CrowdStrike (CRWD) Reports Strong Q4 Results, Guides for 50% Growth Next Year

Radek Strnad /

March 16, 2021

Cybersecurity company Crowdstrike (NASDAQ:CRWD) reported Q4 FY2021 results topping analyst expectations, with revenue up 74.17% year on year to $264.9 million. Crowdstrike made a GAAP loss of $19.00 million, improving on its loss of $28.41 million, in the same quarter last year.

Crowdstrike (CRWD) Q4 FY2021 Highlights:

- Revenue: $264.9 million vs analyst estimates of $250.6 million (5.7% beat)

- EPS (non-GAAP): $0.13 vs analyst estimates of $0.08 ($0.05 beat)

- Revenue guidance for Q1 2022 is $290.0 million at the midpoint, above analyst estimates of $268.4 million

- Management's revenue guidance for FY2022 of $1.316 billion at the midpoint, predicting 50.45% growth (vs 84.49% in FY2021)

- Free cash flow of $97.39 million, up from $76.10 milion in previous quarter

- 9,896 customers, up from 8,416 in previous quarter

- Gross Margin (GAAP): 74.81%, up from 73.53% previous quarter

“Our go-to-market engine has gained incredible momentum with both marquee enterprises and small businesses alike as we expand our partner ecosystem and leverage our frictionless sales motion and leading technology to deliver immediate value to our customers. Combined with strong secular tailwinds, including digital transformation and an unprecedented threat environment, and our expanding technology portfolio, which now includes leading index-free data ingestion capabilities, we believe we are in an ideal position to further extend our leadership in the Security Cloud category we pioneered,” said George Kurtz, CrowdStrike’s co-founder and chief executive officer.

Modern Cybersecurity

The story of Crowdstrike starts in 2011 when the founder George Kurtz watched a fellow plane passenger turn his laptop on and wait 15 minutes for the antivirus software to stop scanning before he could use the computer.

Crowdstrike (CRWD) is a cybersecurity software as a service that protects companies from breaches and detects and responds to attacks. Unlike the legacy antivirus products which are typically rules based and on-premise, Crowdstrike's Falcon platform is cloud-based and uses prevention-and-detection technology based on machine-learning and artificial intelligence that looks for behavioral attack patterns and indicators of attack to identify bad actors. As a result it is easier and cheaper to deploy, it works on any device and it has superior efficacy rates in detecting threats compared to the legacy competitors.

The overall demand for cybersecurity has been increasing as companies move their systems and data into cloud and work is becoming more distributed.

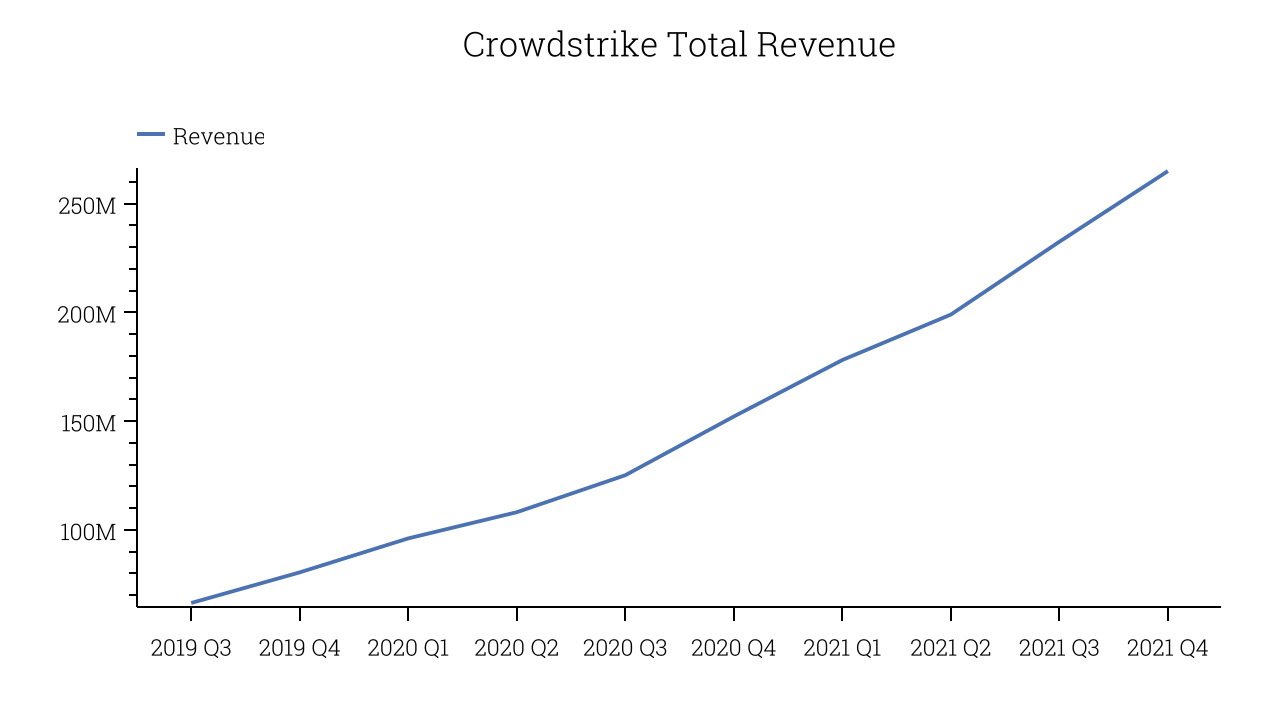

As you can see below, Crowdstrike's revenue growth has been incredible over the last twelve months, growing from $152.1 million to $264.9 million.

This was another standout quarter with the revenue up a splendid 74.17% year on year. Quarter on quarter the revenue increased by $32.47 million in Q4, which was roughly in line with the Q3 2021 increase. This steady quarter-on-quarter growth shows the company is able to maintain a strong growth trajectory.

Crowdstrike Grows With Its Customers

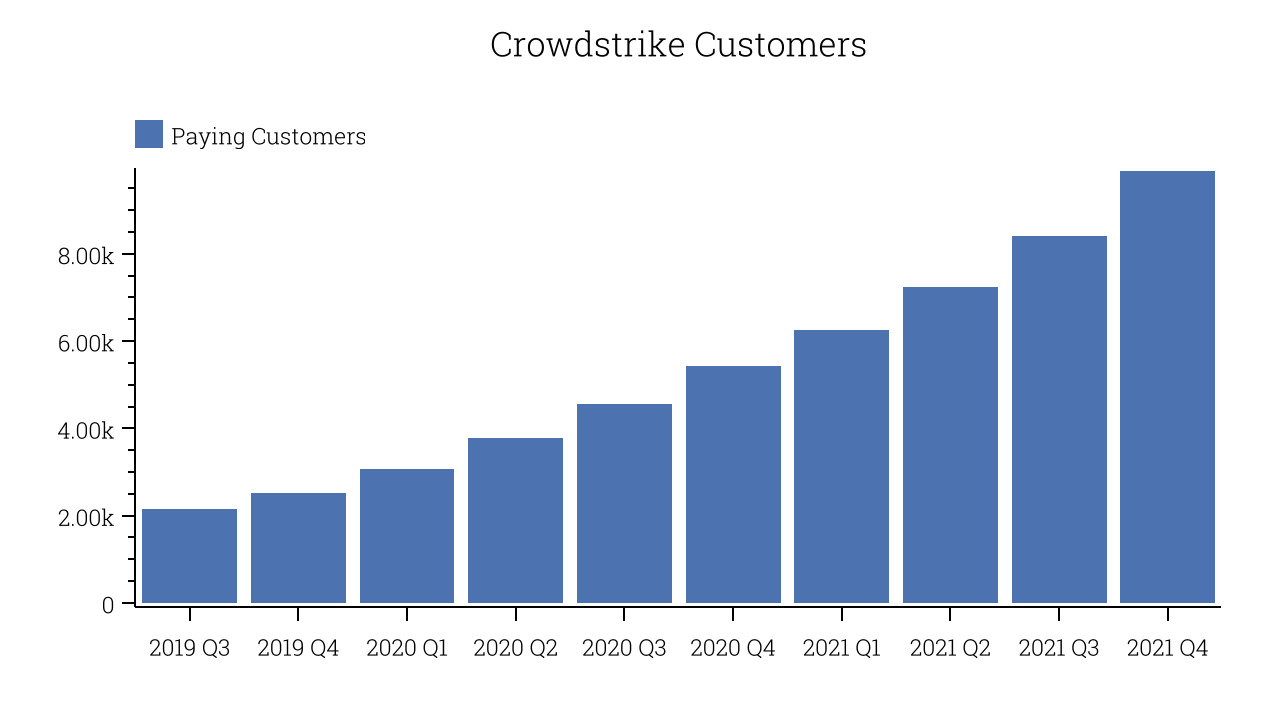

For any software-as-a-service company new customers typically mean new predictable revenue streams. But for Crowdstrike they also mean a better product, because Falcon’s machine learning algorithms get better at predicting and identifying breaches as more customers use it. You can see below that Crowdstrike reported 9,896 customers at the end of the quarter, an increase of 1,480 on last quarter. That is quite a bit better customer growth than last quarter and quite a bit above the typical customer growth we have seen lately, demonstrating that the business itself has good sales momentum. We've no doubt shareholders will take this as an indication that the company's go-to-market strategy is working very well.

Key Takeaways from Crowdstrike's Q4 Results

With market capitalisation of $44.37 billion, more than $1.919 billion in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

We were impressed by the exceptional revenue growth Crowdstrike delivered this quarter. And we were also glad that the revenue guidance for the next quarter exceeded analysts' expectations. On the other hand, it was a little disappointing that the revenue guidance for next year indicates bit of a slow down. Overall, we think this was a strong quarter, that should leave shareholders feeling very positive. While the market has high expectations of Crowdstrike we think it will continue to stand out as one of the best quality SaaS stocks, even more so than before.

The author has no position in any of the stocks mentioned.