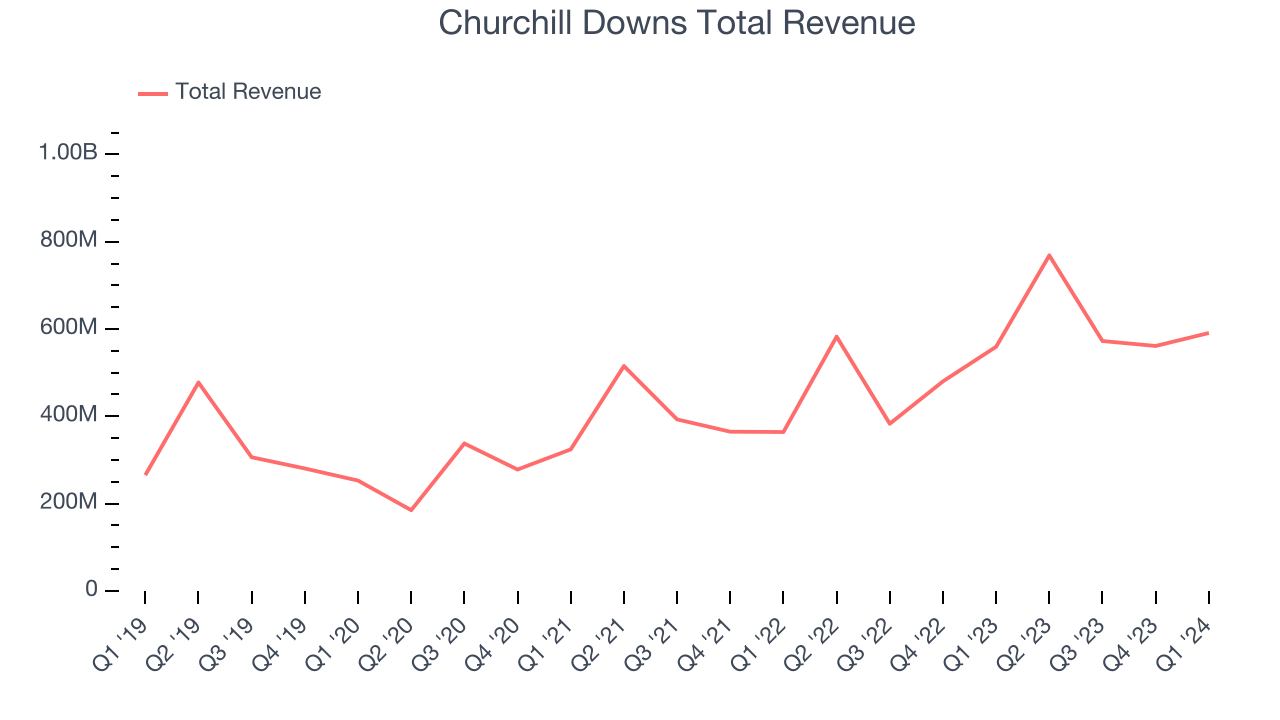

Racing, gaming, and entertainment company Churchill Downs (NASDAQ:CHDN) beat analysts' expectations in Q1 CY2024, with revenue up 5.6% year on year to $590.9 million. It made a non-GAAP profit of $1.13 per share, improving from its profit of $0.98 per share in the same quarter last year.

Is now the time to buy Churchill Downs? Find out by accessing our full research report, it's free.

Churchill Downs (CHDN) Q1 CY2024 Highlights:

- Revenue: $590.9 million vs analyst estimates of $565.9 million (4.4% beat)

- EPS (non-GAAP): $1.13 vs analyst estimates of $0.83 (36.8% beat)

- Gross Margin (GAAP): 31.3%, up from 30.7% in the same quarter last year

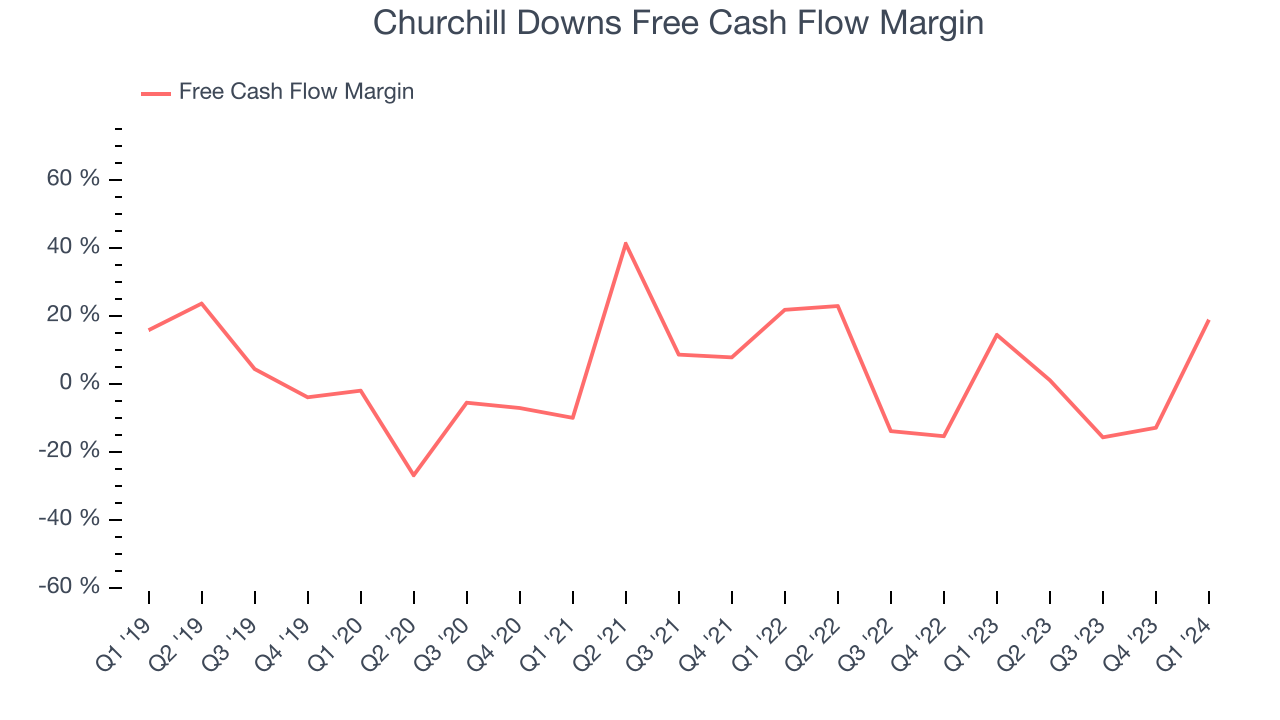

- Free Cash Flow of $112.1 million is up from -$71.9 million in the previous quarter

- Market Capitalization: $9.10 billion

Famous for hosting the Kentucky Derby, Churchill Downs (NASDAQ:CHDN) operates a horse racing, online wagering, and gaming entertainment business in the United States.

Gaming Solutions

Gaming solution companies operate in a dynamic and evolving market, and the digital transformation of the gaming industry presents significant opportunities for innovation and growth, whether it be immersive slot machine terminals or mobile sports betting. However, the gaming solution industry is not without its challenges. Regulatory compliance is a crucial consideration as companies must navigate a complex and often fragmented regulatory landscape across different jurisdictions. Changes in regulations can impact product offerings, operational practices, and market access, requiring companies to maintain flexibility and adaptability in their business strategies. Additionally, the competitive nature of the industry necessitates continuous investment in research and development to stay ahead of competitors and meet evolving consumer demands.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. Churchill Downs's annualized revenue growth rate of 18.1% over the last five years was solid for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Churchill Downs's healthy annualized revenue growth of 23.4% over the last two years is above its five-year trend, suggesting its brand resonates with consumers.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Churchill Downs's healthy annualized revenue growth of 23.4% over the last two years is above its five-year trend, suggesting its brand resonates with consumers.

We can better understand the company's revenue dynamics by analyzing its most important segments, Racing and Gaming, which are 42.1% and 41.2% of revenue. Over the last two years, Churchill Downs's Racing revenue (live and historical) averaged 67.4% year-on-year growth while its Gaming revenue (casino games) averaged 16.7% growth.

This quarter, Churchill Downs reported solid year-on-year revenue growth of 5.6%, and its $590.9 million of revenue outperformed Wall Street's estimates by 4.4%. Looking ahead, Wall Street expects sales to grow 12% over the next 12 months, an acceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Churchill Downs has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 1.1%, subpar for a consumer discretionary business.

Churchill Downs's free cash flow came in at $112.1 million in Q1, equivalent to a 19% margin and up 38.1% year on year.

Key Takeaways from Churchill Downs's Q1 Results

We were impressed by how significantly Churchill Downs blew past analysts' revenue, EBITDA, and EPS expectations this quarter. That was driven by strong performance in its racing segment, particularly at its TwinSpires subsidiary.

During the earnings release, Churchill Downs announced it would open The Rose Gaming Resort in September 2024, which cost $460 million to build. It also shared plans to open another site in the first quarter of 2025.

Lastly, the company closed the sale of its 49% stake in United Tote Company on April 8, 2024.

Overall, this was a really good quarter that should please shareholders. The stock is up 5.2% after reporting and currently trades at $130 per share.

Churchill Downs may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.