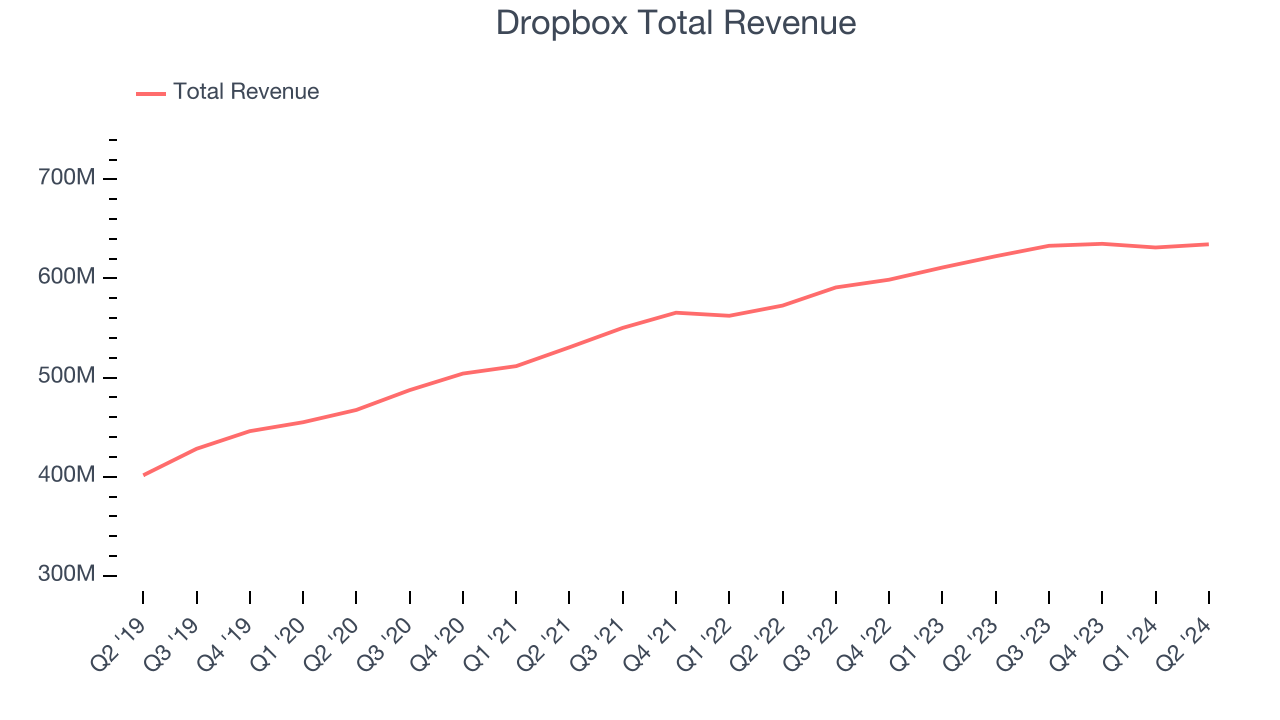

Cloud storage and e-signature company Dropbox (Nasdaq: DBX) reported results in line with analysts' expectations in Q2 CY2024, with revenue up 1.9% year on year to $634.5 million. It made a non-GAAP profit of $0.60 per share, improving from its profit of $0.51 per share in the same quarter last year.

Is now the time to buy Dropbox? Find out by accessing our full research report, it's free.

Dropbox (DBX) Q2 CY2024 Highlights:

- Revenue: $634.5 million vs analyst estimates of $630 million (small beat)

- Adjusted Operating Income: $227.9 million vs analyst estimates of $207.6 million (9.8% beat)

- EPS (non-GAAP): $0.60 vs analyst estimates of $0.52 (14.6% beat)

- Gross Margin (GAAP): 83.1%, up from 81.1% in the same quarter last year

- Free Cash Flow of $224.7 million, up 35.1% from the previous quarter

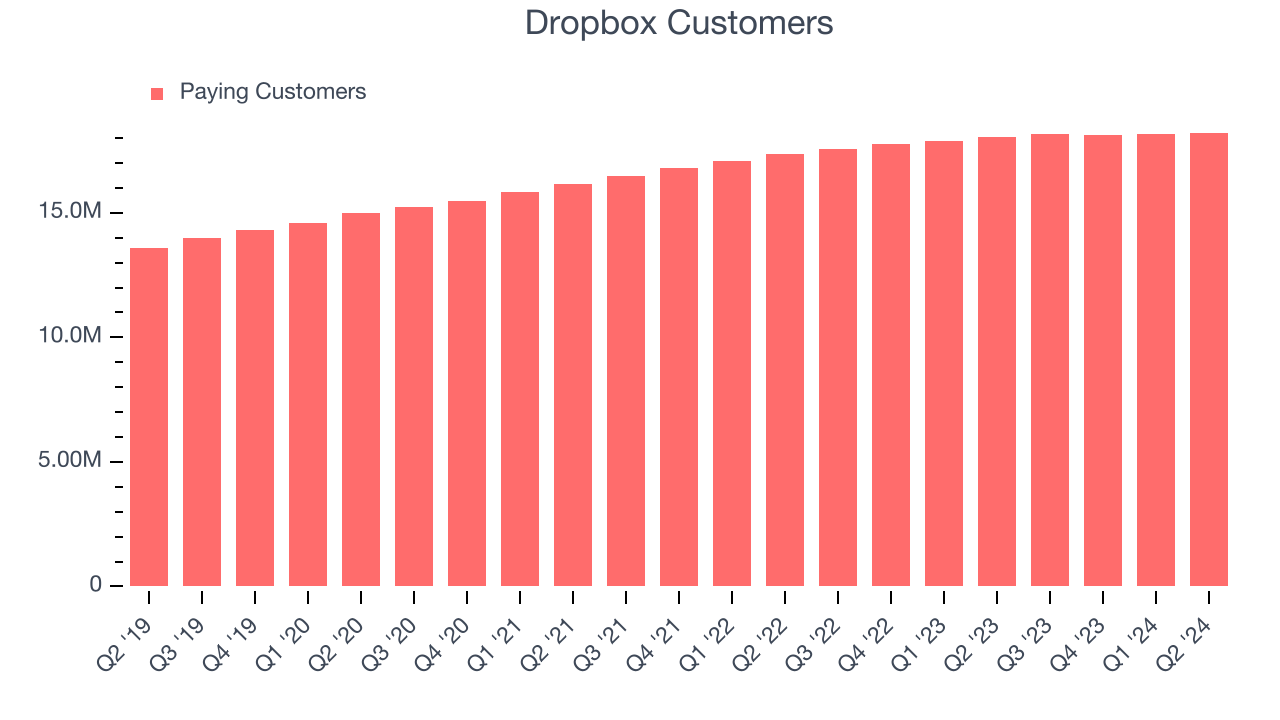

- Customers: 18.22 million, up from 18.16 million in the previous quarter

- Billings: $634.5 million at quarter end, in line with the same quarter last year

- Market Capitalization: $7.16 billion

Founded by the long-serving CEO Drew Houston and Arash Ferdowsi in 2007, Dropbox (NASDAQ:DBX) provides a file hosting cloud platform that helps organizations collaborate and share documents.

Document Management

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

Sales Growth

As you can see below, Dropbox's 7.6% annualized revenue growth over the last three years has been weak, and its sales came in at $634.5 million this quarter.

Dropbox's quarterly revenue was only up 1.9% year on year, which might disappoint some shareholders. However, its revenue increased $3.2 million quarter on quarter, a strong improvement from the $3.7 million decrease in Q1 CY2024. This is a sign of acceleration of growth and very nice to see indeed.

Looking ahead, analysts covering the company were expecting sales to grow 1.3% over the next 12 months before the earnings results announcement.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Customer Growth

Dropbox reported 18.22 million customers at the end of the quarter, an increase of 60,000 from the previous quarter. That's a little better customer growth than last quarter and in line with what we've seen in past quarters, demonstrating that the company has the sales momentum required to drive continued growth. We've no doubt shareholders will take this as an indication that Dropbox's go-to-market strategy is running smoothly.

Key Takeaways from Dropbox's Q2 Results

We were impressed by Dropbox's strong growth in customers this quarter. On the other hand, its billings unfortunately missed analysts' expectations. Overall, this quarter was mixed but with some key positives. The stock traded up 4.8% to $22.77 immediately after reporting.

So should you invest in Dropbox right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.