Outdoor lifestyle and equipment company Clarus (NASDAQ:CLAR) announced better-than-expected results in Q1 CY2024, with revenue down 1.4% year on year to $69.31 million. The company expects the full year's revenue to be around $275 million, in line with analysts' estimates. It made a non-GAAP loss of $0 per share, down from its profit of $0.01 per share in the same quarter last year.

Clarus (CLAR) Q1 CY2024 Highlights:

- Revenue: $69.31 million vs analyst estimates of $64.53 million (7.4% beat)

- Adjusted EBITDA: $2.0 million vs analyst estimates of $2.4 million (miss)

- EPS (non-GAAP): $0 vs analyst estimates of $0.02 (-$0.02 miss)

- The company reconfirmed its revenue guidance for the full year of $275 million at the midpoint (also reaffirmed its adjusted EBITDA guidance for the full year)

- Gross Margin (GAAP): 35.9%, up from 12.7% in the same quarter last year

- Market Capitalization: $243.2 million

Initially a financial services business, Clarus (NASDAQ:CLAR) designs, manufactures, and distributes outdoor equipment and lifestyle products.

The company was founded in 1991, but after recognizing the potential of the outdoor equipment market, pivoted to meet the needs of adventure enthusiasts in 2002.

Today, Clarus offers products across several brands, including Black Diamond Equipment, Sierra Bullets, PIEPS, and SKINourishment. Its brands sell goods such as advanced climbing gear, ski equipment, precision ammunition, and skincare products tailored for outdoor environments.

Clarus generates revenue through a multi-faceted approach, leveraging a direct salesforce, extensive retail partnerships, and an e-commerce platform to sell its products. This strategy allows the company to reach a diverse and global consumer base.

Leisure Products

Leisure products cover a wide range of goods in the consumer discretionary sector. Maintaining a strong brand is key to success, and those who differentiate themselves will enjoy customer loyalty and pricing power while those who don’t may find themselves in precarious positions due to the non-essential nature of their offerings.

Select competitors in the outdoor and recreation space include The North Face (owned by NYSE:VFC), Johnson Outdoors (NASDAQ:JOUT), and Smith & Wesson (NASDAQ:SWBI).Sales Growth

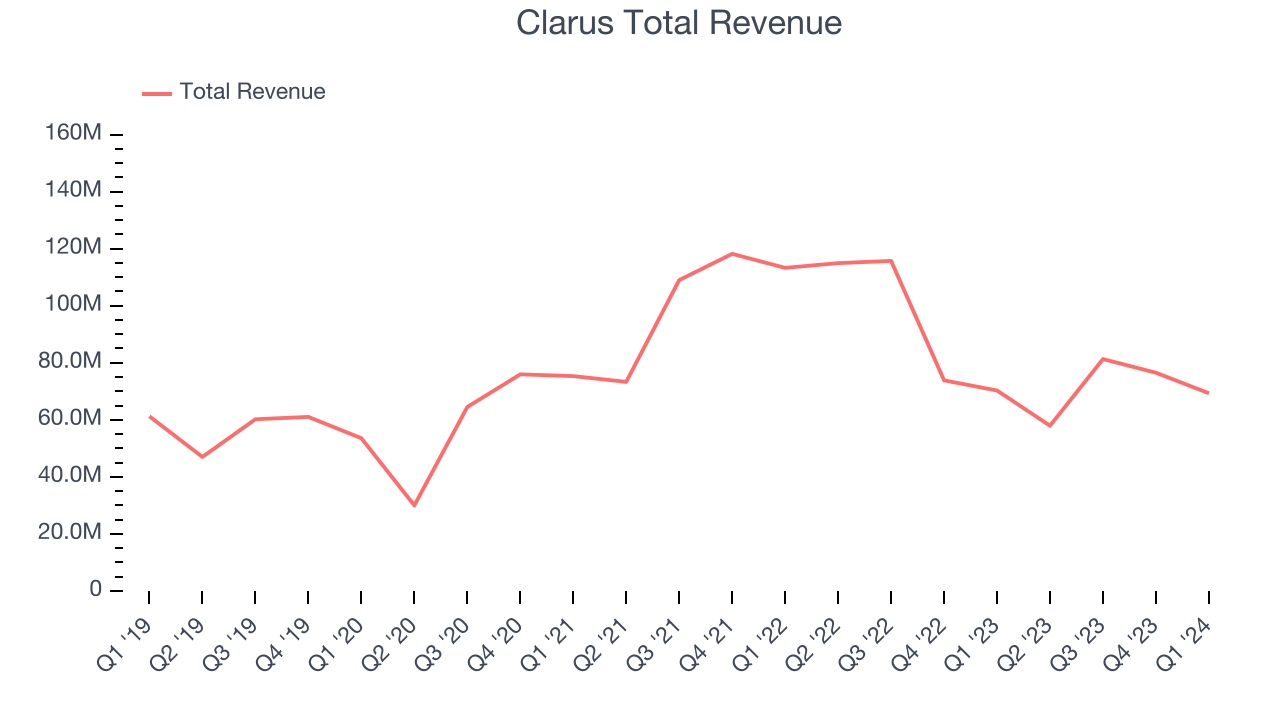

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. Clarus's annualized revenue growth rate of 5.3% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Clarus's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 17% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Clarus's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 17% over the last two years.

This quarter, Clarus's revenue fell 1.4% year on year to $69.31 million but beat Wall Street's estimates by 7.4%. Looking ahead, Wall Street expects sales to grow 1.4% over the next 12 months, an acceleration from this quarter.

Operating Margin

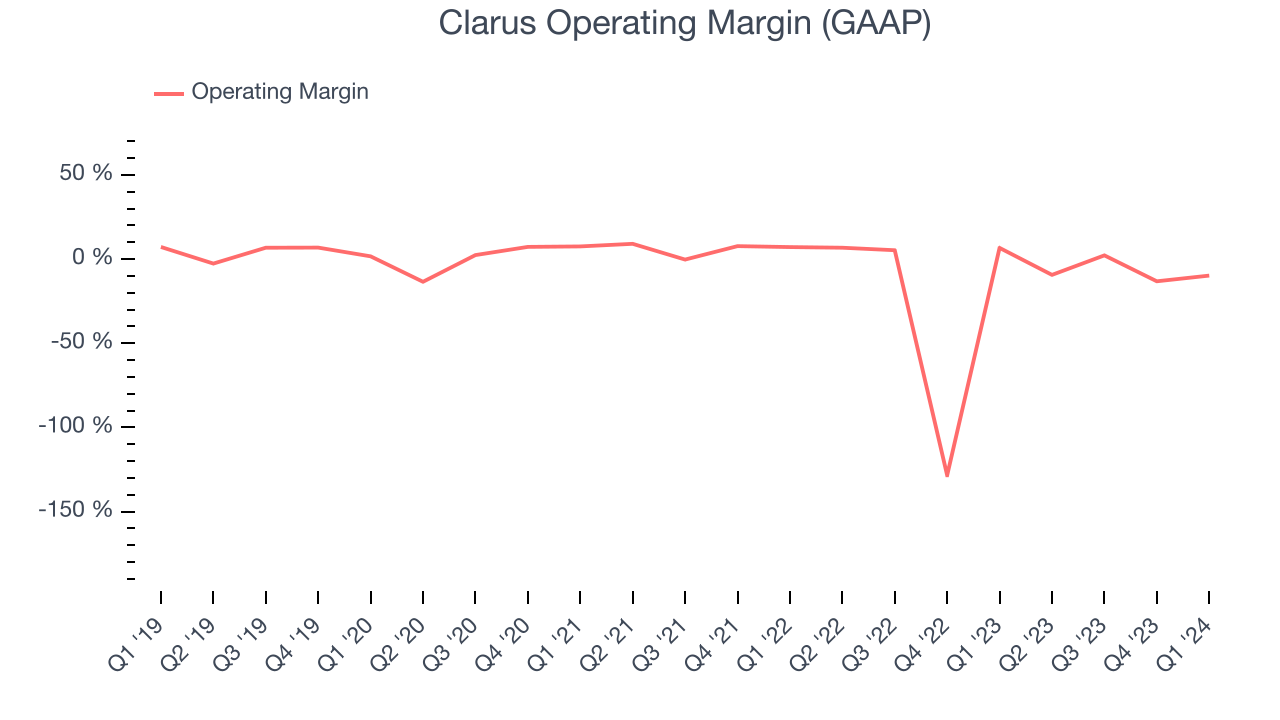

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Given the consumer discretionary industry's volatile demand characteristics, unprofitable companies should be scrutinized. Over the last two years, Clarus's high expenses have contributed to an average operating margin of negative 14.6%.

This quarter, Clarus generated an operating profit margin of negative 9.8%, down 16.5 percentage points year on year.

Over the next 12 months, Wall Street expects Clarus to become profitable. Analysts are expecting the company’s LTM operating margin of negative 7.2% to rise to positive 2.6%.EPS

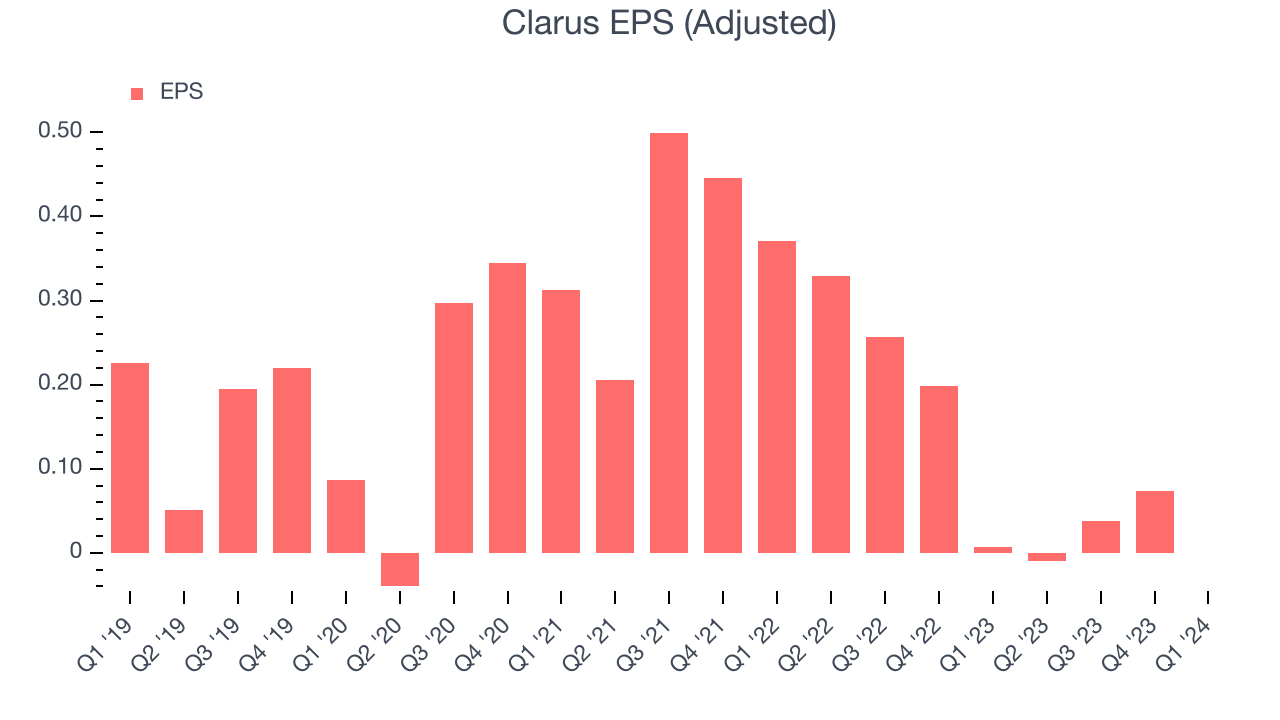

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last five years, Clarus's EPS dropped 312%, translating into 32.7% annualized declines. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends or consumer preferences. Consumer discretionary companies are particularly exposed to this, leaving a low margin of safety around the company (making the stock susceptible to large downward swings).

In Q1, Clarus reported EPS at $0, down from $0.01 in the same quarter last year. This print unfortunately missed analysts' estimates. We also like to analyze expected EPS growth based on Wall Street analysts' consensus projections, but unfortunately, there is insufficient data.

Return on Invested Capital (ROIC)

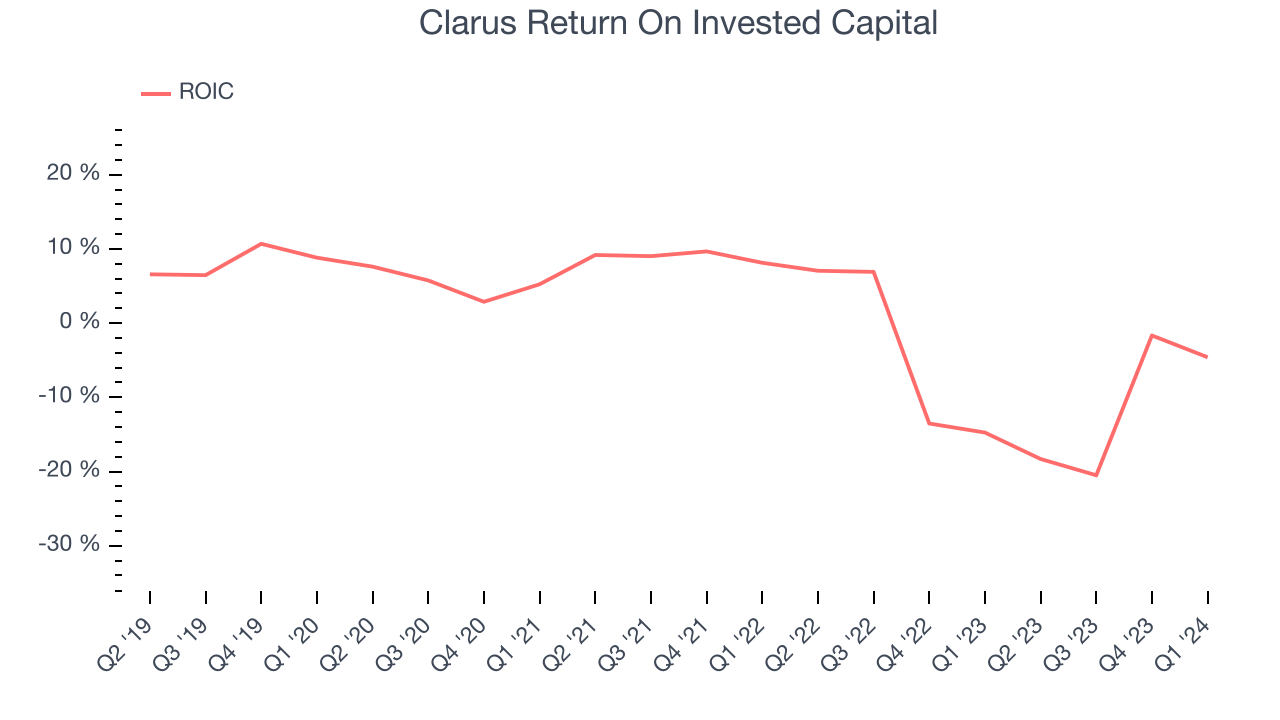

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to how much money the business raised (debt and equity).

Clarus's five-year average return on invested capital was 0.6%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Clarus's ROIC significantly decreased over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Clarus is a well-capitalized company with $47.48 million of cash and $81,000 of debt, meaning it could pay back all its debt tomorrow and still have $47.4 million of cash on its balance sheet. This net cash position gives Clarus the freedom to raise more debt, return capital to shareholders, or invest in growth initiatives.

Key Takeaways from Clarus's Q1 Results

We were impressed by how significantly Clarus blew past analysts' revenue expectations this quarter. On the other hand, its operating margin missed and its EPS fell short of Wall Street's estimates. Overall, this was a mixed quarter for Clarus. The stock is flat after reporting and currently trades at $6.1 per share.

Is Now The Time?

Clarus may have had a mixed quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Clarus, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last five years, and analysts expect growth to deteriorate from here. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its declining EPS over the last five years makes it hard to trust. On top of that, its relatively low ROIC suggests it has historically struggled to find compelling business opportunities.

While we've no doubt one can find things to like about Clarus, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $7.25 per share right before these results (compared to the current share price of $6.10).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.