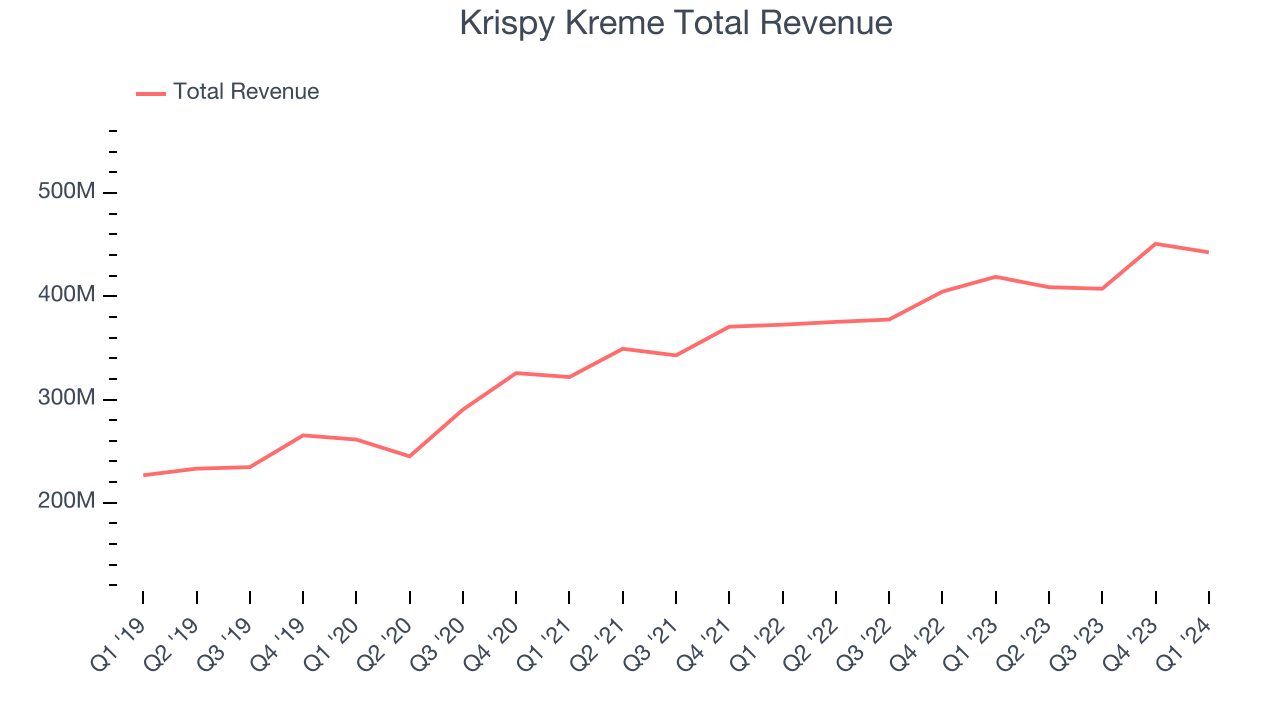

Doughnut chain Krispy Kreme (NASDAQ:DNUT) reported Q1 CY2024 results exceeding Wall Street analysts' expectations, with revenue up 5.7% year on year to $442.7 million. It made a non-GAAP profit of $0.07 per share, down from its profit of $0.09 per share in the same quarter last year.

Is now the time to buy Krispy Kreme? Find out by accessing our full research report, it's free.

Krispy Kreme (DNUT) Q1 CY2024 Highlights:

- Revenue: $442.7 million vs analyst estimates of $434.1 million (2% beat)

- EPS (non-GAAP): $0.07 vs analyst expectations of $0.06 (in line)

- Gross Margin (GAAP): 29.5%, up from 26.2% in the same quarter last year

- Free Cash Flow was -$46.77 million compared to -$31.31 million in the previous quarter

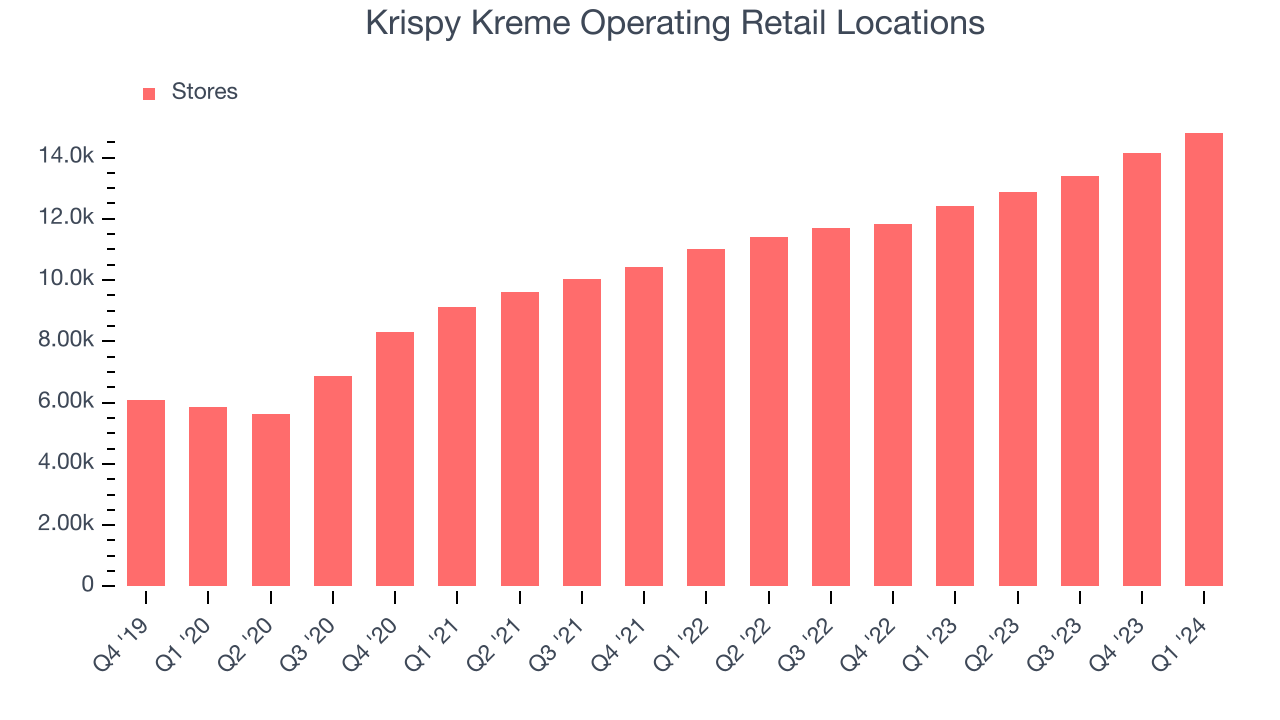

- Store Locations: 14,814 at quarter end, increasing by 2,404 over the last 12 months

- Market Capitalization: $2.14 billion

“First-quarter results exceeded our expectations, driven by increased digital sales and strong consumer demand, highlighted by a record setting Valentine’s Day with specialty doughnuts available in 33 countries around the world,” said Josh Charlesworth, CEO.

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ:DNUT) is one of the most beloved and well-known fast-food chains in the world.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

Krispy Kreme is larger than most restaurant chains and benefits from economies of scale, giving it an edge over its smaller competitors.

As you can see below, the company's annualized revenue growth rate of 14.5% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it added more dining locations and expanded its reach.

This quarter, Krispy Kreme reported solid year-on-year revenue growth of 5.7%, and its $442.7 million in revenue outperformed Wall Street's estimates by 2%. Looking ahead, Wall Street expects sales to grow 6.7% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Number of Stores

A restaurant chain's total number of dining locations often determines how much revenue it can generate.

When a chain like Krispy Kreme is opening new restaurants, it usually means it's investing for growth because there's healthy demand for its meals and there are markets where the concept has few or no locations. Krispy Kreme's restaurant count increased by 2,404, or 19.4%, over the last 12 months to 14,814 locations in the most recently reported quarter.

Over the last two years, Krispy Kreme has rapidly opened new restaurants, averaging 15.9% annual increases in new locations. This growth is among the fastest in the restaurant sector. Analyzing a restaurant's location growth is important because expansion means Krispy Kreme has more opportunities to feed customers and generate sales.

Key Takeaways from Krispy Kreme's Q1 Results

We enjoyed seeing Krispy Kreme exceed analysts' revenue expectations this quarter as its organic sales outperformed (6.7% vs estimates of 5.8%). We were also glad its full-year earnings guidance exceeded Wall Street's estimates. On the other hand, its gross margin fell short. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 4.4% after reporting and currently trades at $13.25 per share.

So should you invest in Krispy Kreme right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.