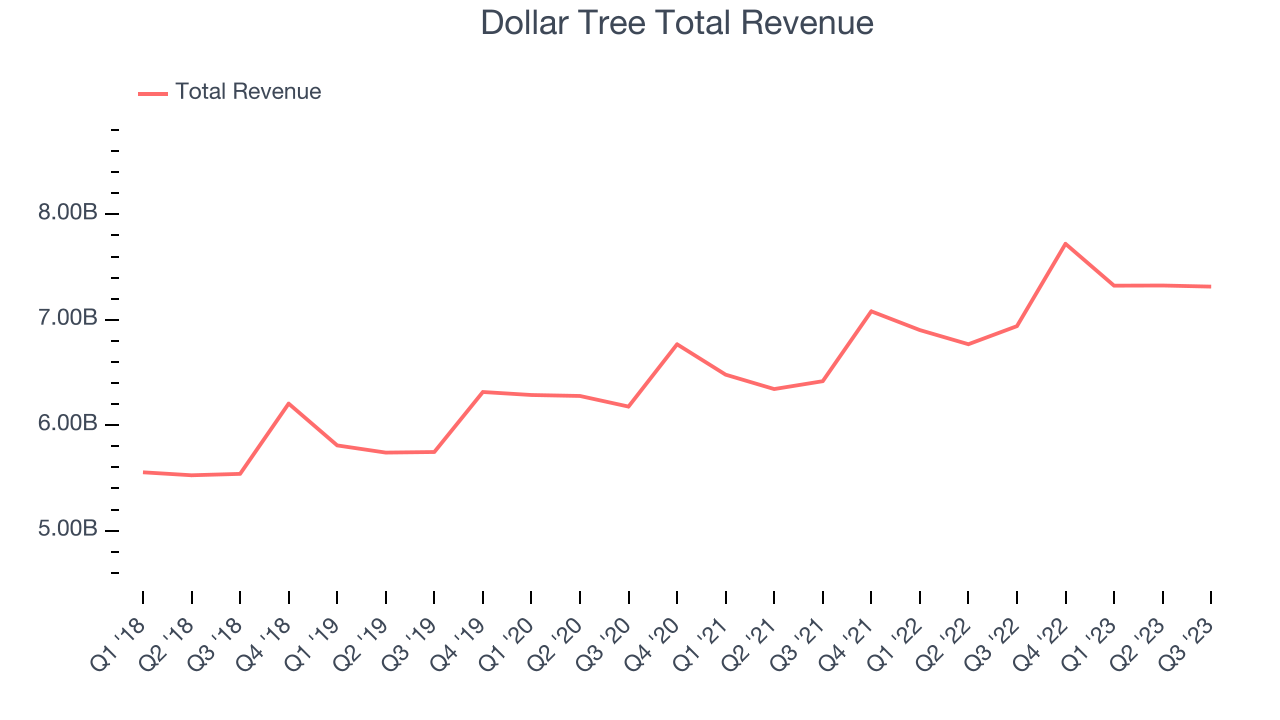

Discount treasure-hunt retailer Dollar Tree (NASDAQ:DLTR) fell short of analysts' expectations in Q3 FY2023, with revenue up 5.4% year on year to $7.31 billion. The company expects next quarter's revenue to be around $8.7 billion, slightly below analysts' estimates. It made a GAAP profit of $0.97 per share, down from its profit of $1.20 per share in the same quarter last year.

Is now the time to buy Dollar Tree? Find out by accessing our full research report, it's free.

Dollar Tree (DLTR) Q3 FY2023 Highlights:

- Revenue: $7.31 billion vs analyst estimates of $7.42 billion (1.4% miss)

- EPS: $0.97 vs analyst expectations of $1.01 (3.7% miss)

- Revenue Guidance for Q4 2023 is $8.7 billion at the midpoint, roughly in line with what analysts were expecting

- Free Cash Flow was -$35.6 million compared to -$177.7 million in the same quarter last year

- Gross Margin (GAAP): 29.8%, in line with the same quarter last year

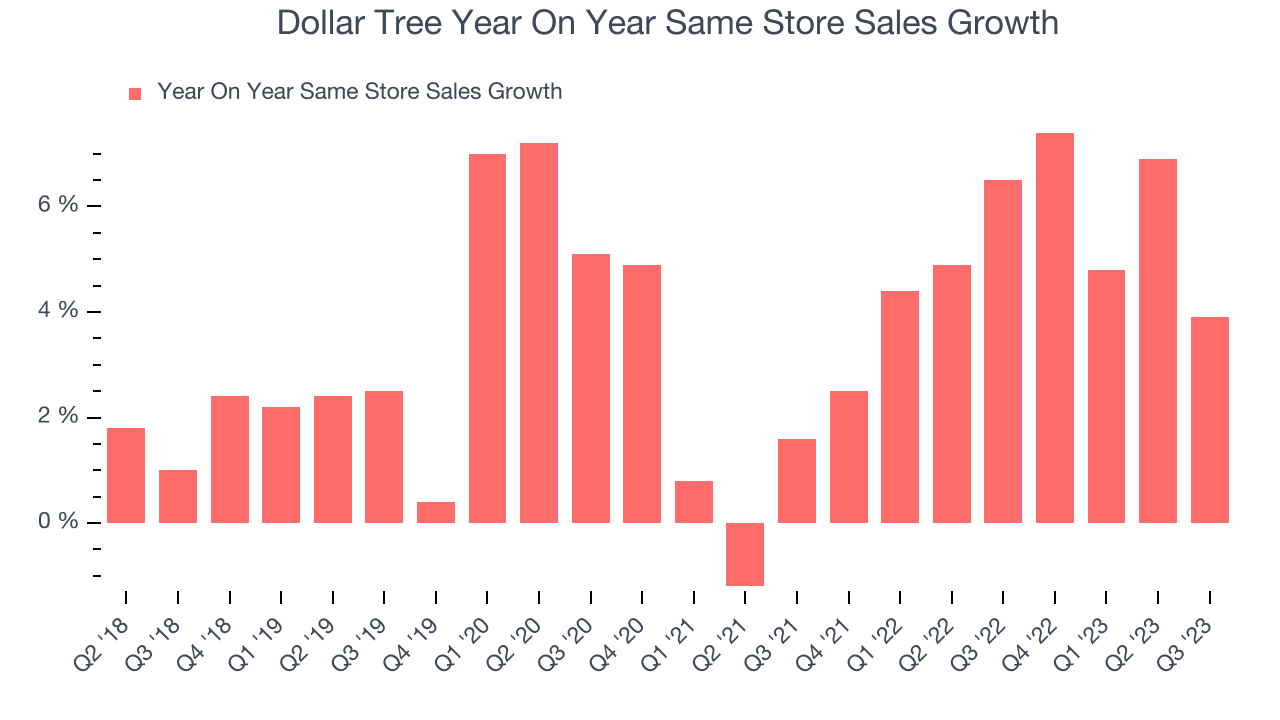

- Same-Store Sales were up 3.9% year on year

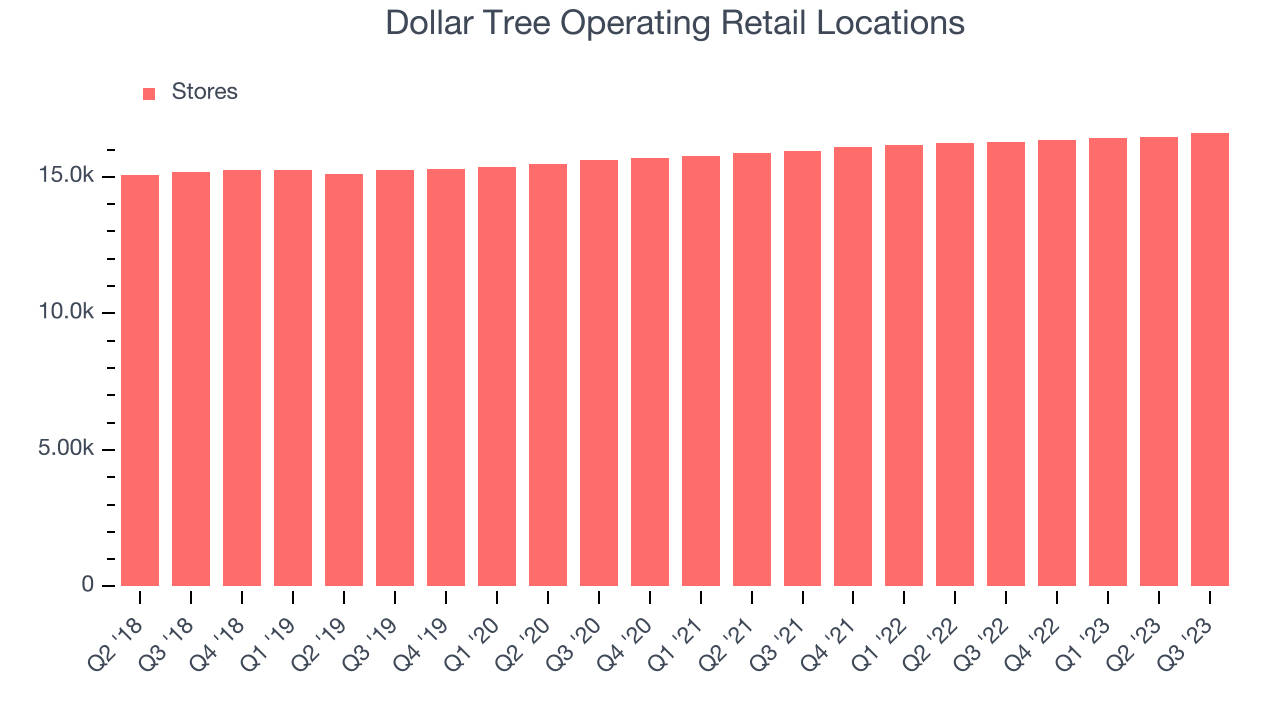

- Store Locations: 16,622 at quarter end, increasing by 329 over the last 12 months

A treasure hunt because there’s no guarantee of consistent product selection, Dollar Tree (NASDAQ:DLTR) is a discount retailer that sells general merchandise and select packaged food at extremely low prices.

Discount Grocery Store

Traditional grocery stores are go-tos for many families, but discount grocers serve those who may not have a traditional grocery store nearby or who may have different spending thresholds. Certain rural or lower-income areas simply don’t have a grocery store. Additionally, some lower-income families would prefer to buy in smaller quantities than available at most stores (think one or two paper towel rolls at a time). While online competition threatens all of retail, grocery is one of the least penetrated because of the nature of buying food. Furthermore, those buying small quantities for immediate need are even less likely to leverage e-commerce for these purposes.

Sales Growth

Dollar Tree is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

As you can see below, the company's annualized revenue growth rate of 6% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre , but to its credit, it opened new stores and grew sales at existing, established stores.

This quarter, Dollar Tree grew its revenue by 5.4% year on year, missing Wall Street's expectations. The company is guiding for a 11.3% year-on-year revenue decline next quarter to $8.7 billion, a reversal from the 9% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts expect sales to grow 7.9% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

When a retailer like Dollar Tree keeps its store footprint steady, it usually means that demand is stable and it's focused on improving operational efficiency to increase profitability. Dollar Tree's store count increased by 329 locations, or 2%, over the last 12 months to 16,622 total retail locations in the most recently reported quarter.

Taking a step back, the company has only opened a few new stores over the last eight quarters, averaging 2% annual growth in new locations. Although it's expanded its presence, this sluggish store growth lags other retailers. A flat store base means that revenue growth must come from increased e-commerce sales or higher foot traffic and sales per customer at existing stores.

Same-Store Sales

Dollar Tree's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 5.2% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Dollar Tree is reaching more customers and growing sales.

In the latest quarter, Dollar Tree's same-store sales rose 3.9% year on year. This growth was a deceleration from the 6.5% year-on-year increase it posted 12 months ago, showing the business is still performing well but lost a bit of steam.

Key Takeaways from Dollar Tree's Q3 Results

With a market capitalization of $25.53 billion, a $444.6 million cash balance, and positive free cash flow over the last 12 months, we're confident that Dollar Tree has the resources needed to pursue a high-growth business strategy.

It was great to see Dollar Tree's strong earnings forecast for next quarter, which exceeded analysts' expectations. On the other hand, this quarter's revenue and its full-year revenue guidance slightly missed Wall Street's estimates, driven by lower-than-expected same-store sales growth. Customer traffic, however, did increase at all three of its brands (Dollar Tree, Family Dollar, Enterprise). Zooming out, we think this was a decent, albeit mixed, quarter, showing that the company is staying on track. The market was likely expecting more, and the stock is down 2.9% after reporting, trading at $112.76 per share.

So should you invest in Dollar Tree right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.