Electric vehicle charging company EVgo (NASDAQ:EVGO) reported Q3 CY2024 results beating Wall Street’s revenue expectations, with sales up 92.4% year on year to $67.54 million. The company expects the full year’s revenue to be around $257.5 million, close to analysts’ estimates. Its GAAP loss of $0.11 per share was also 4.3% above analysts’ consensus estimates.

Is now the time to buy EVgo? Find out by accessing our full research report, it’s free.

EVgo (EVGO) Q3 CY2024 Highlights:

- Revenue: $67.54 million vs analyst estimates of $65.97 million (2.4% beat)

- EPS (GAAP): -$0.11 vs analyst estimates of -$0.11 (beat by $0)

- EBITDA: -$8.88 million vs analyst estimates of -$11.14 million (20.3% beat)

- The company slightly lifted its revenue guidance for the full year to $257.5 million at the midpoint from $255 million

- EBITDA guidance for the full year is -$35 million at the midpoint, above analyst estimates of -$35.68 million

- Gross Margin (GAAP): 9.4%, down from 26.3% in the same quarter last year

- Operating Margin: -47.1%, up from -104% in the same quarter last year

- EBITDA Margin: -13.2%, up from -40.6% in the same quarter last year

- Free Cash Flow was -$13.73 million compared to -$31.28 million in the same quarter last year

- Market Capitalization: $576.9 million

“I’m pleased to report another record quarter anchored by strong revenues and triple digit year-over-year network throughput growth,” said Badar Khan, EVgo’s CEO.

Company Overview

Created through a settlement between NRG Energy and the California Public Utilities Commission, EVgo (NASDAQ:EVGO) is a provider of electric vehicle charging solutions, operating fast charging stations across the United States.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

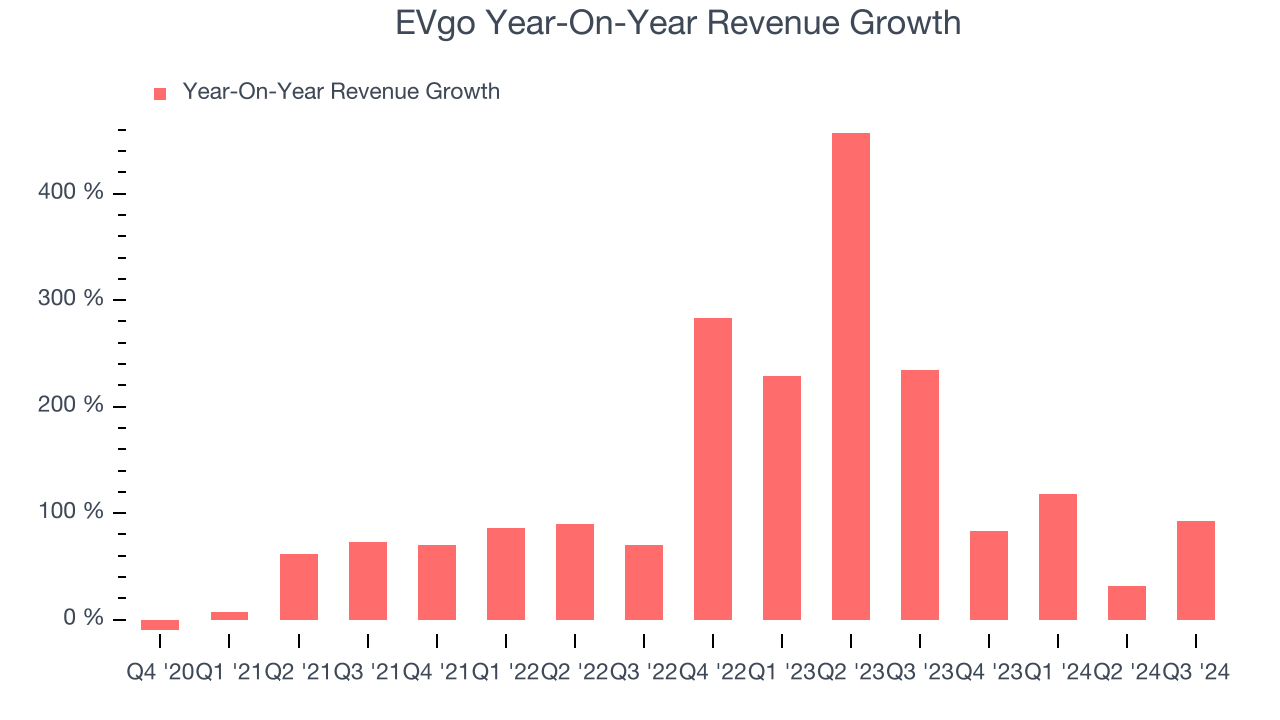

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, EVgo’s 99.8% annualized revenue growth over the last four years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. EVgo’s annualized revenue growth of 164% over the last two years is above its four-year trend, suggesting its demand was strong and recently accelerated.

This quarter, EVgo reported magnificent year-on-year revenue growth of 92.4%, and its $67.54 million of revenue beat Wall Street’s estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 33.6% over the next 12 months, a deceleration versus the last two years. This projection is still noteworthy and suggests the market is baking in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

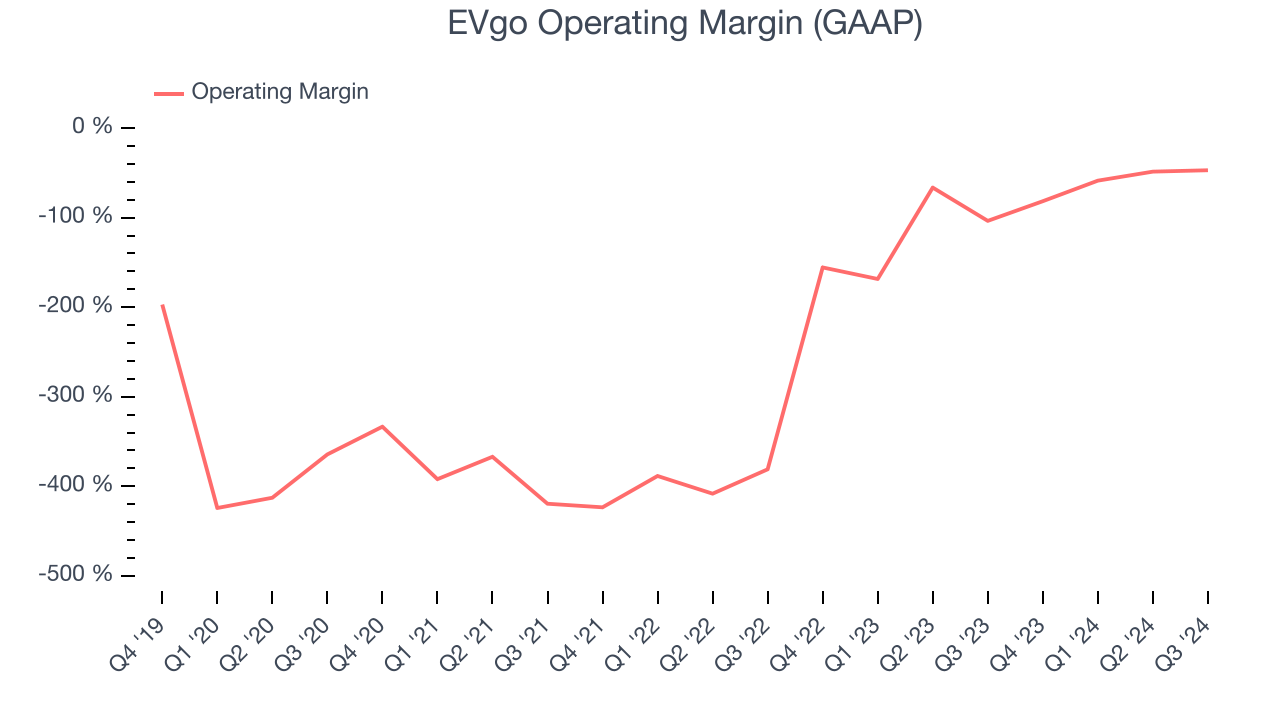

Operating Margin

EVgo’s high expenses have contributed to an average operating margin of negative 124% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, EVgo’s annual operating margin rose over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q3, EVgo generated a negative 47.1% operating margin.

Earnings Per Share

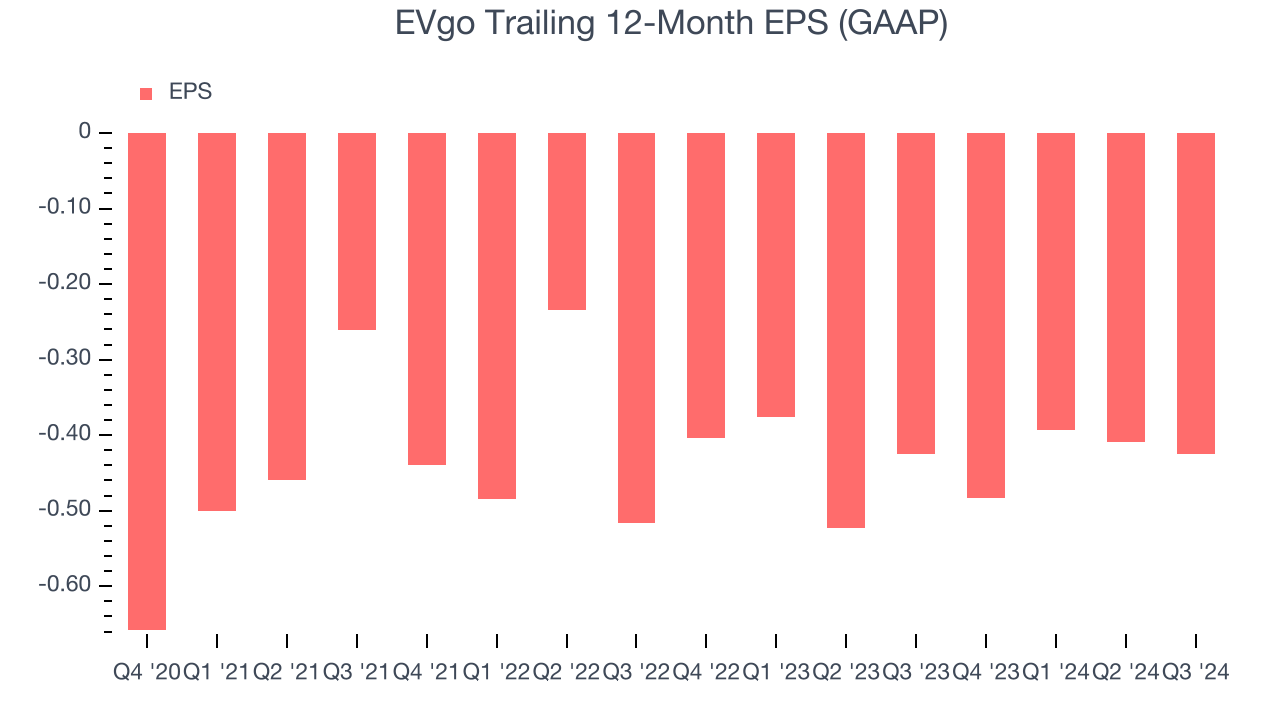

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Although EVgo’s full-year earnings are still negative, it reduced its losses and improved its EPS by 17.7% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For EVgo, its two-year annual EPS growth of 9.3% was lower than its four-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.In Q3, EVgo reported EPS at negative $0.11, down from negative $0.09 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.3%. Over the next 12 months, Wall Street is optimistic. Analysts forecast EVgo’s full-year EPS of negative $0.42 will reach break even.

Key Takeaways from EVgo’s Q3 Results

We liked that EVgo beat analysts’ revenue and EBITDA expectations this quarter. We were also excited its guidance outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 9.4% to $5.90 immediately after reporting.

Sure, EVgo had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.