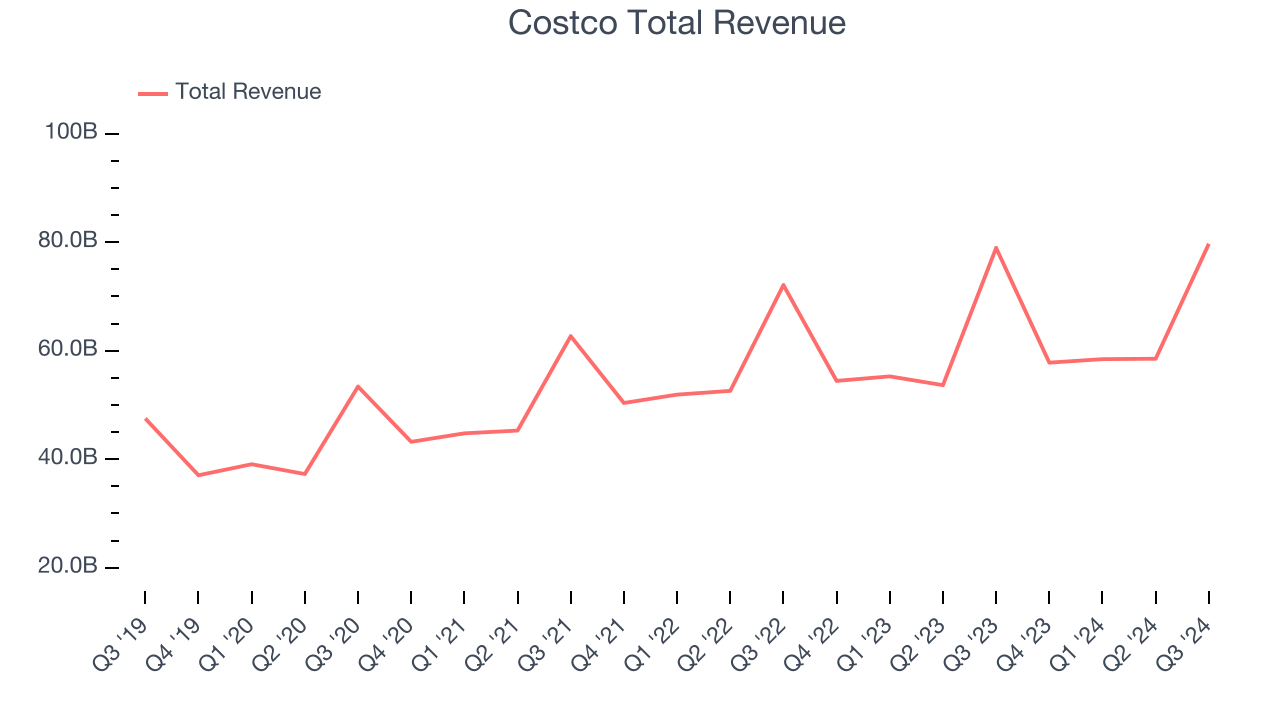

Membership-only discount retailer Costco (NASDAQ:COST) met Wall Street’s revenue expectations in Q3 CY2024, but sales were flat year on year at $79.7 billion. Its GAAP profit of $5.29 per share was 4.5% above analysts’ consensus estimates.

Is now the time to buy Costco? Find out by accessing our full research report, it’s free.

Costco (COST) Q3 CY2024 Highlights:

- Revenue: $79.7 billion vs analyst estimates of $80.03 billion (in line)

- EPS: $5.29 vs analyst estimates of $5.06 (4.5% beat)

- Gross Margin (GAAP): 12.7%, in line with the same quarter last year

- EBITDA Margin: 5.7%, up from 4.4% in the same quarter last year

- Free Cash Flow Margin: 1.7%, down from 2.7% in the same quarter last year

- Locations: 891 at quarter end, up from 861 in the same quarter last year

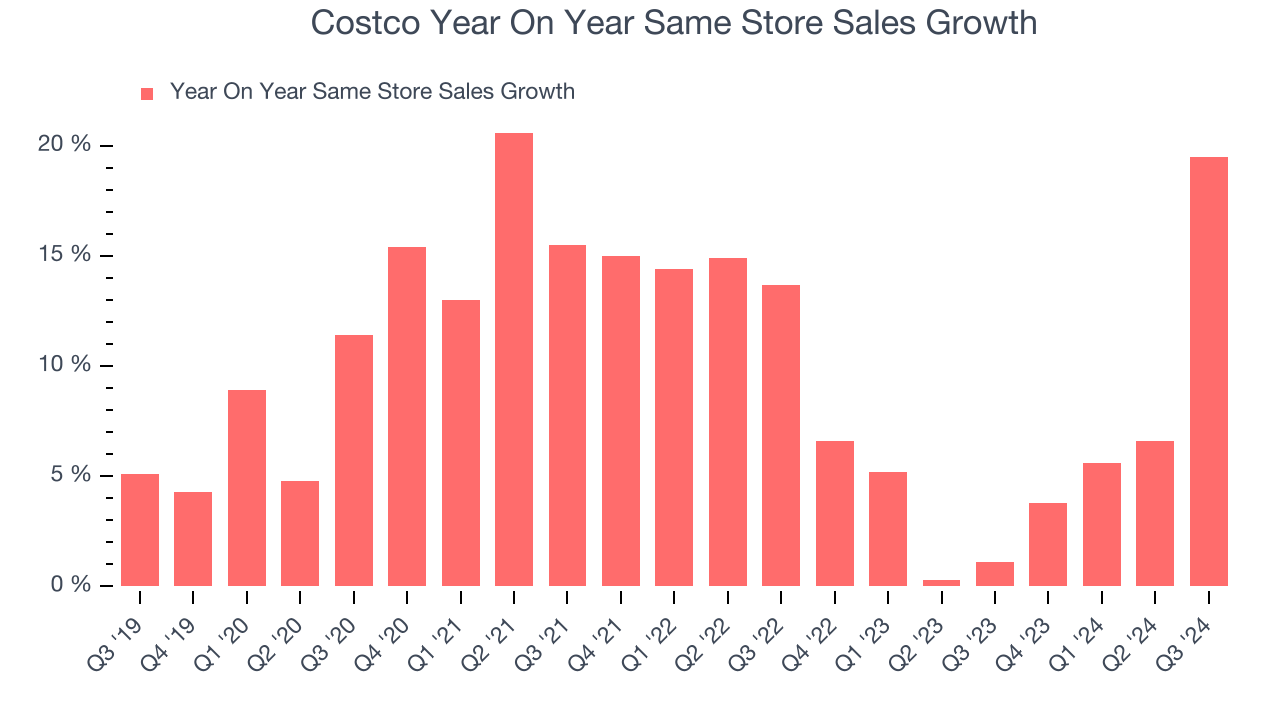

- Same-Store Sales rose 19.5% year on year (1.1% in the same quarter last year)

- Market Capitalization: $402.7 billion

Company Overview

Designed to be a one-stop shop for the suburban consumer, Costco (NASDAQ:COST) is a membership-only retail chain that sells groceries, apparel, toys, and household items, often in bulk quantities.

Large-format Grocery & General Merchandise Retailer

Big-box retailers operate large stores that sell groceries and general merchandise at highly competitive prices. Because of their scale and resulting purchasing power, these big-box retailers–with annual sales in the tens to hundreds of billions of dollars–are able to get attractive volume discounts and sell at often the lowest prices. While e-commerce is a threat, these retailers have been able to weather the storm by either providing a unique in-store shopping experience or by reinvesting their hefty profits into omnichannel investments.

Sales Growth

Costco is a behemoth in the consumer retail sector and benefits from economies of scale, an important advantage giving the business an edge in distribution and more negotiating power with suppliers.

As you can see below, the company’s annualized revenue growth rate of 10.8% over the last five years was decent as it opened new stores and grew sales at existing, established stores.

This quarter, Costco’s revenue grew 1% year on year to $79.7 billion, falling short of Wall Street’s estimates. Looking ahead, Wall Street expects sales to grow 7.6% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for retailers.

Costco’s demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company’s same-store sales have grown by 6.1% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Costco is reaching more customers and growing sales.

In the latest quarter, Costco’s same-store sales rose 19.5% year on year. This growth was an acceleration from the 1.1% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Costco’s Q3 Results

We were impressed by how significantly Costco blew past analysts’ gross margin expectations this quarter. We were also happy its EPS narrowly outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $894.53 immediately following the results.

Should you buy the stock or not?The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy.We cover that in our actionable full research report which you can read here, it’s free.