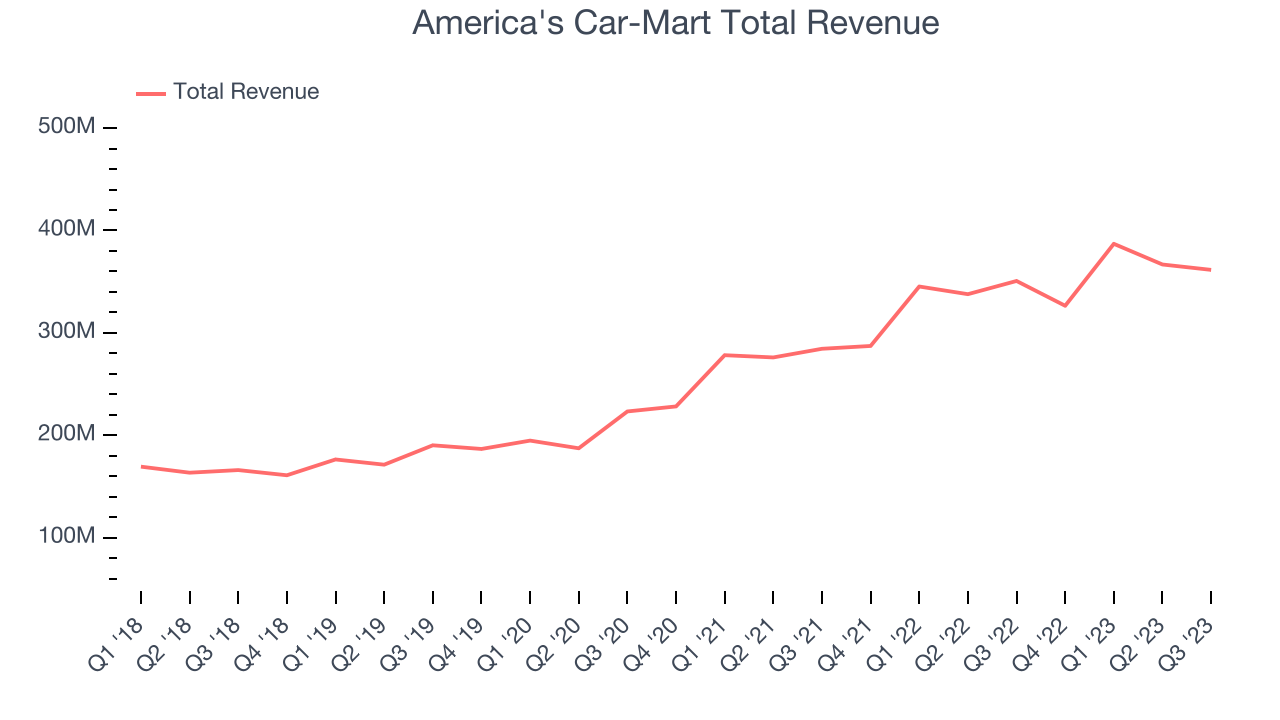

Used-car retailer America’s Car-Mart (NASDAQ:CRMT) fell short of analysts' expectations in Q2 FY2024, with revenue up 3.1% year on year to $361.6 million. It made a GAAP loss of $4.30 per share, down from its profit of $0.48 per share in the same quarter last year.

Is now the time to buy America's Car-Mart? Find out by accessing our full research report, it's free.

America's Car-Mart (CRMT) Q2 FY2024 Highlights:

- Revenue: $361.6 million vs analyst estimates of $376 million (3.8% miss)

- EPS: -$4.30 vs analyst estimates of $0.79 (-$5.09 miss)

- Free Cash Flow was -$30.94 million compared to -$41.81 million in the same quarter last year

- Gross Margin (GAAP): 7.6%, down from 15.9% in the same quarter last year

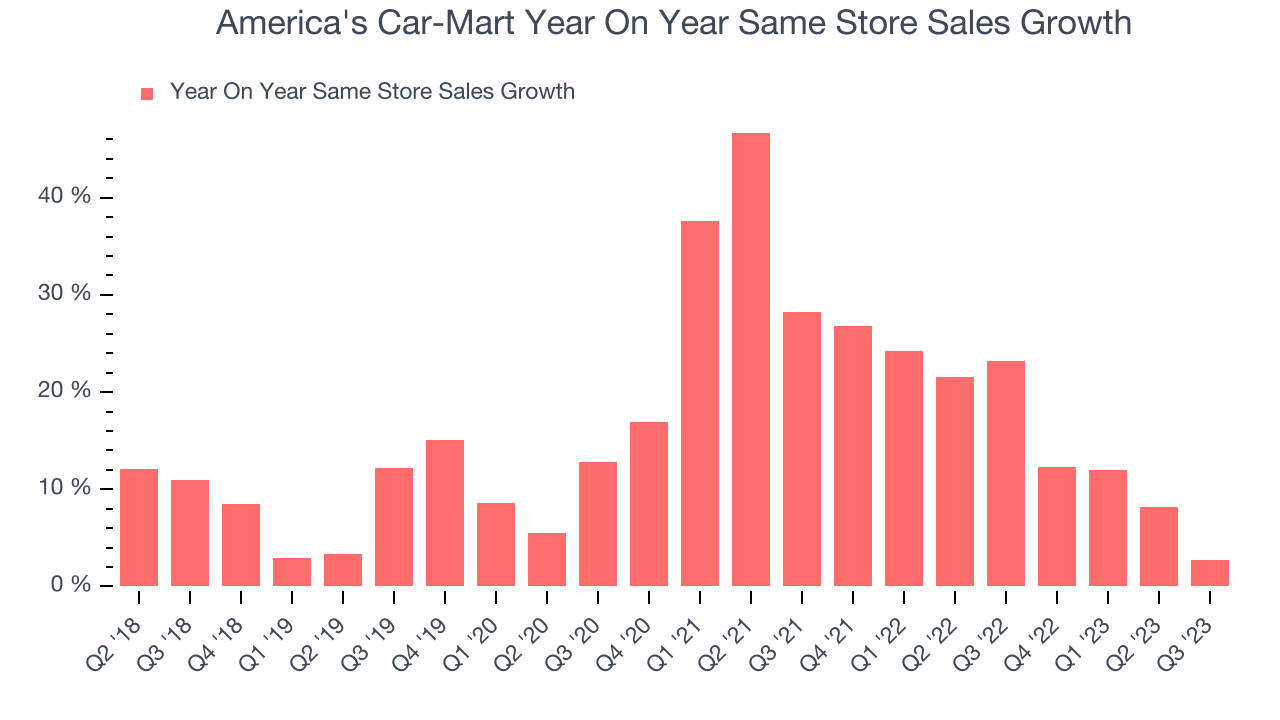

- Same-Store Sales were up 2.7% year on year (big miss vs. expectations of up 7.5% year on year

- Net charge offs: 7.2% vs analyst estimates of 6.4%

With a strong presence in the Southern and Central US, America’s Car-Mart (NASDAQ:CRMT) sells used cars to budget-conscious consumers.

Vehicle Retailer

Buying a vehicle is a big decision and usually the second-largest purchase behind a home for many people, so retailers that sell new and used cars try to offer selection, convenience, and customer service to shoppers. While there is online competition, especially for research and discovery, the vehicle sales market is still very fragmented and localized given the magnitude of the purchase and the logistical costs associated with moving cars over long distances. At the end of the day, a large swath of the population relies on cars to get from point A to point B, and vehicle sellers are acutely aware of this need.

Sales Growth

America's Car-Mart is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale. On the other hand, one advantage is that its growth rates can be higher because it's growing off a small base.

As you can see below, the company's annualized revenue growth rate of 19.8% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was excellent despite not opening many new stores, implying that growth was driven by increased sales at existing, established stores.

This quarter, America's Car-Mart grew its revenue by 3.1% year on year, falling short of Wall Street's estimates. Looking ahead, analysts expect sales to grow 6.3% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

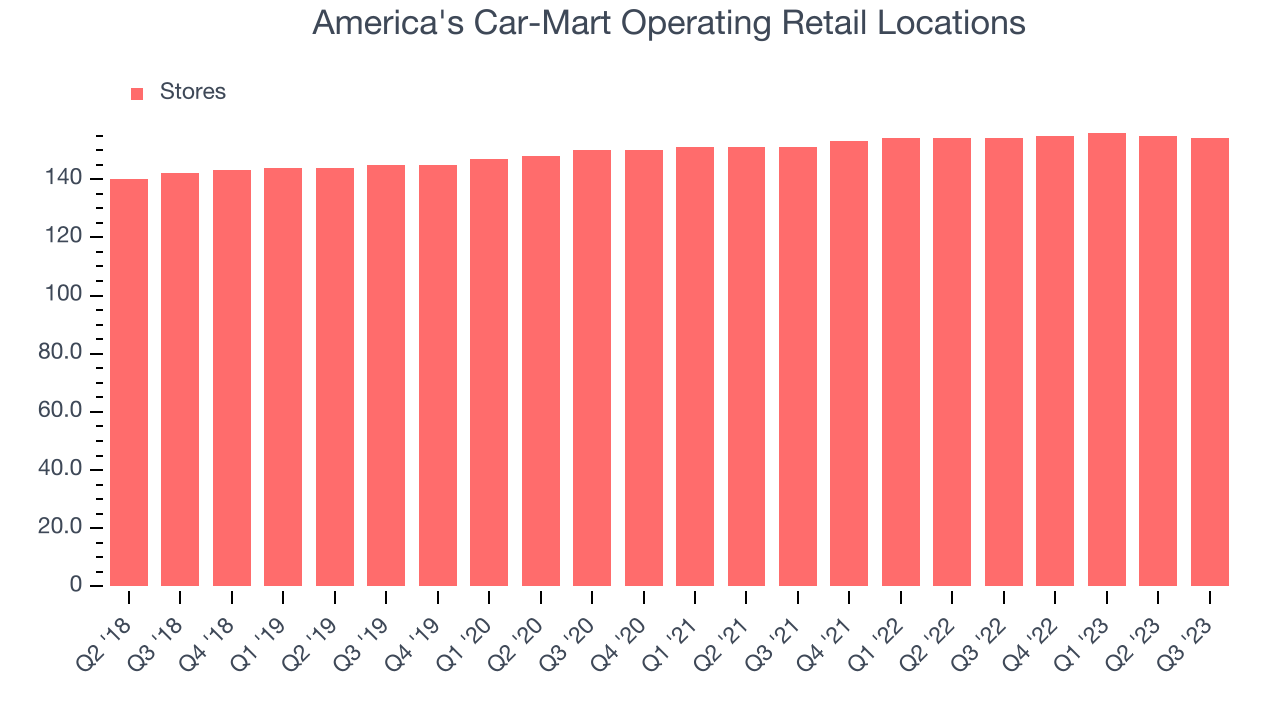

Number of Stores

A retailer's store count is a crucial factor influencing how much it can sell, and store growth is a critical driver of how quickly its sales can grow.

When a retailer like America's Car-Mart keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. As of the most recently reported quarter, America's Car-Mart operated 154 total retail locations, in line with its store count a year ago.

Over the last two years, the company has only opened a few new stores, averaging 1.4% annual growth in new locations. This sluggish pace lags the broader sector. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

America's Car-Mart's demand has outpaced the broader consumer retail sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 16.4% year on year. Given its flat store count over the same period, this performance stems from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, America's Car-Mart's same-store sales rose 2.7% year on year. By the company's standards, this growth was a meaningful deceleration from the 23.2% year-on-year increase it posted 12 months ago. We'll be watching America's Car-Mart closely to see if it can reaccelerate growth.

Key Takeaways from America's Car-Mart's Q2 Results

With a market capitalization of $515.9 million, America's Car-Mart is among smaller companies, but its more than $4.31 million in cash on hand and near break-even free cash flow margins puts it in a stable financial position.

We struggled to find many strong positives in these results. Same-store sales missed, leading to a revenue shortfall vs. expectations. Most worrying was a huge step-up in provision for credit losses, which impacted margins and EPS. Management called out a "challenging economy" and added that the "persistent inflationary environment impacted existing customers, which was evident in our credit losses. This required an increase in the allowance for credit losses which subsequently impacted the bottom line for the quarter." Overall, the results could have been better. The company is down 31.9% on the results and currently trades at $55 per share.

America's Car-Mart may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.