Semiconductor design software provider Cadence Design Systems (NASDAQ:CDNS) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 18.8% year on year to $1.07 billion. On the other hand, next quarter's revenue guidance of $1 billion was less impressive, coming in 8.5% below analysts' estimates. It made a non-GAAP profit of $1.38 per share, improving from its profit of $0.96 per share in the same quarter last year.

Cadence (CDNS) Q4 FY2023 Highlights:

- Revenue: $1.07 billion vs analyst estimates of $1.06 billion (small beat)

- EPS (non-GAAP): $1.38 vs analyst estimates of $1.33 (3.7% beat)

- Revenue Guidance for Q1 2024 is $1 billion at the midpoint, below analyst estimates of $1.09 billion

- Management's revenue guidance for the upcoming financial year 2024 is $4.58 billion at the midpoint, in line with analyst expectations and implying 12% growth (vs 14.8% in FY2023)

- Free Cash Flow of $238.4 million, down 36.2% from the previous quarter

- Gross Margin (GAAP): 90.3%, in line with the same quarter last year

- Market Capitalization: $84.87 billion

With the name chosen to reflect the idea of a repeating pattern or rhythm in electronic design, Cadence Design Systems (NASDAQ:CDNS) offers a software-as-a-service platform for semiconductor engineering and design.

Known as an electronic design automation (EDA) software platform, Cadence helps engineers design semiconductors and test them through simulation. The company's flagship product is the Cadence Encounter digital implementation system, which provides a complete set of tools such as logic synthesis, placement and routing, and timing optimization. Logic synthesis converts electronic designs into detailed digital circuit implementations. Placement and timing tools determine the physical locations of components to meet design constraints. Timing optimization ensures the digital circuit meets the required performance metrics.

As chips become smaller and more densely packed with transistors, it becomes harder to design and optimize them. Cadence's tools address these challenges by automating many of the design and optimization tasks, which lets engineers to focus on higher-level decisions. Simulation capabilities means testing can be done before final production to identify and correct defects or inefficiencies, which saves time/resources and improves time to market.

Cadence principally generates revenue by selling software seat licenses, usually based on number of users in a customer’s organization. In addition, the company generates a smaller portion of revenue from consulting and support services to ensure that customers succeed with the company’s software suite.

Design Software

The demand for rich, interactive 2D, 3D, VR and AR experiences is growing, and while the ubiquitous metaverse might still be more of a buzzword than a real thing, what is real is the demand for the tools to create these experiences, whether they are games, 3D tours or interactive movies.

Competitors in engineering and design software include Ansys (NASDAQ:ANSS), Synopsys (NASDAQ:SNPS), and Siemens EDA (subsidiary of XTRA:SIE).Sales Growth

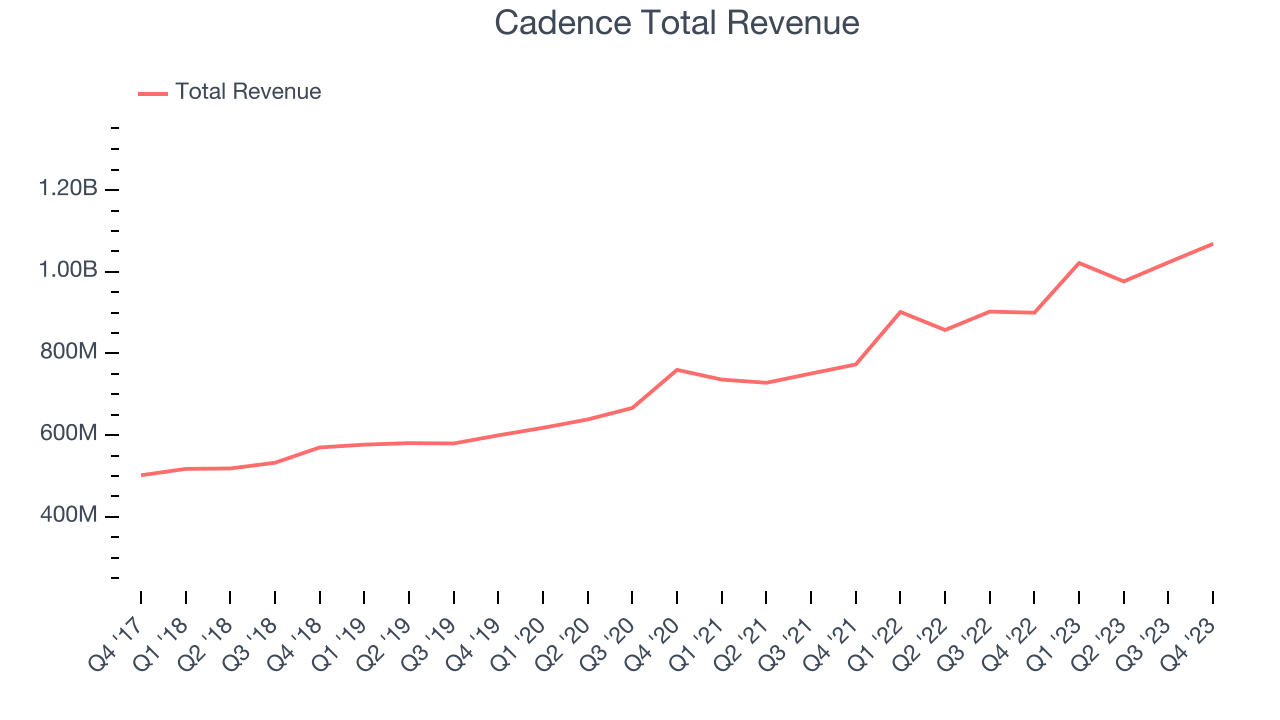

As you can see below, Cadence's revenue growth has been mediocre over the last two years, growing from $773 million in Q4 FY2021 to $1.07 billion this quarter.

This quarter, Cadence's quarterly revenue was once again up 18.8% year on year. We can see that Cadence's revenue increased by $45.53 million in Q4, which was roughly the same growth rate observed in Q3 2023. This steady quarter-on-quarter growth shows that the company can maintain its paced growth trajectory.

Next quarter, Cadence is guiding for a 2.1% year-on-year revenue decline to $1 billion, a further deceleration from the 13.3% year-on-year decrease it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $4.58 billion at the midpoint, growing 12% year on year compared to the 14.8% increase in FY2023.

Profitability

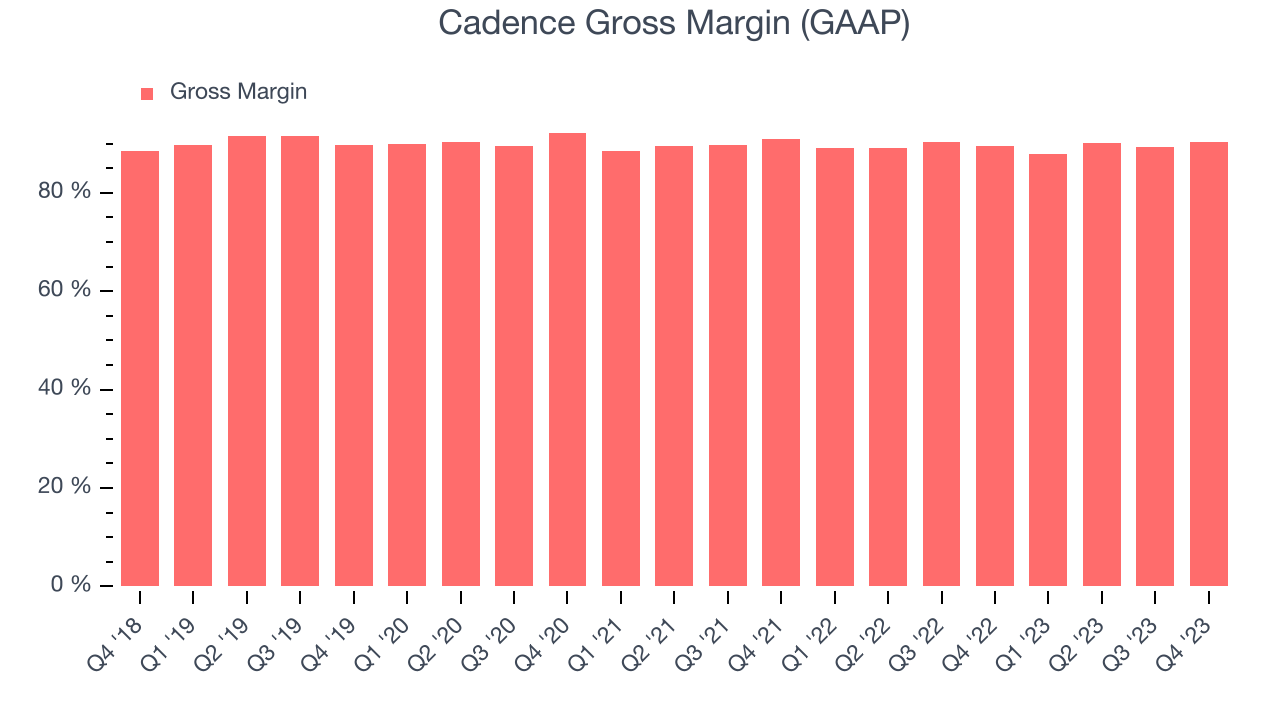

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Cadence's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 90.3% in Q4.

That means that for every $1 in revenue the company had $0.90 left to spend on developing new products, sales and marketing, and general administrative overhead. Significantly up from the last quarter, Cadence's excellent gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity.

Cash Is King

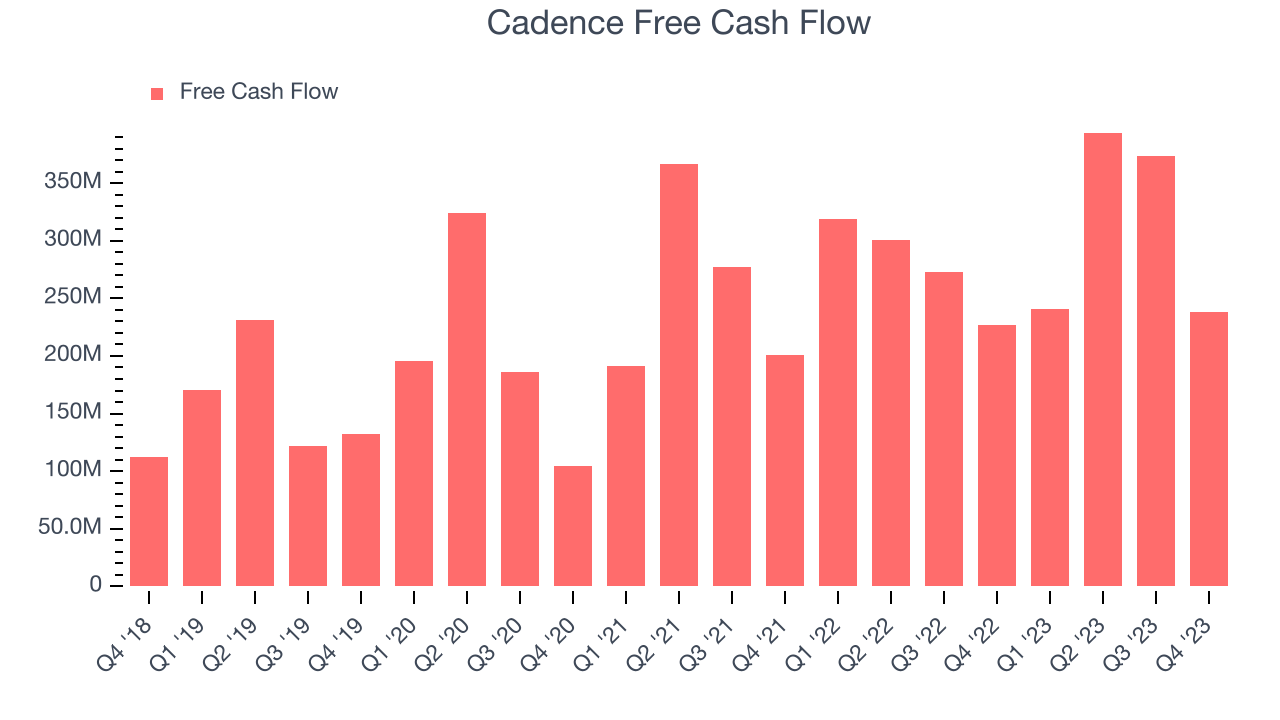

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Cadence's free cash flow came in at $238.4 million in Q4, up 5.1% year on year.

Cadence has generated $1.25 billion in free cash flow over the last 12 months, an eye-popping 30.7% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Key Takeaways from Cadence's Q4 Results

It was good to see Cadence slightly improve its gross margin and beat analysts' revenue and EPS estimates this quarter. On the other hand, its year-end backlog of $6 billion fell short of Wall Street's projections ($6.4 billion). Looking ahead, the company's full-year 2024 revenue and EPS guidance were in line with expectations, but next quarter's forecast was soft. Overall, the results could have been better. The company is down 5.2% on the results and currently trades at $291 per share.

Is Now The Time?

Cadence may have had a bad quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We think Cadence is a good business. Although its with analysts expecting growth to slow from here, its bountiful generation of free cash flow empowers it to invest in growth initiatives.

Cadence's price-to-sales ratio based on the next 12 months of 18.3x indicates that the market is certainly optimistic about its growth prospects. There's definitely a lot of things to like about Cadence and looking at the tech landscape right now, it seems that the company trades at a pretty interesting price point.

Wall Street analysts covering the company had a one-year price target of $289.36 per share right before these results (compared to the current share price of $291).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.