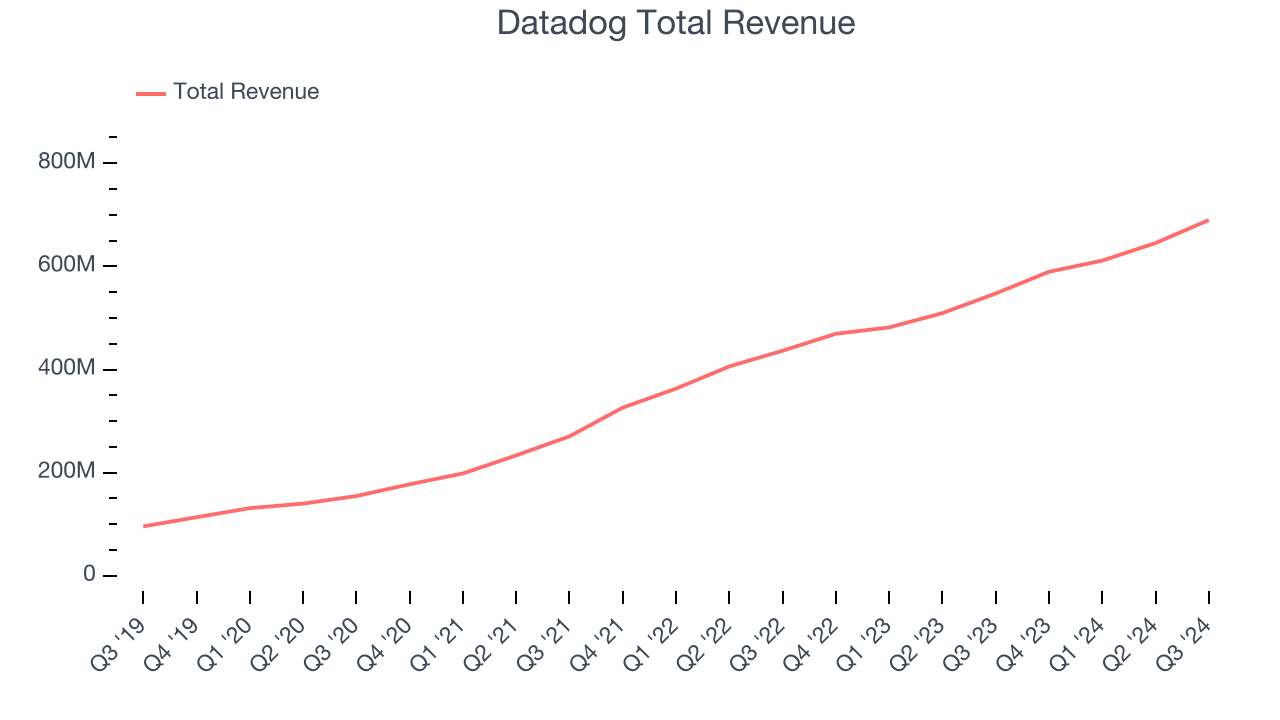

Cloud monitoring software company Datadog (NASDAQ:DDOG) announced better-than-expected revenue in Q3 CY2024, with sales up 26% year on year to $690 million. The company expects next quarter’s revenue to be around $711 million, close to analysts’ estimates. Its non-GAAP profit of $0.46 per share was also 15.7% above analysts’ consensus estimates.

Is now the time to buy Datadog? Find out by accessing our full research report, it’s free.

Datadog (DDOG) Q3 CY2024 Highlights:

- Revenue: $690 million vs analyst estimates of $664.5 million (3.8% beat)

- Adjusted EPS: $0.46 vs analyst estimates of $0.40 (15.7% beat)

- Adjusted Operating Income: $173 million vs analyst estimates of $148.8 million (16.3% beat)

- Revenue Guidance for Q4 CY2024 is $711 million at the midpoint, roughly in line with what analysts were expecting

- Management raised its full-year Adjusted EPS guidance to $1.76 at the midpoint, a 7.3% increase

- Gross Margin (GAAP): 80%, down from 81.1% in the same quarter last year

- Operating Margin: 2.9%, up from -0.8% in the same quarter last year

- Free Cash Flow Margin: 29.5%, up from 22.3% in the previous quarter

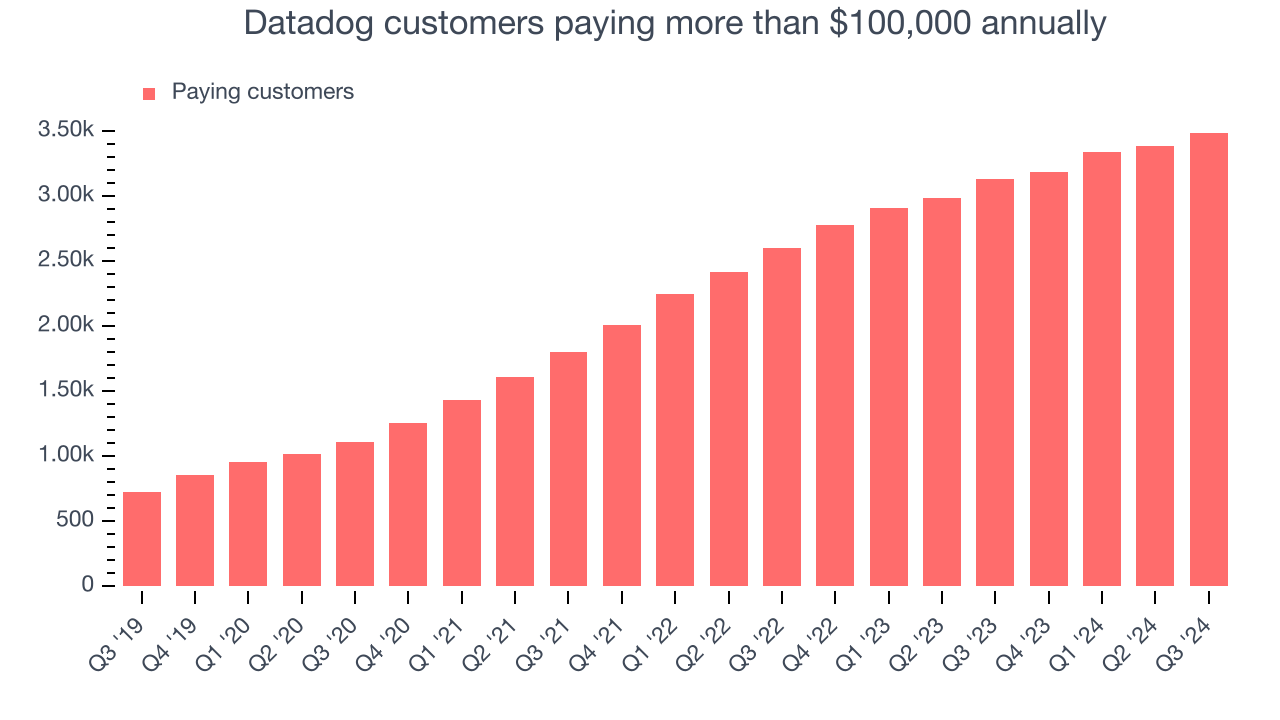

- Customers: 3,490 customers paying more than $100,000 annually

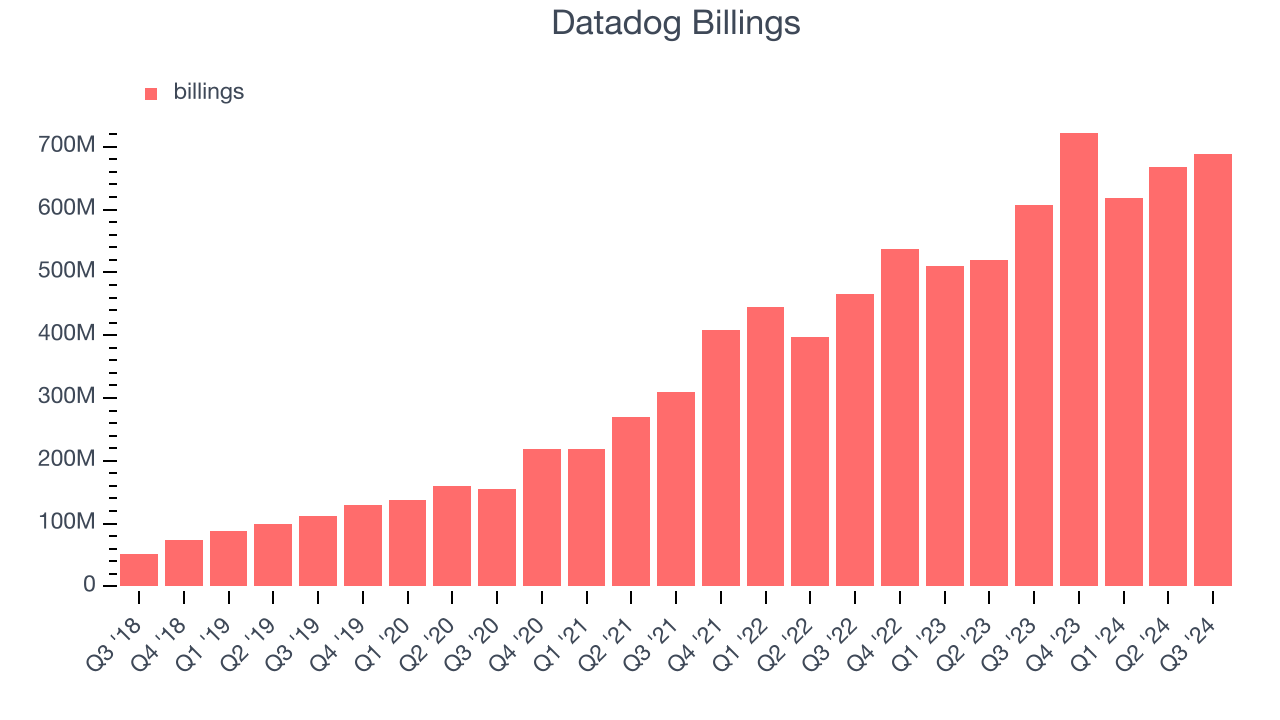

- Billings: $688.6 million at quarter end, up 13.5% year on year

- Market Capitalization: $43.27 billion

"Datadog executed well in the third quarter, with 26% year-over-year revenue growth. We continued to broaden our platform to help our customers observe, secure, and act on their mission-critical cloud applications," said Olivier Pomel, co-founder and CEO of Datadog.

Company Overview

Named after a database the founders had to painstakingly look after at their previous company, Datadog (NASDAQ:DDOG) is a software-as-a-service platform that makes it easier to monitor cloud infrastructure and applications.

Cloud Monitoring

Software is eating the world, increasing organizations’ reliance on digital-only solutions. As more workloads and applications move to the cloud, the reliability of the underlying cloud infrastructure becomes ever more critical and ever more complex. To solve this challenge, companies and their engineering teams have turned to a range of cloud monitoring tools that provide them with the visibility to troubleshoot issues in real-time.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Datadog’s 42.3% annualized revenue growth over the last three years was incredible. This is a great starting point for our analysis because it shows Datadog’s offerings resonate with customers.

This quarter, Datadog reported robust year-on-year revenue growth of 26%, and its $690 million of revenue topped Wall Street estimates by 3.8%. Management is currently guiding for a 20.6% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 20% over the next 12 months, a deceleration versus the last three years. This projection is still healthy and shows the market is factoring in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Billings

In addition to revenue, billings is a non-GAAP metric that sheds additional light on Datadog’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Over the last year, Datadog’s billings growth has been impressive, averaging 24.4% year-on-year increases and punching in at $688.6 million in the latest quarter. This performance was in line with its revenue growth, indicating robust customer demand and a strong sales pipeline. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

Large Customers Growth

This quarter, Datadog reported 3,490 enterprise customers paying more than $100,000 annually, an increase of 100 from the previous quarter. That’s quite a bit more contract wins than last quarter but also quite a bit below what we’ve typically observed over the last year, suggesting that the company may be reinvigorating growth.

Key Takeaways from Datadog’s Q3 Results

We were impressed by Datadog’s optimistic EPS forecast for next quarter, which exceeded analysts’ expectations. We were also glad it had many new large contract wins. On the other hand, revenue guidance was just in line, and its billings missed analysts’ expectations. Holding aside expectations gross margin decreased year on year. The billings miss seems to be driving the move, and shares traded down 3.5% to $123.81 immediately after reporting.

So should you invest in Datadog right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.