DocuSign (DOCU) Delivers Strong Q4, Guides For Growth To Continue In FY 2022

Adam Hejl /

March 11, 2021

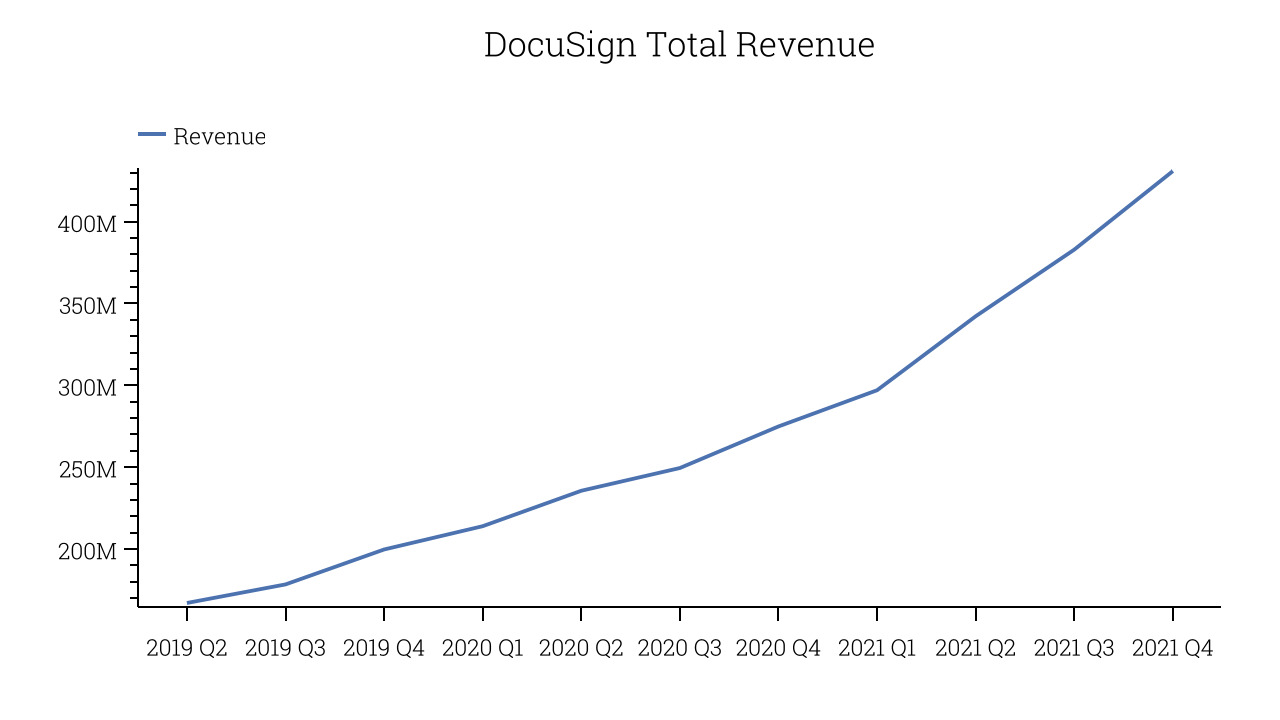

E-signature company DocuSign (DOCU) reported Q4 FY2021 results topping analyst expectations, with revenue up 56.75% year on year to $430.9 million. DocuSign made a GAAP loss of $72.41 million, down on its loss of $47.41 million, in the same quarter last year.

DocuSign (DOCU) Q4 FY2021 Highlights:

- Revenue: $430.9 million vs analyst estimates of $408.0 million (5.6% beat)

- EPS (non-GAAP): $0.37 vs analyst estimates of $0.22 ($0.15 beat)

- Revenue guidance for Q1 2022 is $434.0 million at the midpoint, above analyst estimates of $418.7 million

- Management's revenue guidance for FY2022 of $1.968 billion at the midpoint, predicting 35.44% growth (vs 44.69% in FY2021)

- Free cash flow of $43.98 million, up 15.59% from previous quarter

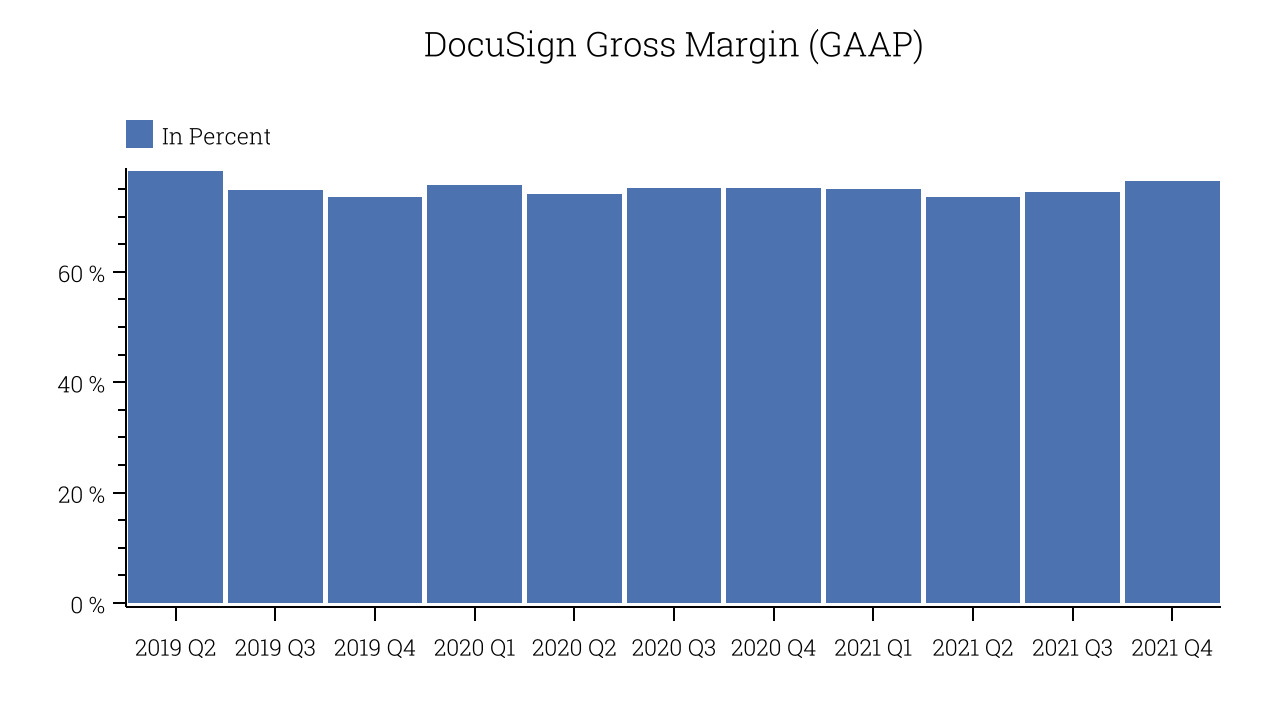

- Gross Margin (GAAP): 76.43%, up from 74.45% previous quarter

"Fiscal 2021 was a milestone year for DocuSign. We became a pillar of the 'anywhere economy' that lets people increasingly do anything in life and work from anywhere," said Dan Springer, CEO of DocuSign.

Frictionless Agreements

Founded in 2003, DocuSign (DOCU) is the pioneer of e-signature and offers software as a service that allows people and organisations to sign legally binding documents electronically. The platforms digitizes the whole signing process from preparing the agreement, making sure that correct people received it, to storing it after it is signed. DocuSign makes the overall process of signing a document a lot faster and significantly reduces error rates, and it's integrations with many other software platforms (such as Google Drive or Salesforce) allows companies to generate and send new agreements to their customers at the click of the button.

DocuSign can be an interesting company to watch because it is profiting from the overall digitization of the economy as the product is useful to any company, large or small, across a wide range of industries. The Covid pandemic has accelerated the digital transformation of how we work and do business and the e-signature products like DocuSign, Dropbox’s HelloSign or Adobe’s Sign have been clear beneficiaries of it.

As you can see below, DocuSign's revenue growth has been impressive over the last twelve months, growing from $274.9 million to $430.9 million.

This was another standout quarter with the revenue up a splendid 56.75% year on year. On top of that, revenue increased $47.98 million quarter on quarter, a solid improvement on the $40.71 million increase in Q3 2021, and happily, a slight acceleration of growth.

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers.

DocuSign's gross profit margin, an important metric measuring how much money there is left after paying for servers, licences, technical support and other necessary running expenses was at 76.43% in Q4. That means that from every $1 in revenue the company had $0.76 left to spend on developing new products, marketing & sales and the general administrative overhead. Significantly up from the last quarter, this is a good gross margin that will allow DocuSign to fund large investments in product and sales during periods of rapid growth and be profitable when it reaches maturity.

Key Takeaways from DocuSign's Q4 Results

With market capitalisation of $40.67 billion, more than $773.5 million in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

We were impressed by the exceptional revenue growth DocuSign delivered this quarter. And we were also glad that the revenue guidance for the next quarter exceeded analysts' expectations. On the other hand, it was disappointing that the revenue guidance for next year was on the weaker side. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. Therefore, we think DocuSign will continue to stand out as a compelling growth stock, arguably even more so than before.

The author has no position in any of the stocks mentioned.