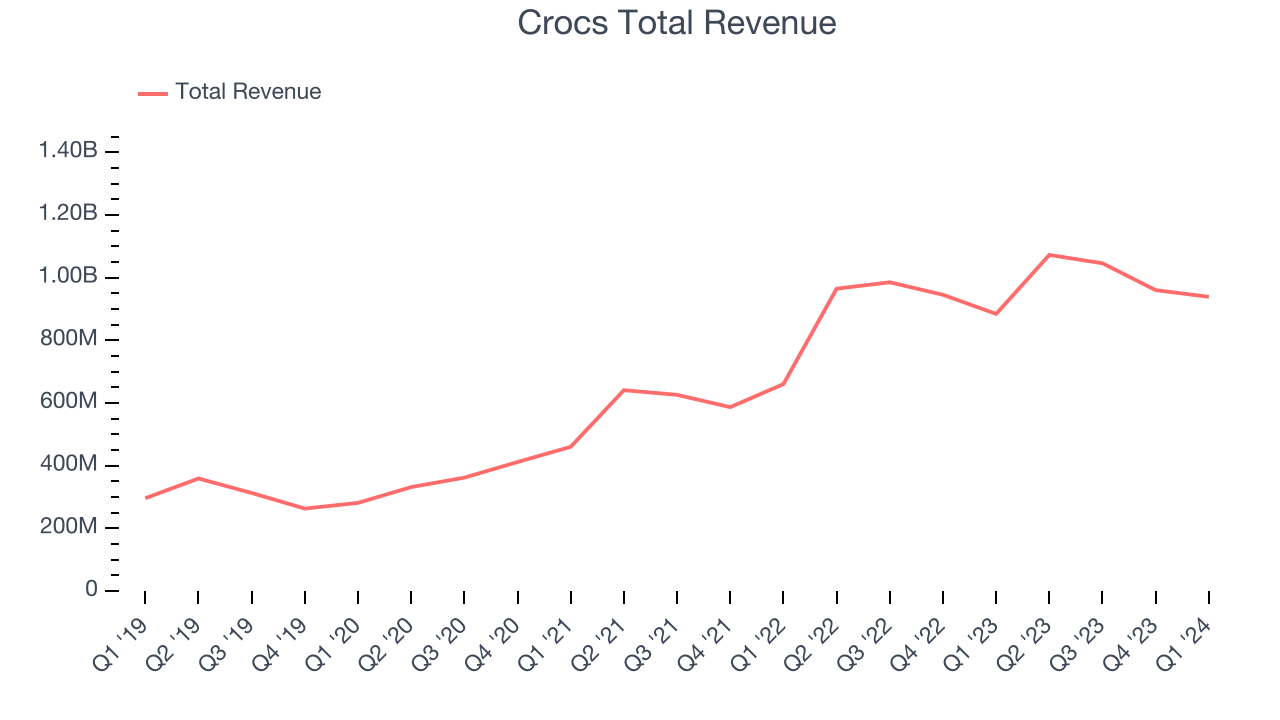

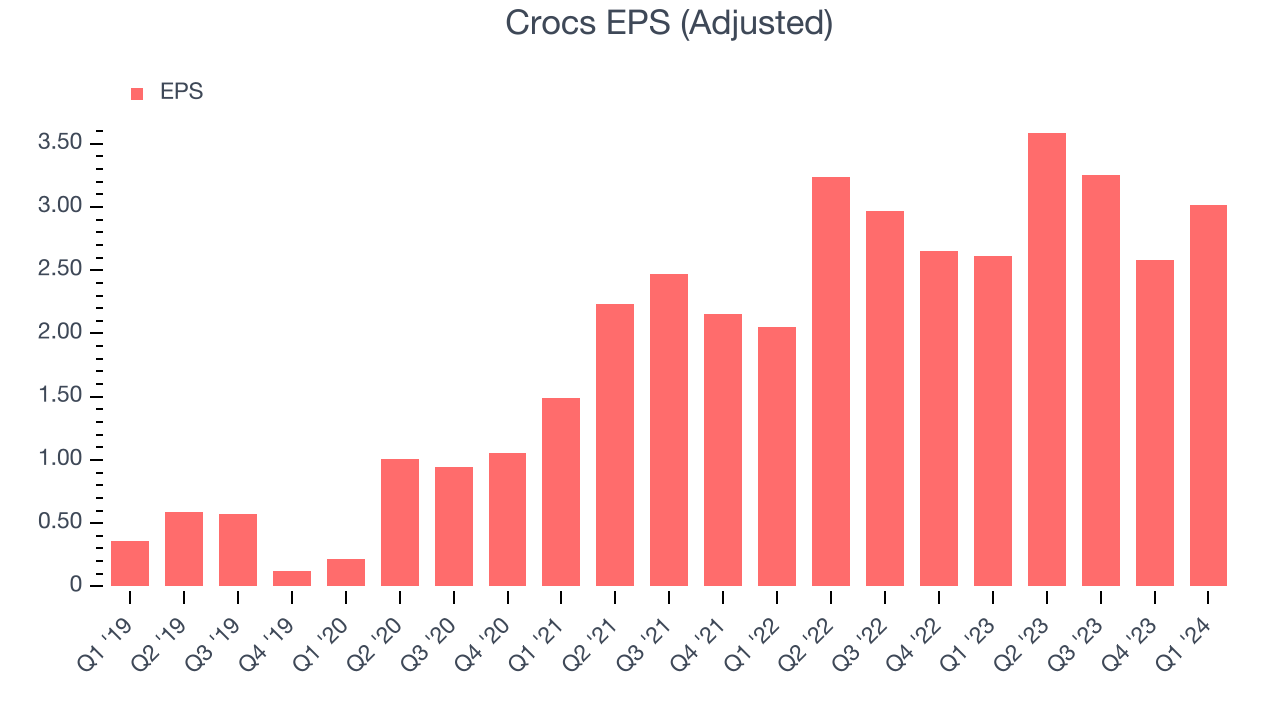

Footwear company Crocs (NASDAQ:CROX) beat analysts' expectations in Q1 CY2024, with revenue up 6.2% year on year to $938.6 million. It made a non-GAAP profit of $3.02 per share, improving from its profit of $2.61 per share in the same quarter last year.

Crocs (CROX) Q1 CY2024 Highlights:

- Total Revenue: $938.6 million vs analyst estimates of $884.7 million (6.1% beat)

- Crocs Revenue: $743.8 million vs analyst estimates of $697.1 million (6.7% beat)

- HEYDUDE Revenue: $194.8 million vs analyst estimates of $184.8 million (5.4% beat)

- EPS (non-GAAP): $3.02 vs analyst estimates of $2.25 (34% beat)

- EPS (non-GAAP) Guidance for Q2 CY2024 is $3.47 at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 55.6%, up from 53.9% in the same quarter last year

- Free Cash Flow was -$43.32 million, down from $320.5 million in the previous quarter

- Market Capitalization: $7.69 billion

Founded in 2002, Crocs (NASDAQ:CROX) sells casual footwear and is known for its iconic clog shoe.

The original Crocs shoe, made from the company's proprietary closed-cell resin called Croslite, was initially intended for boating and outdoor wear due to its slip-resistant, non-marking sole. However, the comfort and functionality of the shoes quickly made them a cross-cultural phenomenon, expanding their use to casual wear, professional use, and even as a fashion statement.

Crocs has capitalized on the popularity of its signature clog by offering a broad assortment of footwear styles, including sandals, wedges, slides, and boots. The brand is also known for its wide range of colors and the ability to personalize shoes with "Jibbitz" charms, small decorative pieces that fit into the holes of the Crocs clogs.

The company sells its products in more than 90 countries through wholesalers, retail stores, and directly to consumers through its website and company-owned stores. Despite its simple product line, Crocs has maintained its relevance through strategic collaborations with designers, celebrities, and brands, elevating the relevance of its products.

Footwear

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Crocs primary competitors include Skechers (NYSE:SKX), Deckers (NYSE:DECK), Birkenstock (private), and private companies Sanuk and Teva.Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. Crocs's annualized revenue growth rate of 29.5% over the last five years was exceptional for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Crocs's recent history shows its momentum has slowed as its annualized revenue growth of 26.4% over the last two years is below its five-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Crocs's recent history shows its momentum has slowed as its annualized revenue growth of 26.4% over the last two years is below its five-year trend.

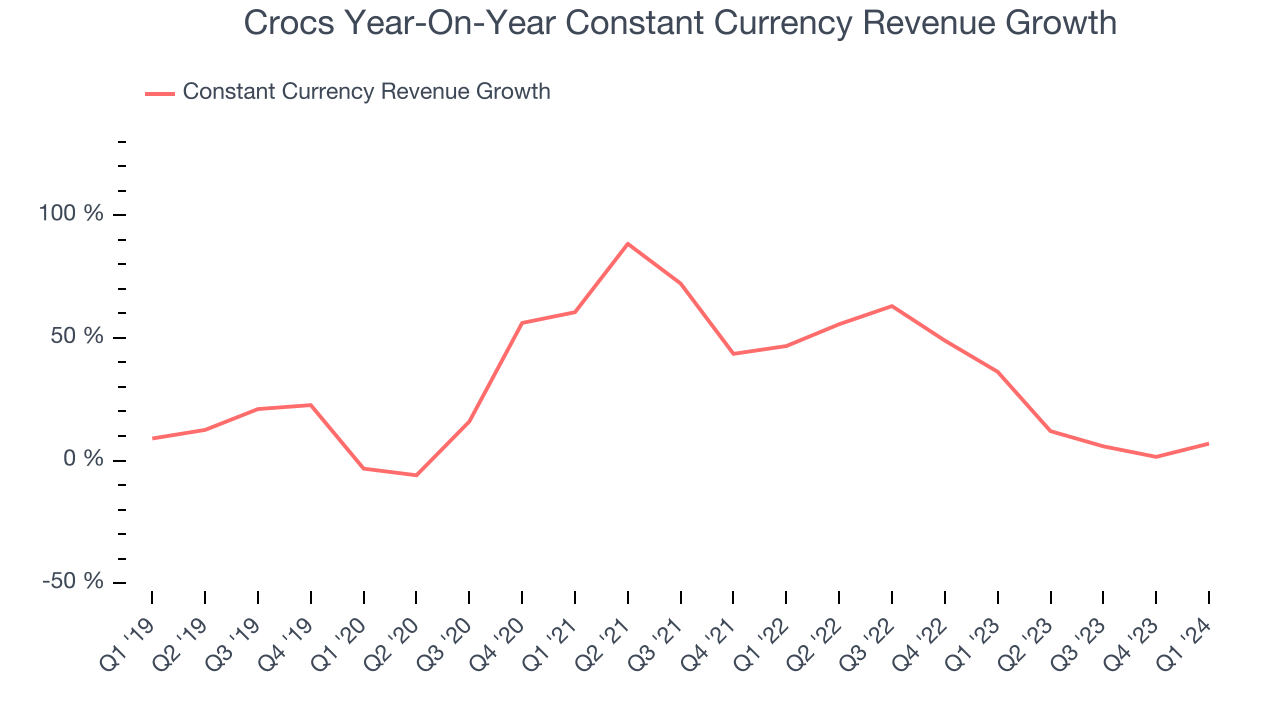

Crocs also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 28.7% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see that foreign exchange rates have been a headwind for Crocs.

This quarter, Crocs reported solid year-on-year revenue growth of 6.2%, and its $938.6 million of revenue outperformed Wall Street's estimates by 6.1%. Looking ahead, Wall Street expects sales to grow 4.5% over the next 12 months, a deceleration from this quarter.

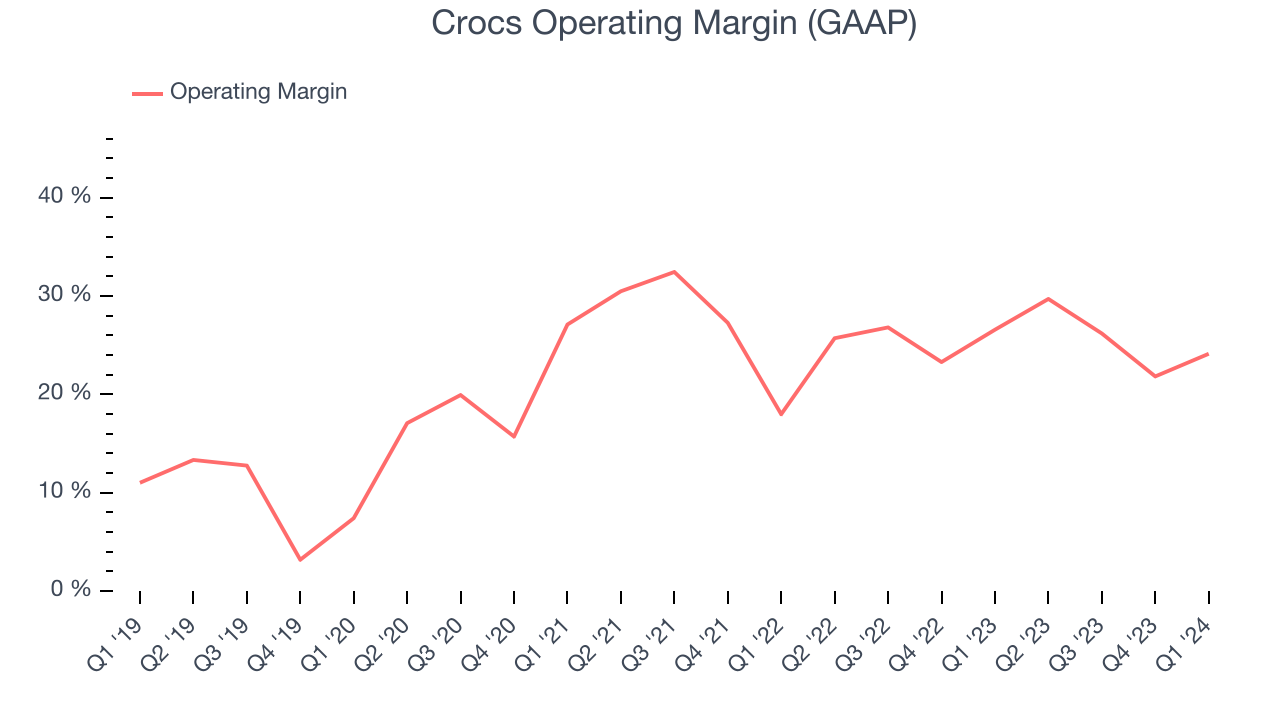

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Crocs has been a well-oiled machine over the last two years. It's demonstrated elite profitability for a consumer discretionary business, boasting an average operating margin of 25.6%.

This quarter, Crocs generated an operating profit margin of 24.1%, down 2.4 percentage points year on year.

Over the next 12 months, Wall Street expects Crocs to maintain its LTM operating margin of 25.6%.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, Crocs's EPS grew 1,160%, translating into an astounding 66% compounded annual growth rate. This performance is materially higher than its 29.5% annualized revenue growth over the same period. There are a few reasons for this, and understanding why can shed light on its fundamentals.

While we mentioned earlier that Crocs's operating margin declined this quarter, a five-year view shows its margin has expanded 13.1 percentage points while its share count has shrunk 18.5%. Improving profitability and share buybacks are positive signs as they juice EPS growth relative to revenue growth.In Q1, Crocs reported EPS at $3.02, up from $2.61 in the same quarter last year. This print beat analysts' estimates by 34%. Over the next 12 months, Wall Street expects Crocs to grow its earnings. Analysts are projecting its LTM EPS of $12.44 to climb by 2.2% to $12.71.

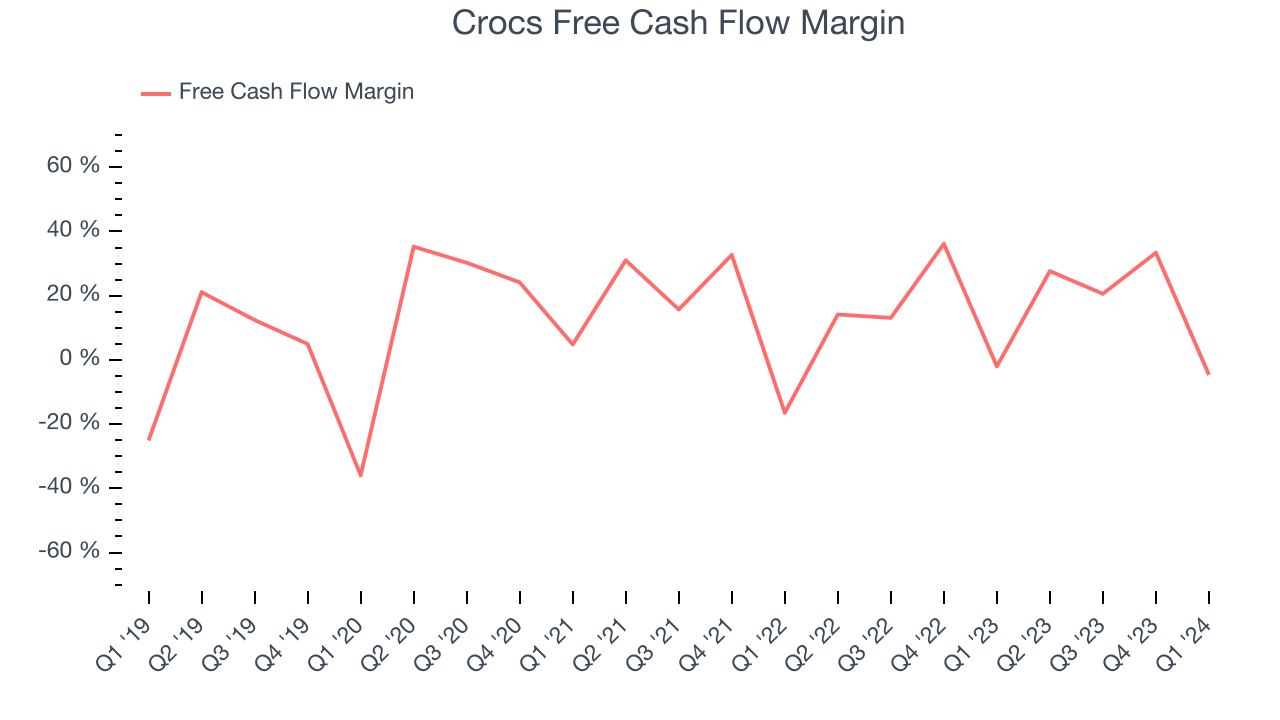

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Crocs has shown strong cash profitability, giving it an edge over its competitors and the option to reinvest or return capital to investors while keeping cash on hand for emergencies. The company's free cash flow margin has averaged 17.7%, quite impressive for a consumer discretionary business.

Crocs burned through $43.32 million of cash in Q1, equivalent to a negative 4.6% margin, reducing its cash burn by 145% year on year. Over the next year, analysts predict Crocs's cash profitability will improve. Their consensus estimates imply its LTM free cash flow margin of 19.6% will increase to 23%.

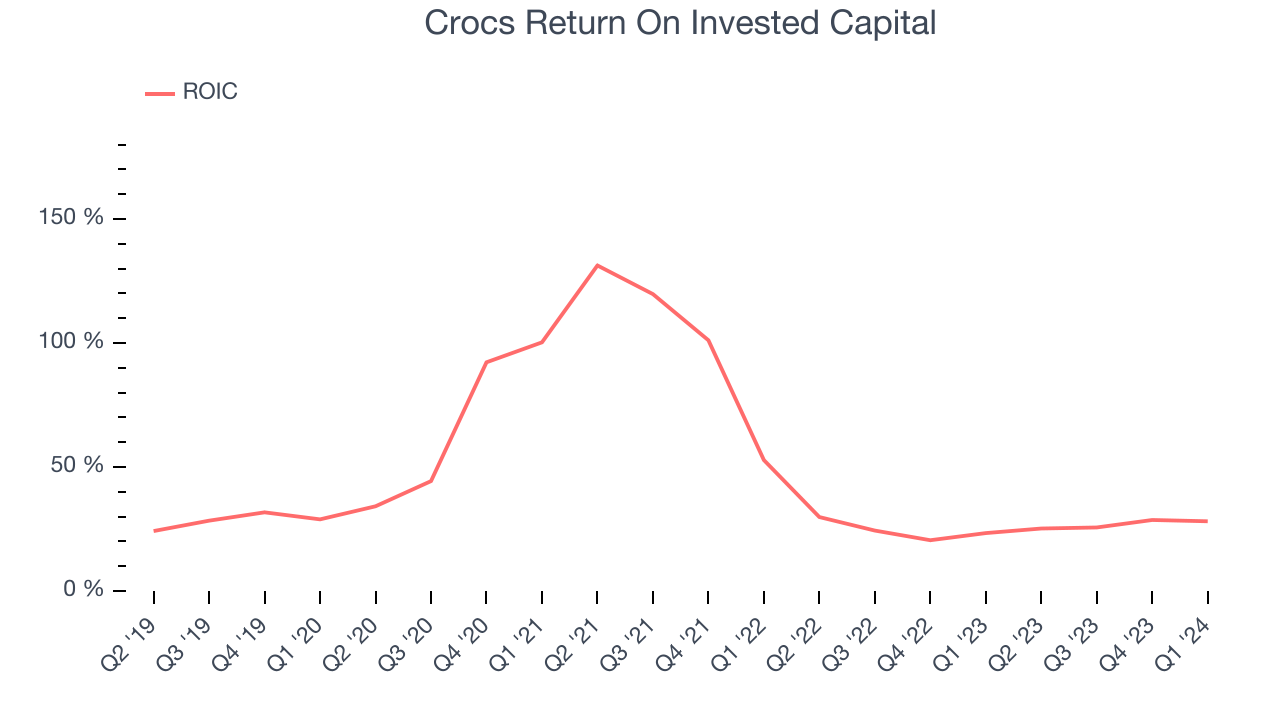

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Crocs's five-year average ROIC was 33.3%, placing it among the best consumer discretionary companies. Just as you’d like your investment dollars to generate returns, Crocs's invested capital has produced excellent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Crocs's ROIC significantly decreased over the last few years. The company has historically shown the ability to generate good returns, but they have gone the wrong way recently, making us a bit conscious.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Crocs reported $159.3 million of cash and $2.06 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $1.14 billion of EBITDA over the last 12 months, we view Crocs's 1.7x net-debt-to-EBITDA ratio as safe. We also see its $86.33 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Crocs's Q1 Results

We were impressed by how significantly Crocs blew past analysts' constant currency revenue and EPS expectations this quarter, driven by outperformance in its flagship Crocs and HEYDUDE brands. On the other hand, its full-year revenue guidance fell slightly short of Wall Street's estimates while its earnings outlook was in line. Overall, we think this was still a really good quarter that should please shareholders. Investors are likely disappointed by the guidance, however, and the stock is down 2.3% after reporting, trading at $123.85 per share.

Is Now The Time?

Crocs may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We think Crocs is a good business. First off, its revenue growth has been exceptional over the last five years. And while its projected EPS for the next year is lacking, its impressive operating margins show it has a highly efficient business model. On top of that, its stellar ROIC suggests it has been a well-run company historically.

Crocs's price-to-earnings ratio based on the next 12 months is 10.0x. There are definitely a lot of things to like about Crocs, and looking at the consumer discretionary landscape right now, it seems to be trading at a pretty interesting price.

Wall Street analysts covering the company had a one-year price target of $146.42 per share right before these results (compared to the current share price of $123.85), implying they saw upside in buying Crocs in the short term.

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.