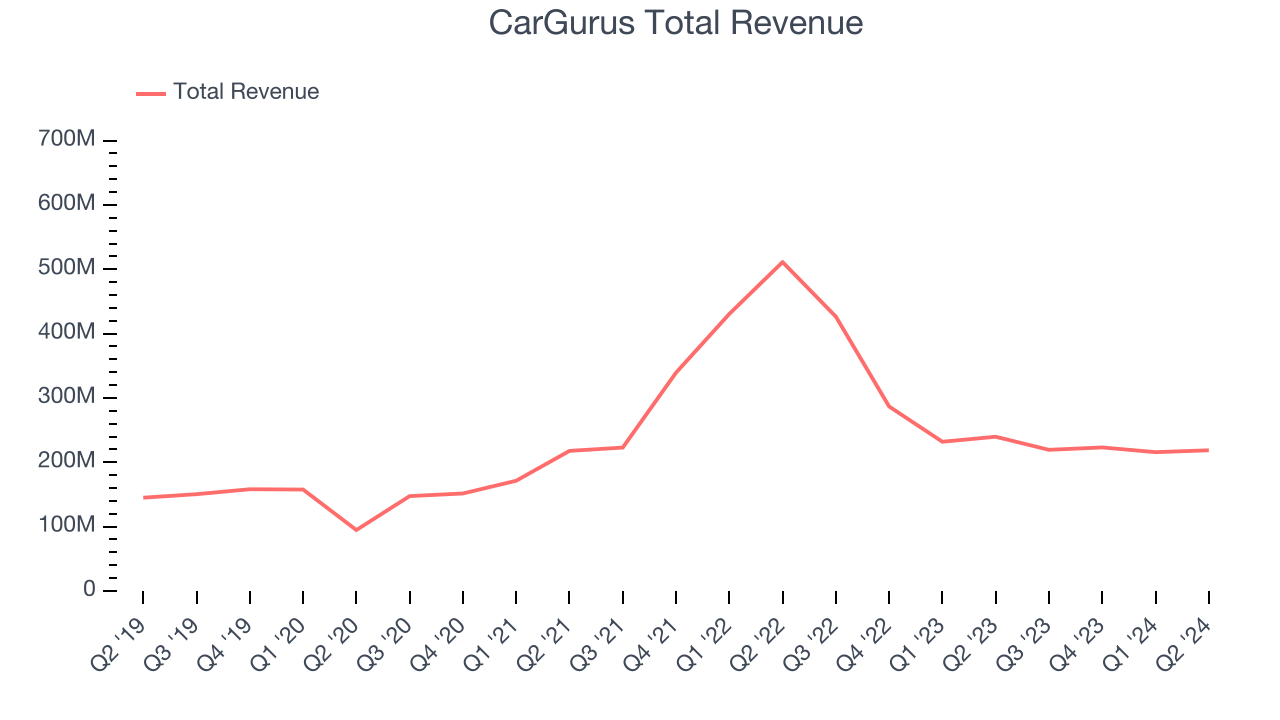

Online auto marketplace CarGurus (NASDAQ:CARG) reported Q2 CY2024 results beating Wall Street analysts' expectations, with revenue down 8.8% year on year to $218.7 million. The company expects next quarter's revenue to be around $222 million, in line with analysts' estimates. It made a GAAP loss of $0.66 per share, down from its profit of $0.12 per share in the same quarter last year.

Is now the time to buy CarGurus? Find out by accessing our full research report, it's free.

CarGurus (CARG) Q2 CY2024 Highlights:

- Revenue: $218.7 million vs analyst estimates of $215.7 million (1.4% beat)

- Adjusted EBITDA: $55.6 million vs analyst estimates of $52.5 million (5.9% beat)

- EPS: -$0.66 vs analyst estimates of $0.20 (-$0.86 miss)

- Revenue Guidance for Q3 CY2024 is $222 million at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 83.4%, up from 68.5% in the same quarter last year

- EBITDA Margin: 25.4%, up from 18.2% in the same quarter last year

- Free Cash Flow of $40.37 million, up 126% from the previous quarter

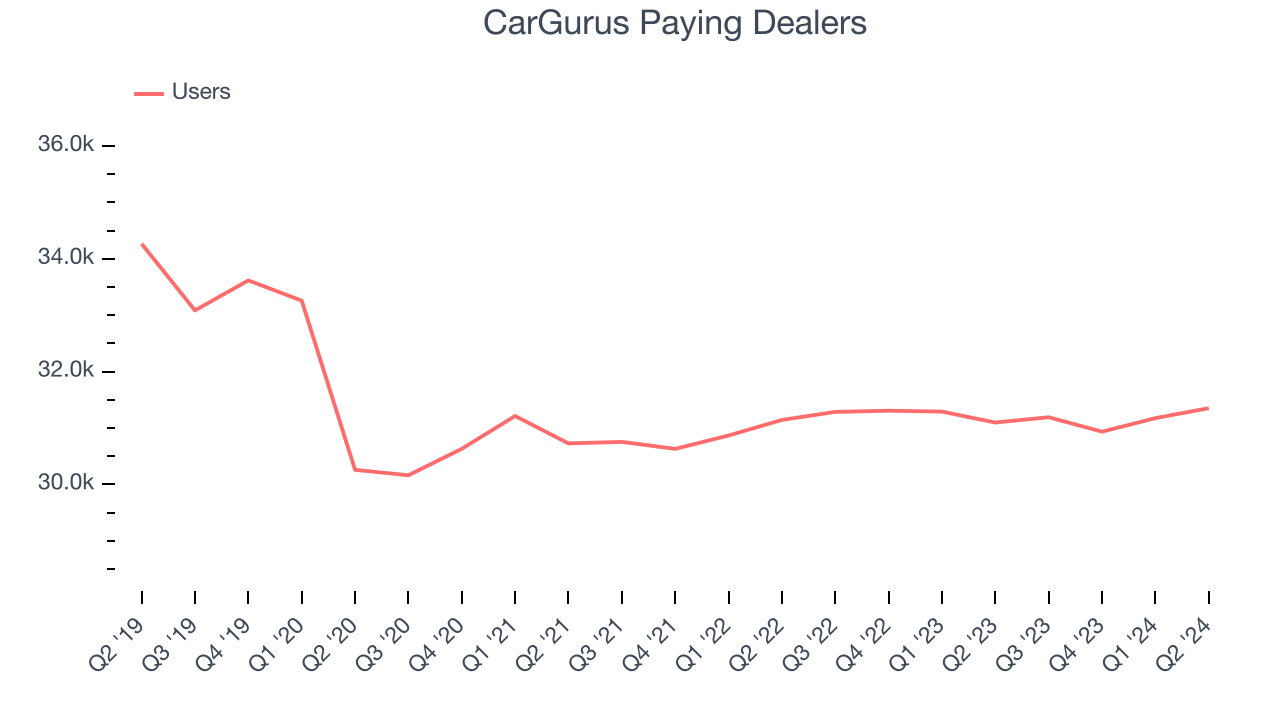

- Paying Dealers: 31,352, in line with the same quarter last year

- Market Capitalization: $2.30 billion

“Our Marketplace business continued to accelerate, achieving the largest quarterly revenue increase since 2021, driven by higher adoption of add-on products, continued migration toward premium subscription tiers, and expansion in our global paying dealer base,” said Jason Trevisan, Chief Executive Officer at CarGurus.

Bringing transparency to a sometimes opaque process, CarGurus (NASDAQ:CARG) is a digital marketplace where auto dealers can connect with potential customers and where car buyers can browse, purchase, and obtain financing.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Sales Growth

CarGurus's revenue growth over the last three years has been strong, averaging 29.3% annually. This quarter, CarGurus beat analysts' estimates but reported a year on year revenue decline of 8.8%.

Guidance for the next quarter indicates CarGurus is expecting revenue to grow 1.2% year on year to $222 million, improving from the 48.5% year-on-year decline it recorded in the comparable quarter last year. Ahead of the earnings results, analysts were projecting sales to grow 4.4% over the next 12 months.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Usage Growth

As an online marketplace, CarGurus generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, CarGurus's users, a key performance metric for the company, grew 0.5% annually to 31,352. This is one of the lowest rates of growth in the consumer internet sector.

In Q2, CarGurus added 255 users, translating into 0.8% year-on-year growth.

Revenue Per User

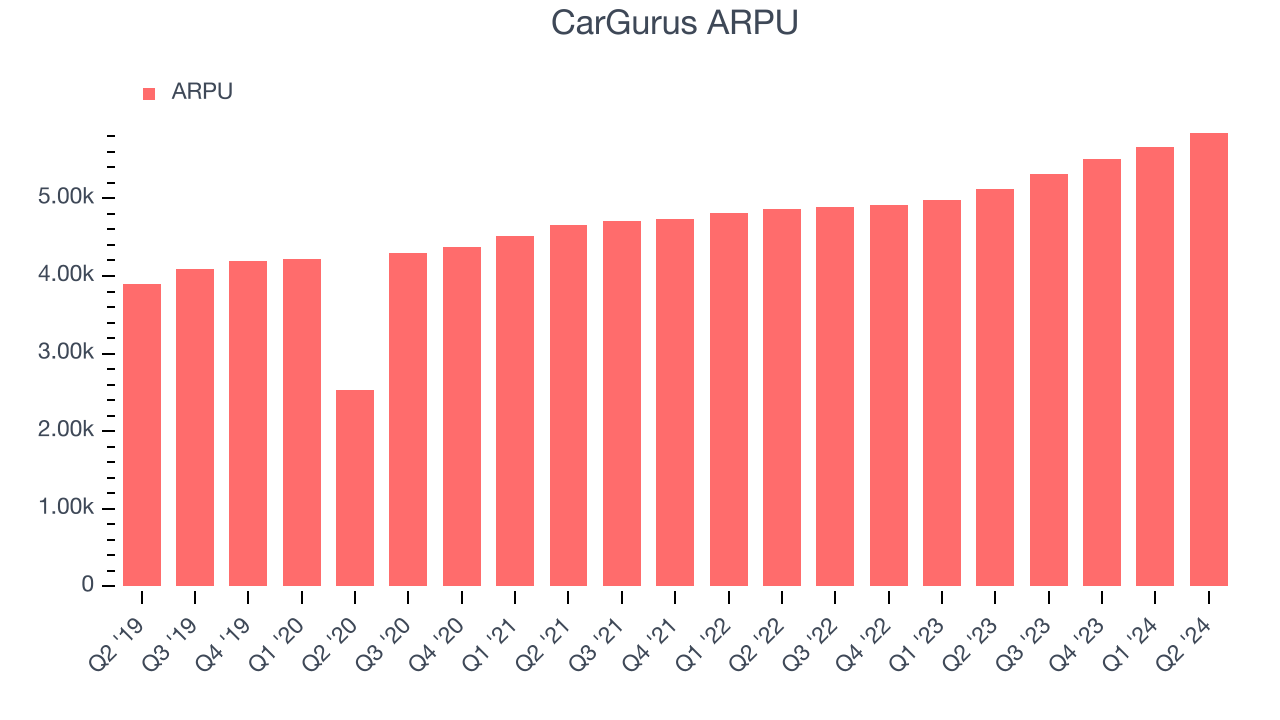

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like CarGurus because it measures how much the company earns in transaction fees from each user. Furthermore, ARPU gives us unique insights as it's a function of a user's average order size and CarGurus's take rate, or "cut", on each order.

CarGurus's ARPU growth has been decent over the last two years, averaging 8.1%. The company's ability to increase prices while growing its users demonstrates the value of its platform. This quarter, ARPU grew 14.3% year on year to $5,848 per user.

Key Takeaways from CarGurus's Q2 Results

It was good to see CarGurus narrowly top analysts' revenue and adjusted EBITDA expectations this quarter. We were also glad next quarter's revenue guidance came in higher than Wall Street's estimates. Overall, this was a solid quarter for CarGurus. The stock traded up 2.7% to $23.01 immediately after reporting.

So should you invest in CarGurus right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.