DocuSign (NASDAQ:DOCU) Surprises With Q2 Sales, Stock Jumps 15.5%

Kayode Omotosho /

September 8, 2022

E-signature company DocuSign (DOCU) beat analyst expectations in Q2 FY2023 quarter, with revenue up 21.5% year on year to $622.1 million. The company expects that next quarter's revenue would be around $626 million, which is the midpoint of the guidance range. That was in roughly line with analyst expectations. DocuSign made a GAAP loss of $45 million, down on its loss of $25.5 million, in the same quarter last year.

Is now the time to buy DocuSign? Access our full analysis of the earnings results here, it's free.

DocuSign (DOCU) Q2 FY2023 Highlights:

- Revenue: $622.1 million vs analyst estimates of $602.2 million (3.3% beat)

- EPS (non-GAAP): $0.44 vs analyst estimates of $0.42 (4.3% beat)

- Revenue guidance for Q3 2023 is $626 million at the midpoint, roughly in line with what analysts were expecting

- The company reconfirmed revenue guidance for the full year, at $2.47 billion at the midpoint

- Free cash flow of $105.4 million, down 39.5% from previous quarter

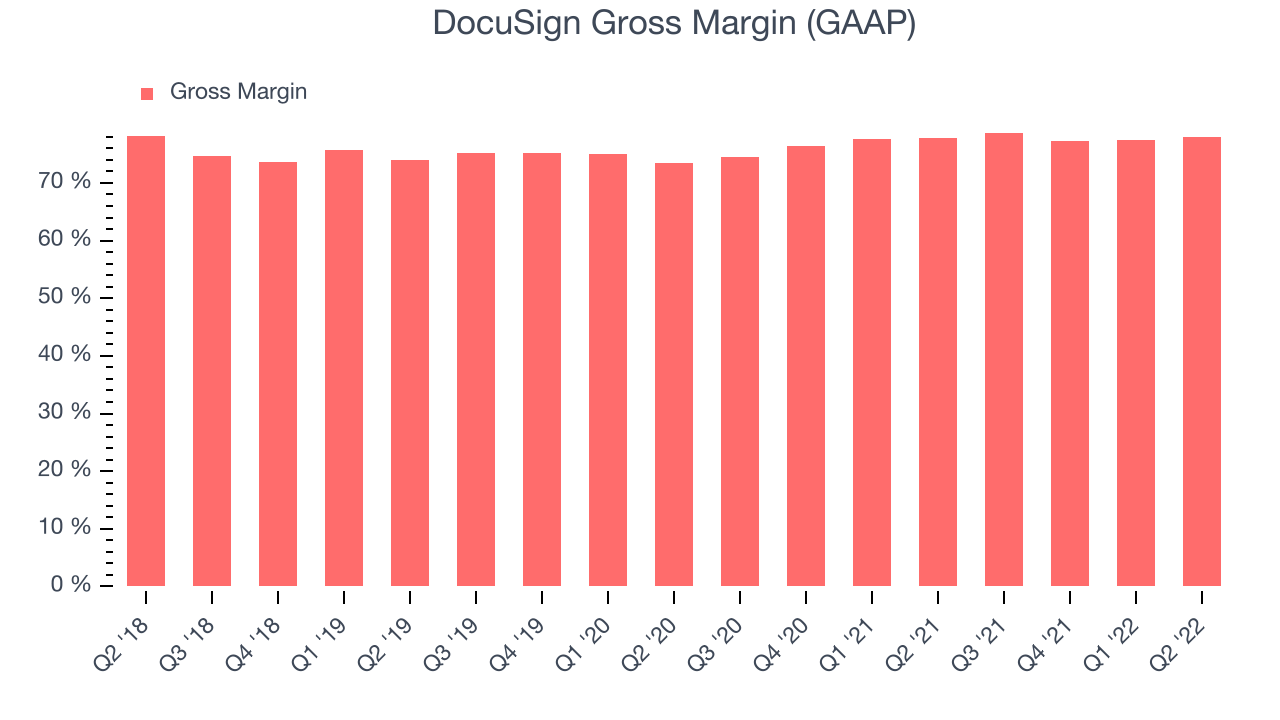

- Gross Margin (GAAP): 78%, in line with same quarter last year

"We delivered solid Q2 results, with a strong finish to the first half of the year. These results reflect the focus and dedication of our team on execution during this transition period, with a stronger foundation in place to deliver in the second half of the year. We enter this next phase with a clear set of vital few deliverables for our people initiatives and product roadmap, while driving sustainable and profitable growth at scale," said Maggie Wilderotter, DocuSign's Interim CEO and Board Chair.

Founded by Seattle-based entrepreneur Tom Gonser, DocuSign (NASDAQ:DOCU) is the pioneer of e-signature and offers software as a service that allows people and organisations to sign legally binding documents electronically.

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

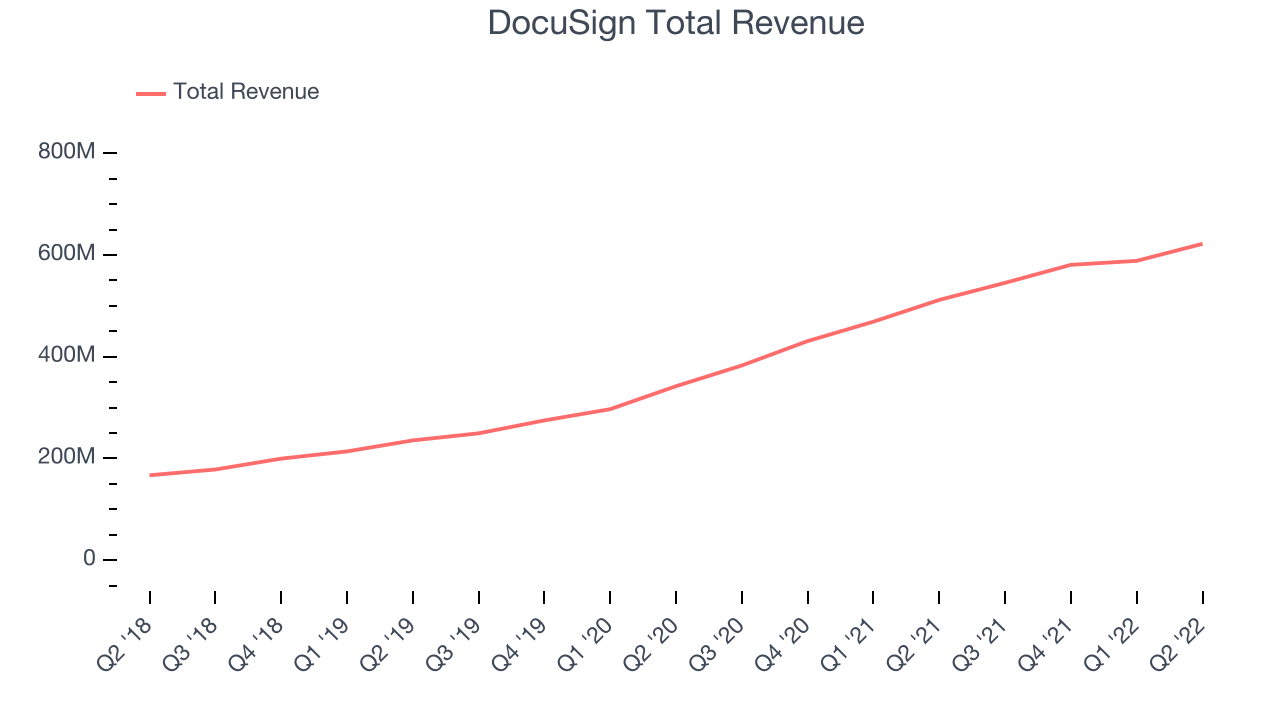

Sales Growth

As you can see below, DocuSign's revenue growth has been very strong over the last year, growing from quarterly revenue of $511.8 million, to $622.1 million.

This quarter, DocuSign's quarterly revenue was once again up a very solid 21.5% year on year. On top of that, revenue increased $33.4 million quarter on quarter, a very strong improvement on the $7.86 million increase in Q1 2023, which shows acceleration of growth, and is great to see.

Guidance for the next quarter indicates DocuSign is expecting revenue to grow 14.7% year on year to $626 million, slowing down from the 42.4% year-over-year increase in revenue the company had recorded in the same quarter last year. Ahead of the earnings results the analysts covering the company were estimating sales to grow 11.8% over the next twelve months.

In volatile times like these we look for robust businesses with strong pricing power. Unknown to most investors, this company is one of the highest-quality software companies in the world, and their software products have been the default standard in critical industries for decades. The result is an impressive business that is up an incredible 18,152% since the IPO. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. DocuSign's gross profit margin, an important metric measuring how much money there is left after paying for servers, licenses, technical support and other necessary running expenses was at 78% in Q2.

That means that for every $1 in revenue the company had $0.78 left to spend on developing new products, marketing & sales and the general administrative overhead. This is a good gross margin that allows companies like DocuSign to fund large investments in product and sales during periods of rapid growth and be profitable when they reach maturity. It is good to see that the gross margin is staying stable which indicates that DocuSign is doing a good job controlling costs and is not under pressure from competition to lower prices.

Key Takeaways from DocuSign's Q2 Results

With a market capitalization of $11 billion, more than $994.7 million in cash and with free cash flow over the last twelve months being positive, the company is in a very strong position to invest in growth.

It was good to see DocuSign outperform Wall St’s revenue expectations this quarter. That feature of these results really stood out as a positive. Zooming out, we think this was a decent quarter, showing the company is staying on target. The company is up 15.5% on the results and currently trades at $67 per share.

Should you invest in DocuSign right now? It is important that you take into account its valuation and business qualities, as well as what happened in the latest quarter. We look at that in our actionable report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 70% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned.