Etsy's (NASDAQ:ETSY) Posts Q3 Sales In Line With Estimates But Stock Drops

Petr Huřťák /

November 1, 2023

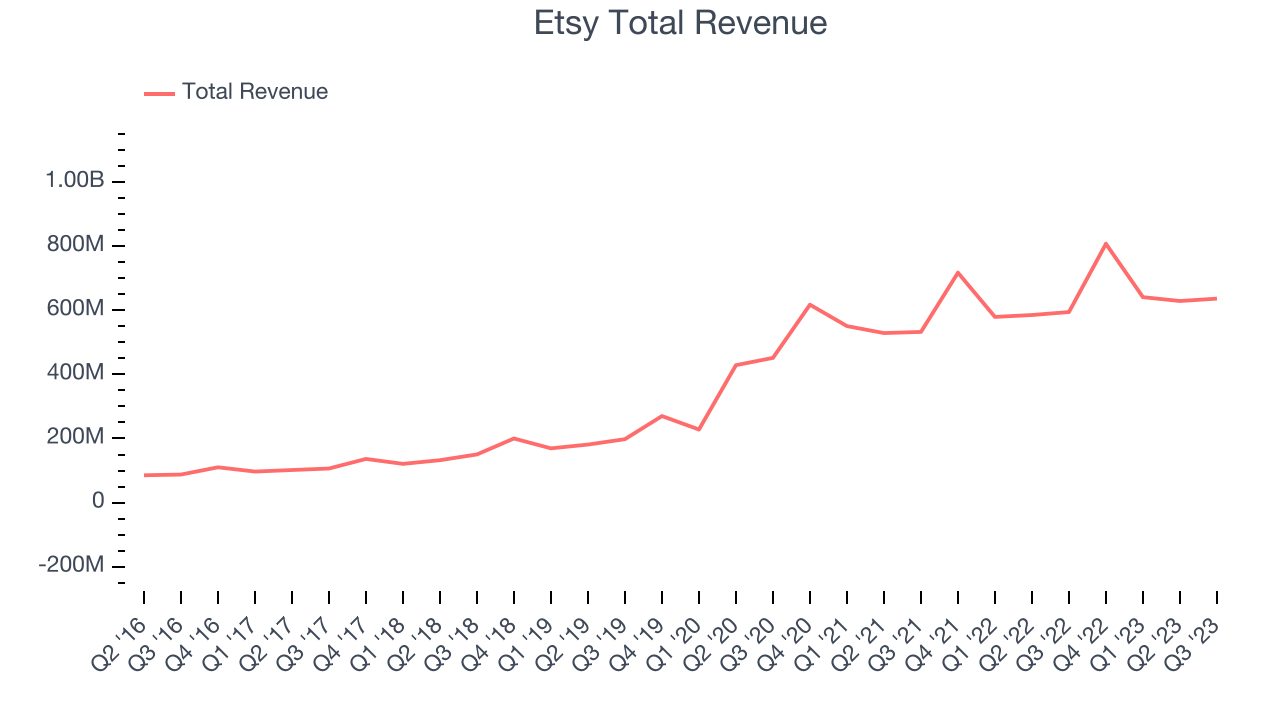

Online marketplace Etsy (NASDAQ:ETSY) reported results in line with analysts' expectations in Q3 FY2023, with revenue up 7.04% year on year to $636.3 million. Turning to EPS, Etsy made a GAAP profit of $0.64 per share, improving from its loss of $7.62 per share in the same quarter last year.

Is now the time to buy Etsy? Find out in our full research report.

Etsy (ETSY) Q3 FY2023 Highlights:

- Revenue: $636.3 million vs analyst estimates of $630.4 million (0.94% beat)

- EPS: $0.64 vs analyst estimates of $0.51 (26.5% beat)

- Free Cash Flow of $207.6 million, up 54.2% from the previous quarter

- Gross Margin (GAAP): 70.3%, in line with the same quarter last year

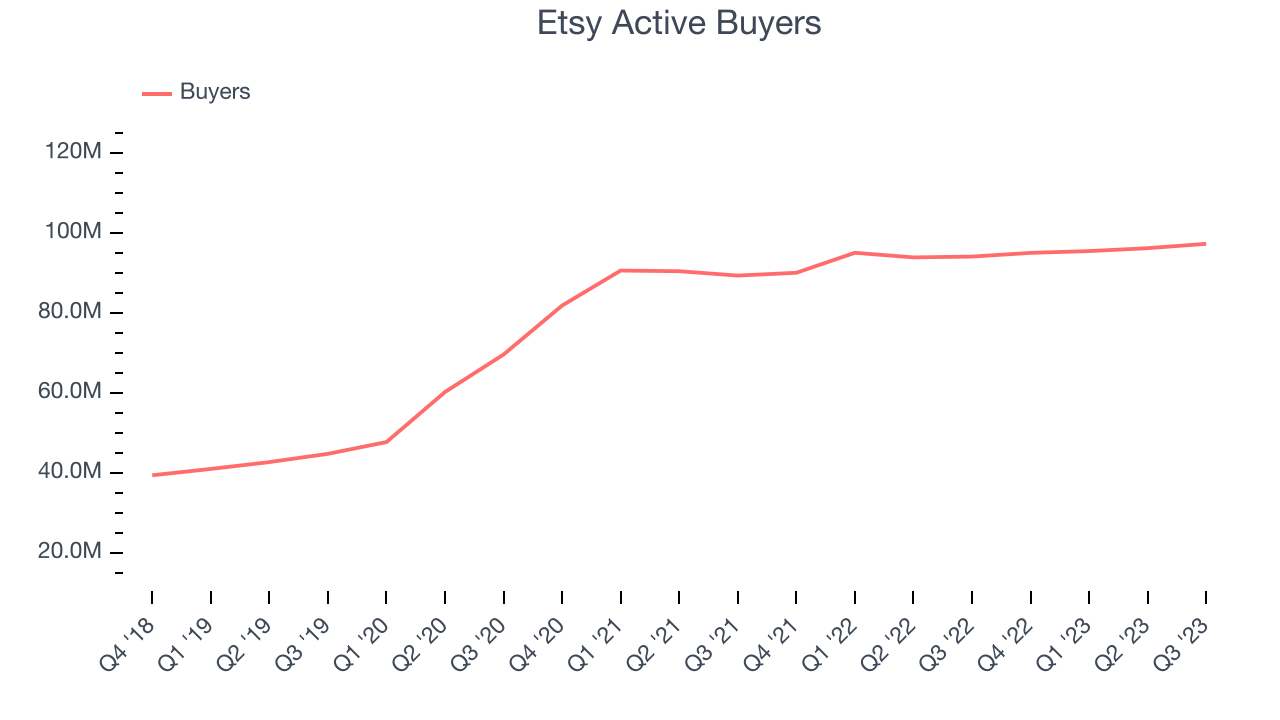

- Active Buyers: 97.3 million, up 3.19 million year on year

"Etsy's consolidated results were in line with expectations for modest top line growth and very strong profitability," said Josh Silverman, Etsy, Inc. Chief Executive Officer. "While we are undoubtedly operating in a challenging environment for spending on consumer discretionary items, we believe that we are at least holding our share gains in our top categories..."

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NASDAQ:ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Sales Growth

Etsy's revenue growth over the last three years has been very strong, averaging 32.7% annually. This quarter, Etsy reported mediocre 7.04% year-on-year revenue growth, in line with what analysts were expecting.

Ahead of the earnings results, analysts covering the company were projecting sales to grow 7.14% over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. See it here.

Usage Growth

As an online marketplace, Etsy generates revenue growth by increasing both the number of buyers on its platform and the average order size in dollars.

Over the last two years, Etsy's active buyers, a key performance metric for the company, grew 4.48% annually to 97.3 million. This growth lags behind the hottest consumer internet apps.

In Q3, Etsy added 3.19 million active buyers, translating into 3.39% year-on-year growth.

Key Takeaways from Etsy's Q3 Results

Sporting a market capitalization of $7.66 billion, Etsy is among smaller companies, but its more than $976.9 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

The major negative was the company guiding to Q4 GMS (gross merchandise sales) below expectations. Its revenue growth regrettably slowed. Overall, the results could have been better. The company is down 9.64% on the results and currently trades at $54.94 per share.

So should you invest in Etsy right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.