Dollar Tree (NASDAQ:DLTR) Posts Better-Than-Expected Sales In Q3

Adam Hejl /

December 4, 2024

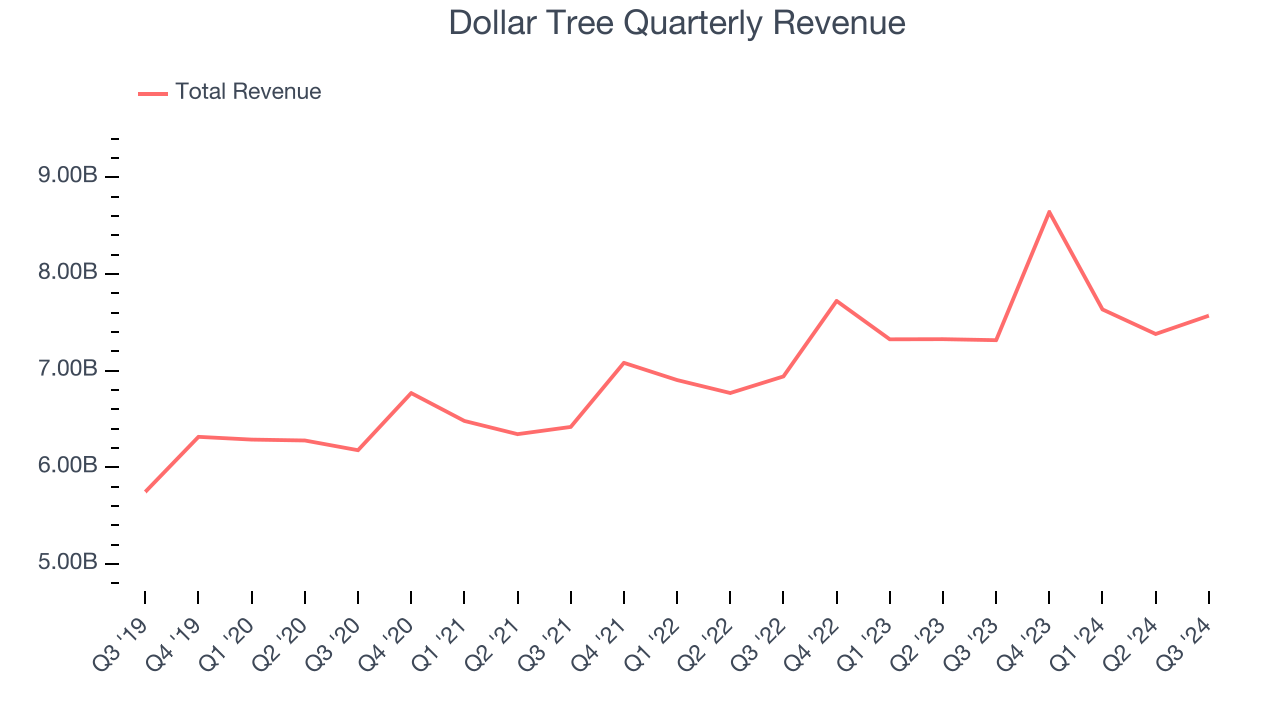

Discount treasure-hunt retailer Dollar Tree (NASDAQ:DLTR) reported revenue ahead of Wall Street’s expectations in Q3 CY2024, with sales up 3.5% year on year to $7.57 billion. The company expects next quarter’s revenue to be around $8.2 billion, close to analysts’ estimates. Its non-GAAP profit of $1.12 per share was 4.1% above analysts’ consensus estimates.

Is now the time to buy Dollar Tree? Find out in our full research report.

Dollar Tree (DLTR) Q3 CY2024 Highlights:

- Revenue: $7.57 billion vs analyst estimates of $7.44 billion (3.5% year-on-year growth, 1.7% beat)

- Adjusted EPS: $1.12 vs analyst estimates of $1.08 (4.1% beat)

- Adjusted EBITDA: $673.8 million vs analyst estimates of $591.1 million (8.9% margin, 14% beat)

- Revenue Guidance for Q4 CY2024 is $8.2 billion at the midpoint, roughly in line with what analysts were expecting

- Management slightly raised its full-year Adjusted EPS guidance to $5.41 at the midpoint

- Operating Margin: 4.4%, in line with the same quarter last year

- Free Cash Flow was $359.2 million, up from -$35.6 million in the same quarter last year

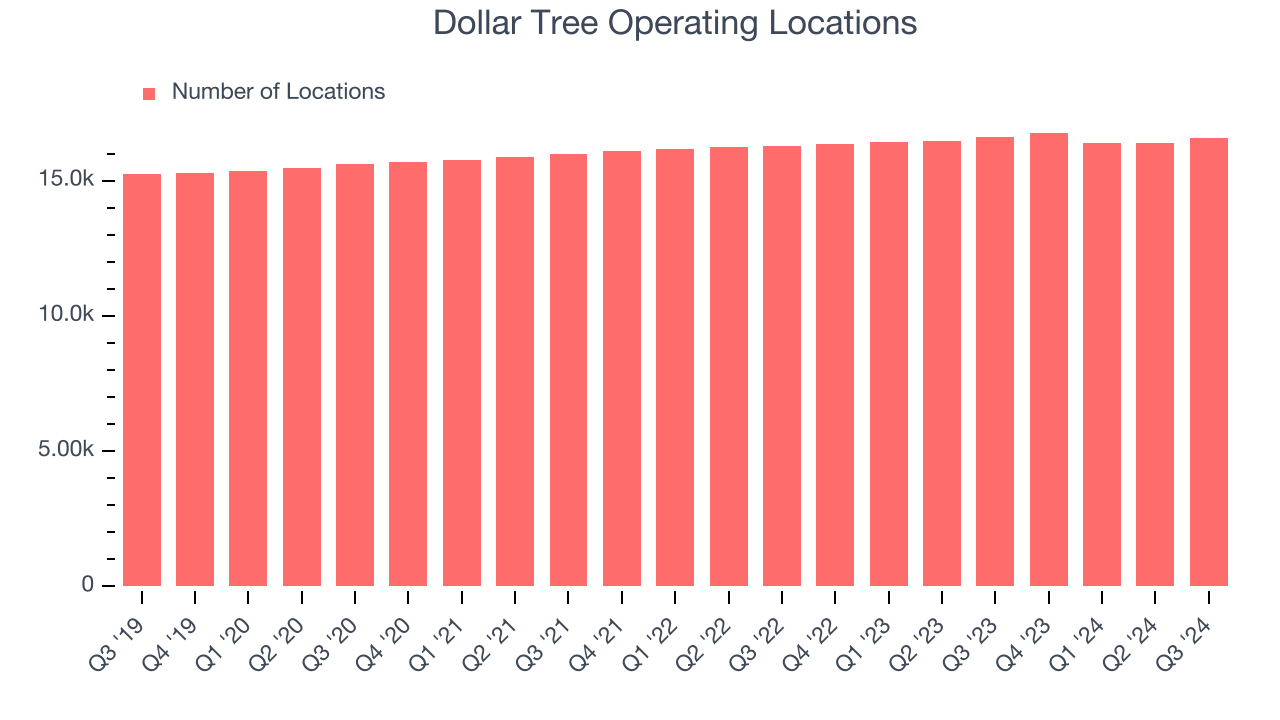

- Locations: 16,590 at quarter end, down from 16,622 in the same quarter last year

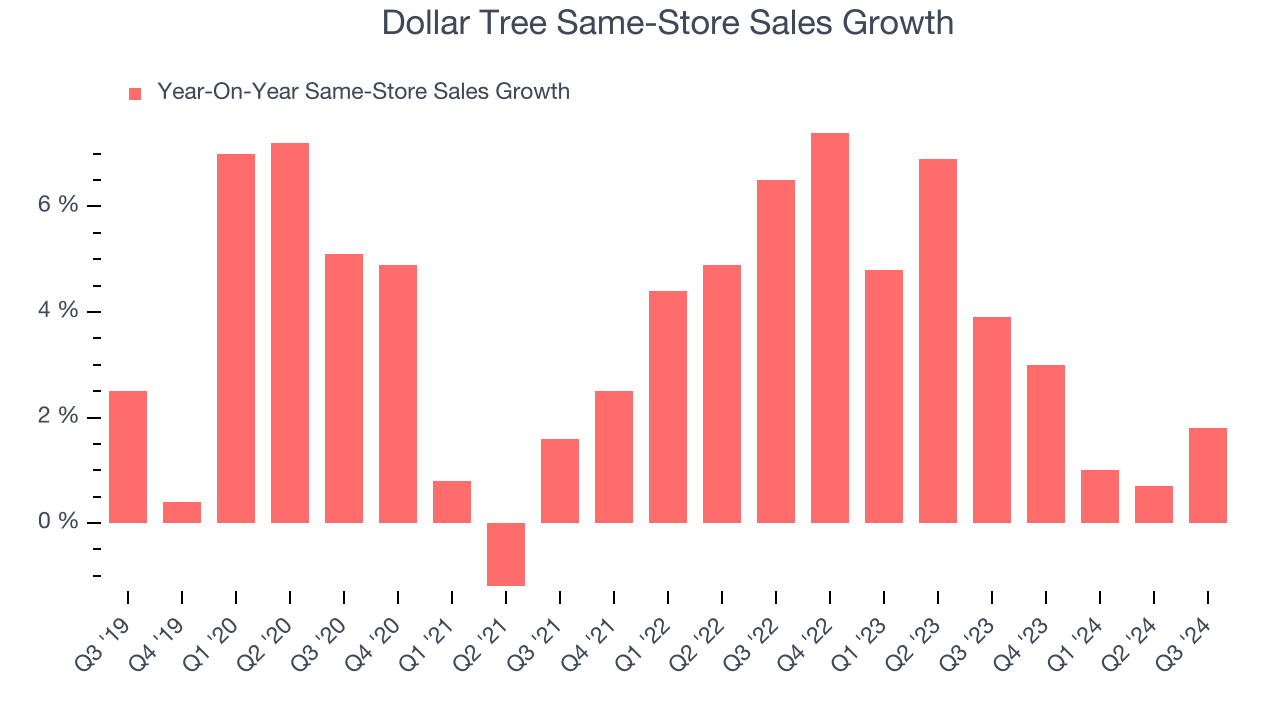

- Same-Store Sales rose 1.8% year on year (3.9% in the same quarter last year)

- Market Capitalization: $15.58 billion

Company Overview

A treasure hunt because there’s no guarantee of consistent product selection, Dollar Tree (NASDAQ:DLTR) is a discount retailer that sells general merchandise and select packaged food at extremely low prices.

Discount Grocery Store

Traditional grocery stores are go-tos for many families, but discount grocers serve those who may not have a traditional grocery store nearby or who may have different spending thresholds. Certain rural or lower-income areas simply don’t have a grocery store. Additionally, some lower-income families would prefer to buy in smaller quantities than available at most stores (think one or two paper towel rolls at a time). While online competition threatens all of retail, grocery is one of the least penetrated because of the nature of buying food. Furthermore, those buying small quantities for immediate need are even less likely to leverage e-commerce for these purposes.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Dollar Tree is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences consumer purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth.

As you can see below, Dollar Tree’s sales grew at a tepid 5.8% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts), but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, Dollar Tree reported modest year-on-year revenue growth of 3.5% but beat Wall Street’s estimates by 1.7%. Company management is currently guiding for a 5.1% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last five years. This projection is underwhelming and indicates its products will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Dollar Tree operated 16,590 locations in the latest quarter. It has generally opened new stores over the last two years and averaged 1.1% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Dollar Tree’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 3.7% per year. This performance suggests its measured rollout of new stores is beneficial for shareholders. We like this backdrop because it gives Dollar Tree multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, Dollar Tree’s same-store sales rose 1.8% year on year. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Dollar Tree can reaccelerate growth.

Key Takeaways from Dollar Tree’s Q3 Results

We were impressed by how significantly Dollar Tree blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter slightly missed. Overall, this quarter had some key positives. The stock traded up 4.8% to $76 immediately after reporting.

So should you invest in Dollar Tree right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.