E-signature company DocuSign (DOCU) reported results ahead of analysts' expectations in Q4 FY2024, with revenue up 8% year on year to $712.4 million. The company also expects next quarter's revenue to be around $706 million, slightly above analysts' estimates. It made a non-GAAP profit of $0.76 per share, improving from its profit of $0.65 per share in the same quarter last year.

DocuSign (DOCU) Q4 FY2024 Highlights:

- Revenue: $712.4 million vs analyst estimates of $699.4 million (1.9% beat)

- EPS (non-GAAP): $0.76 vs analyst estimates of $0.65 (17.5% beat)

- Revenue Guidance for Q1 2025 is $706 million at the midpoint, above analyst estimates of $700.1 million

- Management's revenue guidance for the upcoming financial year 2025 is $2.92 billion at the midpoint, in line with analyst expectations and implying 5.8% growth (vs 9.8% in FY2024)

- Free Cash Flow of $248.6 million, similar to the previous quarter

- Gross Margin (GAAP): 79.2%, in line with the same quarter last year

- Market Capitalization: $10.7 billion

Founded by Seattle-based entrepreneur Tom Gonser, DocuSign (NASDAQ:DOCU) is the pioneer of e-signature and offers software as a service that allows people and organisations to sign legally binding documents electronically.

The platform digitizes the whole signing process from preparing the agreement, making sure that the correct people receive it, to storing it after it is signed. DocuSign makes the overall process of signing a document a lot faster and significantly reduces error rates, and its integrations with many other software platforms (such as Google Drive or Salesforce) allow companies to generate and send new agreements to their customers at the click of the button. It is an interesting company to watch because it is profiting from the overall digitization of the economy as the product is useful to any company, large or small, across a wide range of industries.

Document Management

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

DocuSign is competing with products like Dropbox’s (NASDAQ:DBX) HelloSign or Adobe Sign (NASDAQ:ADBE).

Sales Growth

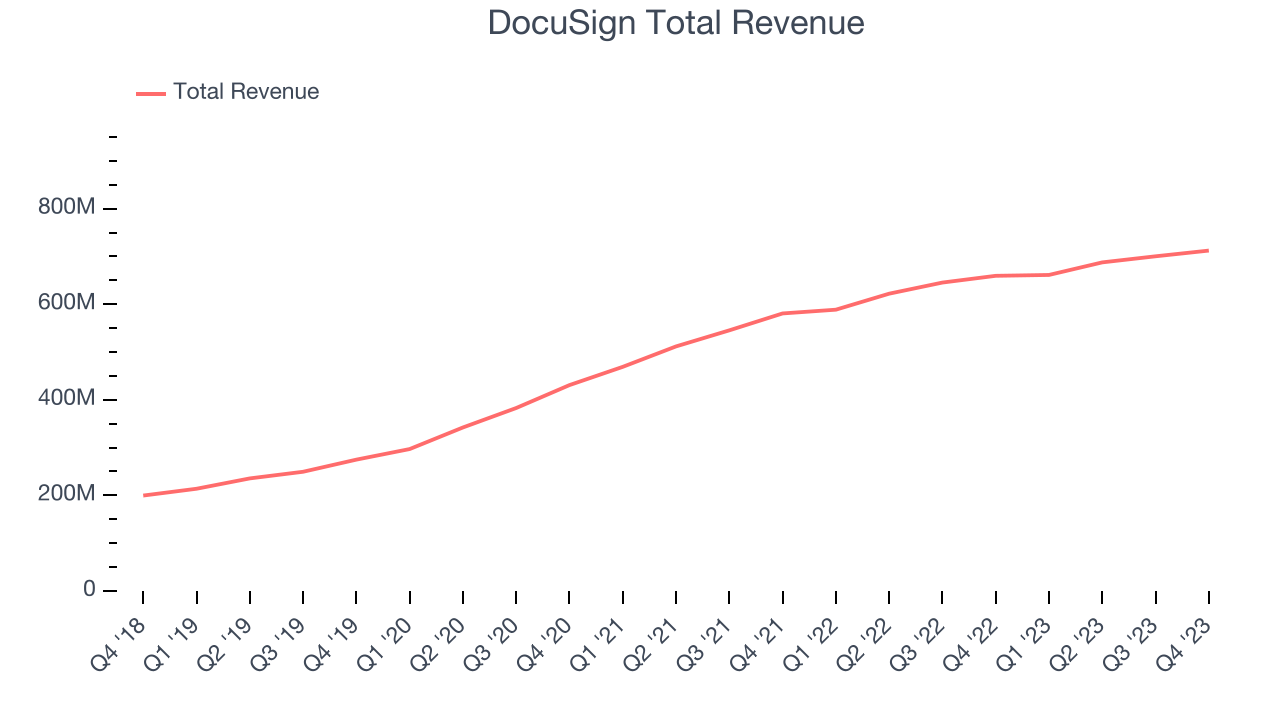

As you can see below, DocuSign's revenue growth has been mediocre over the last two years, growing from $580.8 million in Q4 FY2022 to $712.4 million this quarter.

DocuSign's quarterly revenue was only up 8% year on year, which might disappoint some shareholders. Looking at the last two quarters, we can see that revenue increased by $11.97 million in Q4 compared to $12.73 million in Q3 2024. We'd prefer see growing absolute levels of quarter on quarter revenue gains.

Next quarter's guidance suggests that DocuSign is expecting revenue to grow 6.7% year on year to $706 million, slowing down from the 12.3% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $2.92 billion at the midpoint, growing 5.8% year on year compared to the 9.8% increase in FY2024.

Profitability

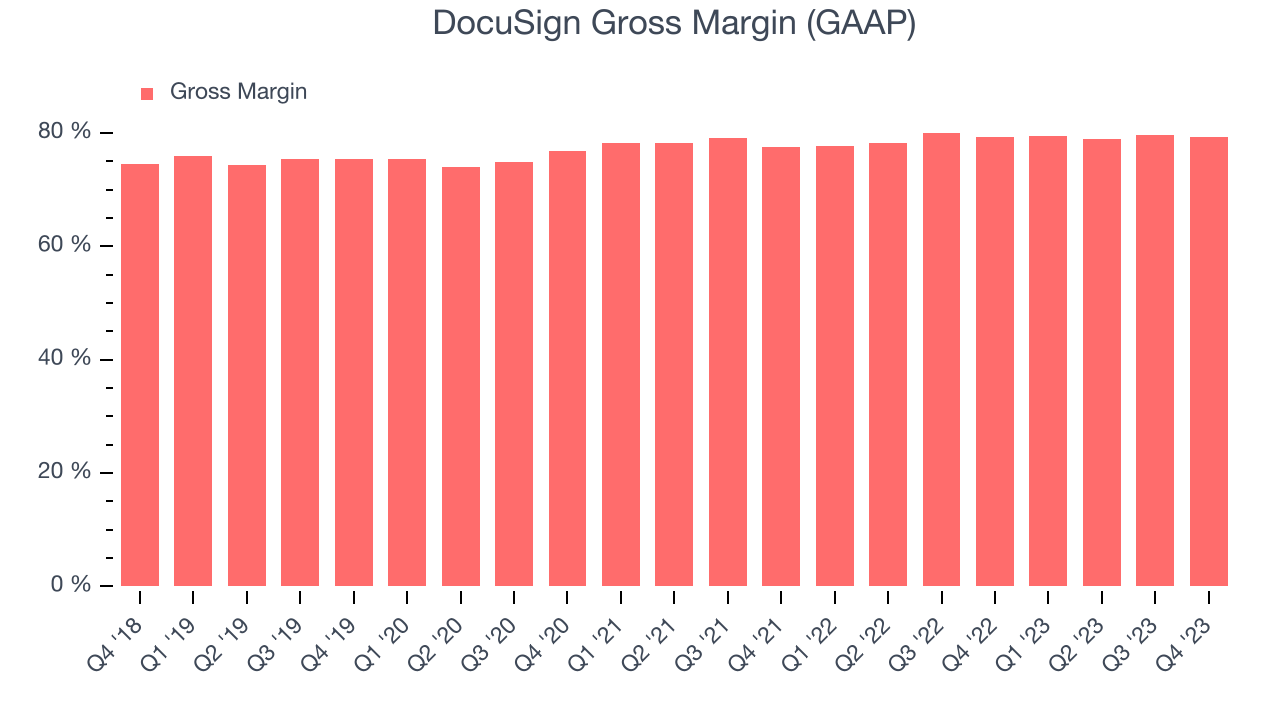

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. DocuSign's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 79.2% in Q4.

That means that for every $1 in revenue the company had $0.79 left to spend on developing new products, sales and marketing, and general administrative overhead. DocuSign's impressive gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity. It's also comforting to see its gross margin remain stable, indicating that DocuSign is controlling its costs and not under pressure from its competitors to lower prices.

Cash Is King

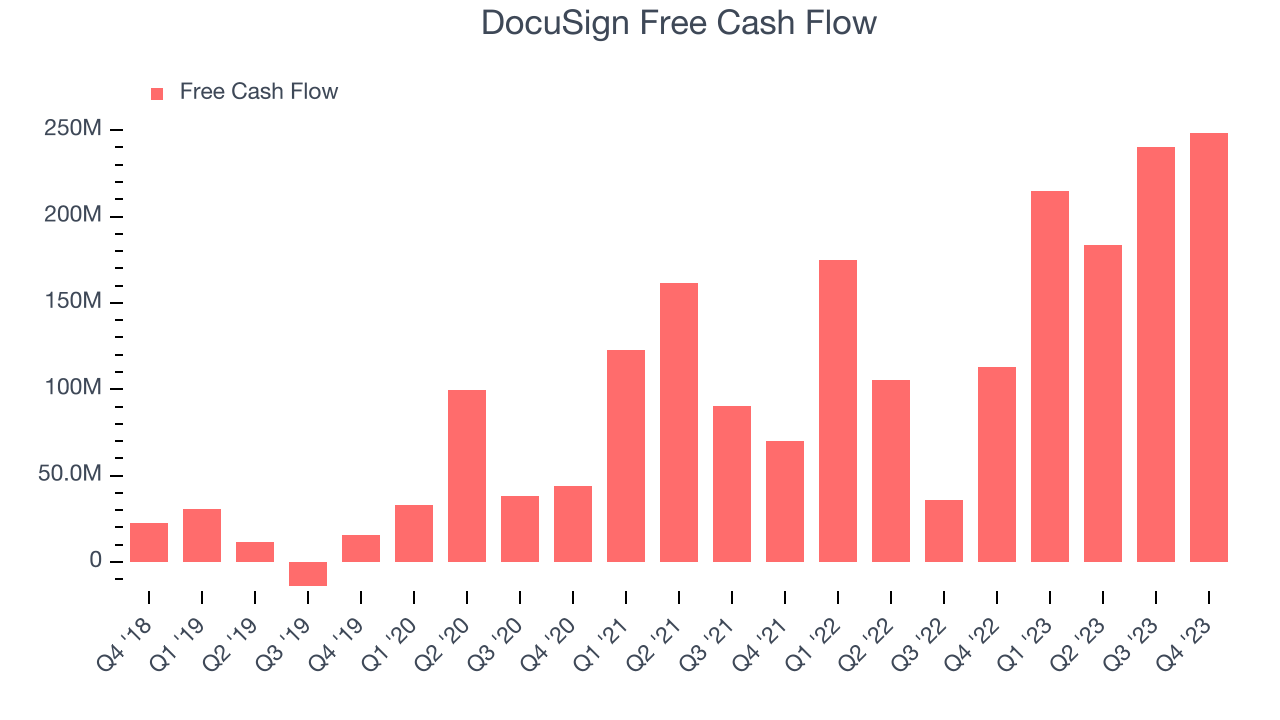

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. DocuSign's free cash flow came in at $248.6 million in Q4, up 120% year on year.

DocuSign has generated $887.1 million in free cash flow over the last 12 months, an eye-popping 32.1% of revenue. This robust FCF margin stems from its asset-lite business model, scale advantages, and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a healthy cash balance.

Key Takeaways from DocuSign's Q4 Results

DocuSign delivered impressive free cash flow in Q4 and revenue guidance slightly exceeded estimates. Even though guidance suggests a slowdown in growth this quarter's results seemed fairly positive. The stock is up 16.9% after reporting and currently trades at $62.65 per share.

Is Now The Time?

When considering an investment in DocuSign, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although DocuSign isn't a bad business, it probably wouldn't be one of our picks. Although its revenue growth has been steady, Wall Street expects growth to deteriorate from here.

DocuSign's price-to-sales ratio based on the next 12 months is 3.9x, suggesting that the market has lower expectations of the business, relative to the high growth tech stocks. We can find things to like about DocuSign and there's no doubt it's a bit of a market darling, at least for some. But we are wondering whether there might be better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $60.24 per share right before these results (compared to the current share price of $62.65), implying they didn't see much short-term potential in the DocuSign.

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.