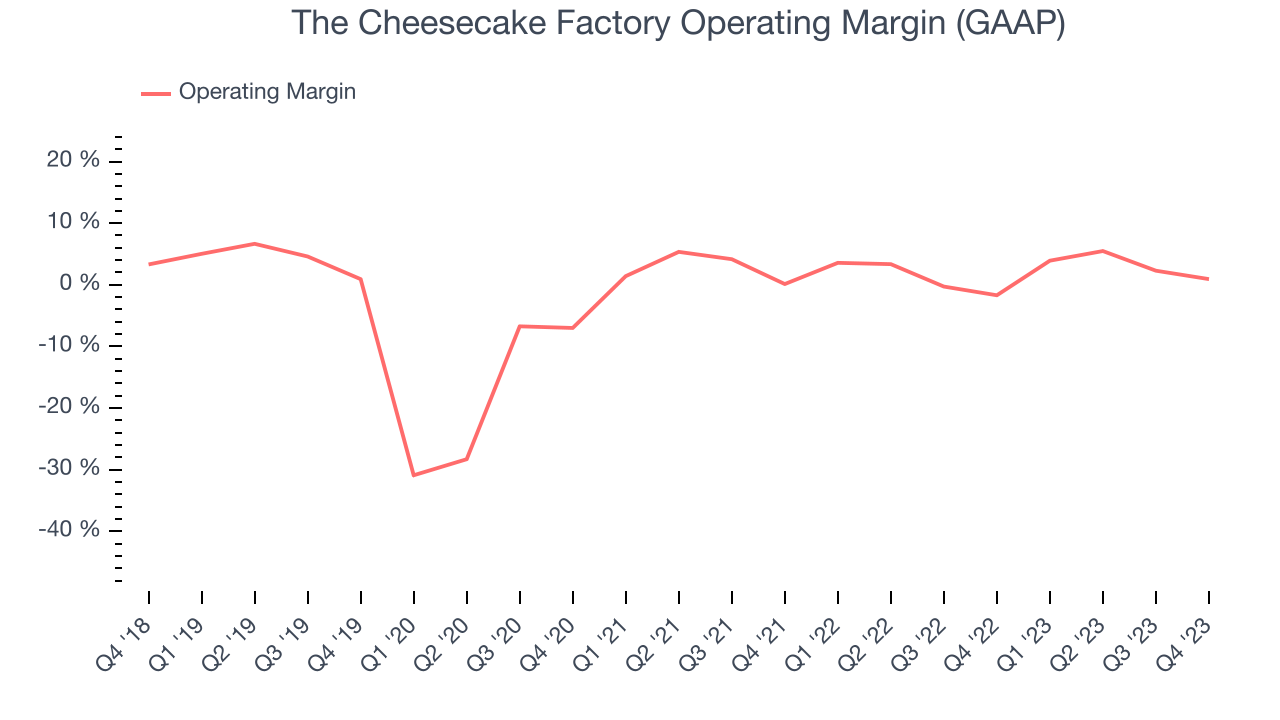

Operating margin is an important measure of profitability for restaurants as it accounts for all expenses keeping the lights on, including wages, rent, advertising, and other administrative costs.

In Q4, The Cheesecake Factory generated an operating profit margin of 0.9%, up 2.6 percentage points year on year. This increase was encouraging, and we can infer The Cheesecake Factory was more disciplined with its expenses or gained leverage on its fixed costs because its operating margin expanded more than its gross margin.

Zooming out, The Cheesecake Factory was profitable over the last two years but held back by its large expense base. Its average operating margin of 2.2% has been paltry for a restaurant business. However, The Cheesecake Factory's margin has improved, on average, by 2 percentage points each year, an encouraging sign for shareholders. The tide could be turning.

Zooming out, The Cheesecake Factory was profitable over the last two years but held back by its large expense base. Its average operating margin of 2.2% has been paltry for a restaurant business. However, The Cheesecake Factory's margin has improved, on average, by 2 percentage points each year, an encouraging sign for shareholders. The tide could be turning.EPS

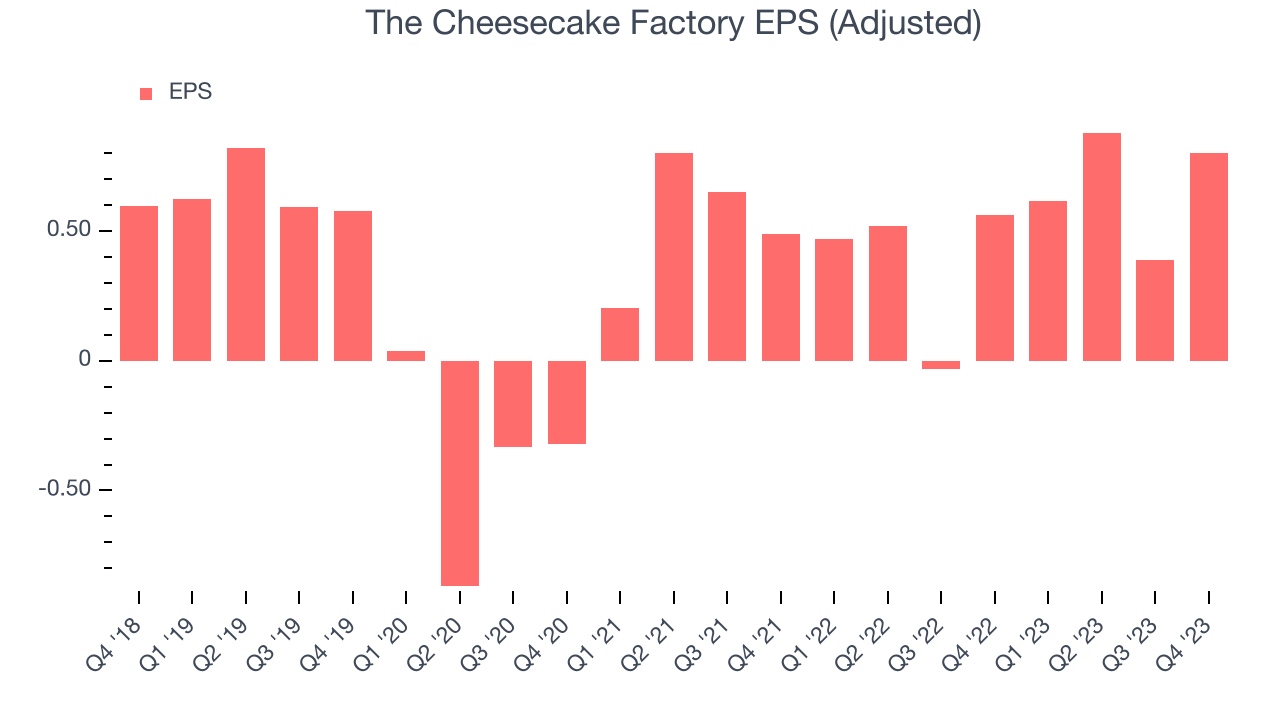

These days, some companies issue new shares like there's no tomorrow. That's why we like to track earnings per share (EPS) because it accounts for shareholder dilution and share buybacks.

In Q4, The Cheesecake Factory reported EPS at $0.80, up from $0.56 in the same quarter a year ago. This print beat Wall Street's estimates by 9.5%.

Between FY2019 and FY2023, The Cheesecake Factory's adjusted diluted EPS grew 2.7%, translating into a weak 0.7% compounded annual growth rate.

On the bright side, Wall Street expects the company to continue growing earnings over the next 12 months, with analysts projecting an average 12.7% year-on-year increase in EPS.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

The Cheesecake Factory's five-year average ROIC was 3%, somewhat low compared to the best restaurant companies that consistently pump out 15%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last two years, The Cheesecake Factory's ROIC averaged 28.2 percentage point increases each year. This is a good sign and we hope the company can continue to improving.

Key Takeaways from The Cheesecake Factory's Q4 Results

We were impressed by how significantly The Cheesecake Factory blew past analysts' gross margin expectations this quarter. We were also happy its EPS narrowly outperformed Wall Street's estimates. Although its same-store sales growth of 2.5% wasn't anything to write home about, the company opened 9 new company-owned restaurants (three Cheesecake Factories, three North Italias, three FRCs) and opened two Cheesecake Factory restaurants in China and Thailand under licensing agreements. Since 12/31/23, The Cheesecake Factory has also opened four new Cheesecake Factory restaurants under licensing agreements in Mexico. Overall, we think this was a really good quarter that should please shareholders. The stock is up 1.9% after reporting and currently trades at $34.88 per share.

Is Now The Time?

The Cheesecake Factory may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of The Cheesecake Factory, we'll be cheering from the sidelines. Although its revenue growth has been decent over the last four years, its relatively low ROIC suggests it has struggled to grow profits historically. And while its gross margins are a strong starting point for the overall profitability of the business, the downside is its operating margins reveal poor profitability compared to other restaurants.

The Cheesecake Factory's price-to-earnings ratio based on the next 12 months is 11.3x. While we've no doubt one can find things to like about The Cheesecake Factory, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $34.93 per share right before these results (compared to the current share price of $34.88).

To get the best start with StockStory, check out our most recent stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.