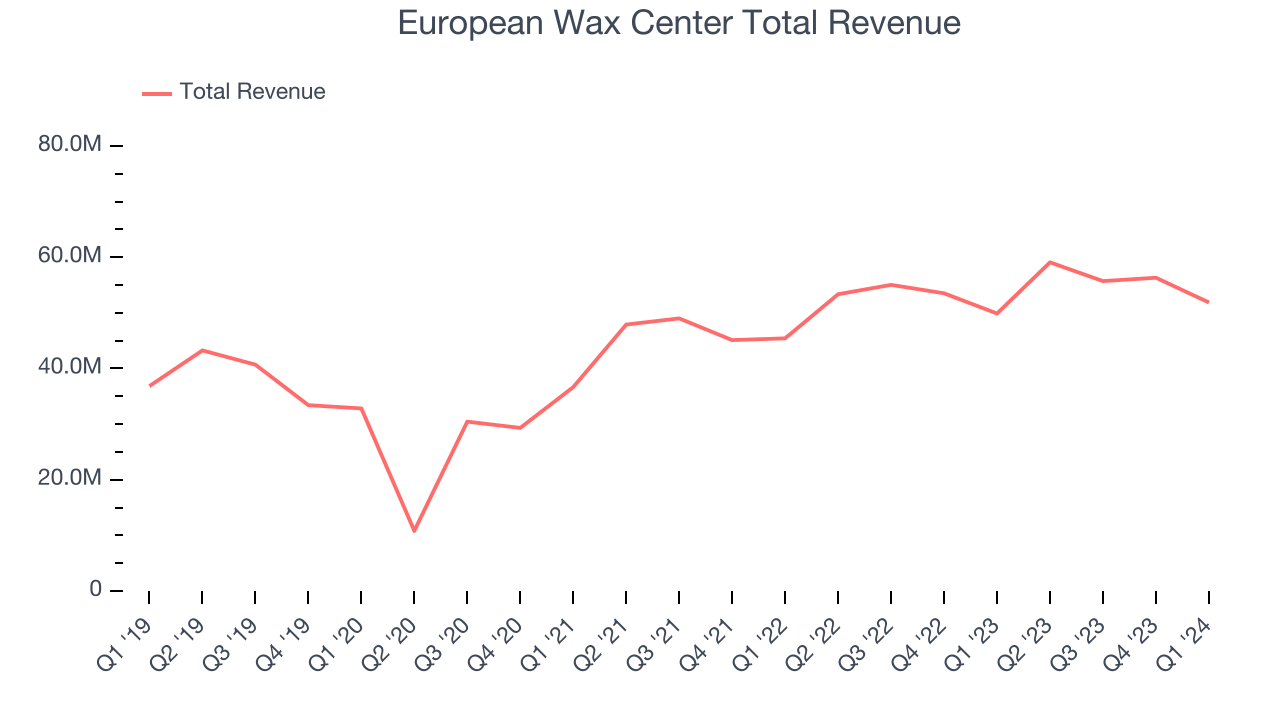

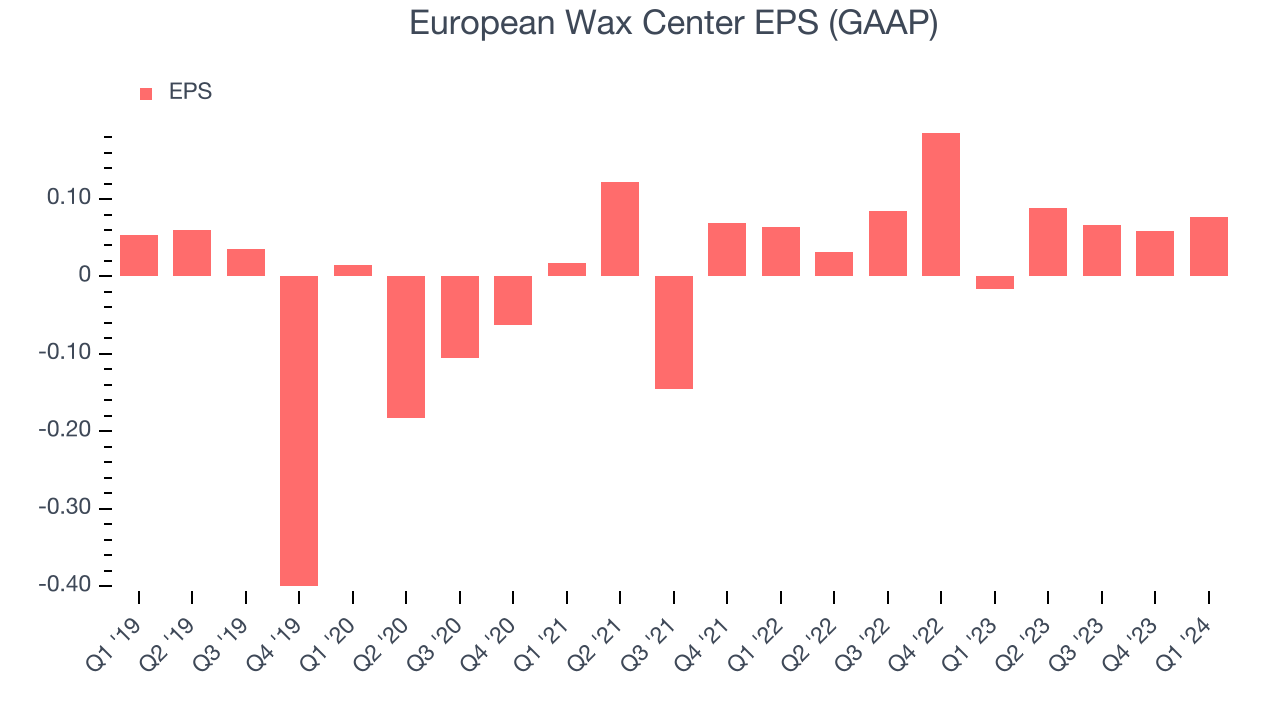

Beauty and waxing service franchise European Wax Center (NASDAQ:EWCZ) reported results in line with analysts' expectations in Q1 CY2024, with revenue up 4% year on year to $51.87 million. On the other hand, the company's full-year revenue guidance of $228.5 million at the midpoint came in slightly below analysts' estimates. It made a GAAP profit of $0.08 per share, improving from its loss of $0.02 per share in the same quarter last year.

European Wax Center (EWCZ) Q1 CY2024 Highlights:

- Revenue: $51.87 million vs analyst estimates of $52.02 million (small miss)

- Adjusted EBITDA: $17.5 million vs analyst estimates of $16.6 million (5.4% beat)

- EPS: $0.08 vs analyst estimates of $0.03 ($0.05 beat)

- The company reconfirmed its revenue guidance for the full year of $228.5 million at the midpoint (slight miss, adjusted EBITDA guidance for the full year roughly in line)

- Gross Margin (GAAP): 73.9%, up from 71% in the same quarter last year

- Free Cash Flow of $10.69 million, down 36.1% from the previous quarter

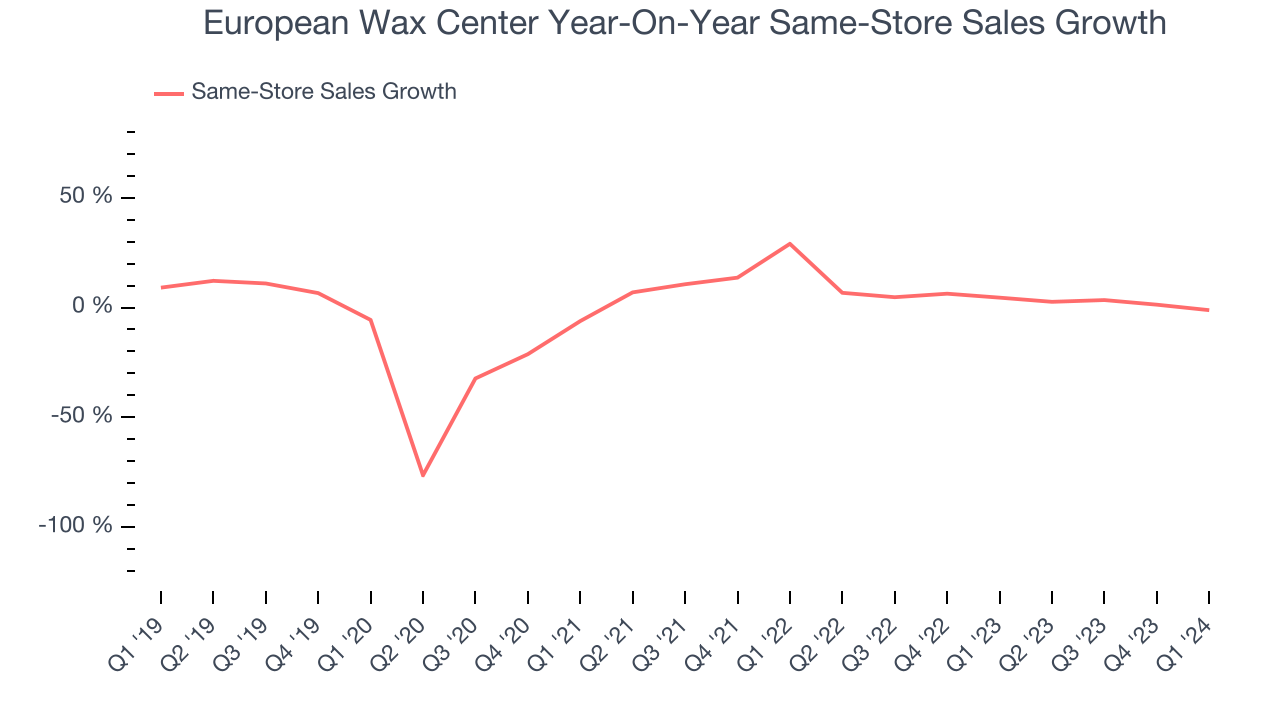

- Same-Store Sales were down 1.2% year on year (miss)

- Market Capitalization: $529.8 million

Founded by two siblings, European Wax Center (NASDAQ:EWCZ) is a beauty and waxing salon chain specializing in professional wax services and skincare products.

European Wax Center recognized the need for a waxing experience focused on comfort and hygiene. The company aimed to provide a luxurious experience, prioritizing customer care and high-quality products. It began with a single salon and has since expanded into a prominent chain.

The company offers a wide range of waxing services for both men and women, including facial and body waxing. European Wax Center's appeal is in its proprietary Comfort Wax, made from natural beeswax. The popularity of Comfort Wax has incentivized the company to market other skincare products that complement its core services.

Revenue is generated through a combination of service fees and product sales. Its business model includes franchise and corporate-owned locations, allowing for scalability and flexibility in expansion. European Wax Center's revenue model is further bolstered by royalty fees from franchisees, which typically come with higher margins.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from "things" to "experiences". Leisure facilities seek to benefit but must innovate to do so because of the industry's high competition and capital intensity.

As a niche business, European Wax Center has no direct public competitors. Privately owned competitors include Bluemercury, Radiant Waxing, and Waxing the City.Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. European Wax Center's annualized revenue growth rate of 10.4% over the last four years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. European Wax Center's recent history shows the business has slowed as its annualized revenue growth of 9.1% over the last two years is below its four-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. European Wax Center's recent history shows the business has slowed as its annualized revenue growth of 9.1% over the last two years is below its four-year trend.

We can dig even further into the company's revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, European Wax Center's same-store sales averaged 3.5% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company's top-line performance.

This quarter, European Wax Center grew its revenue by 4% year on year, and its $51.87 million of revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 5.4% over the next 12 months, an acceleration from this quarter.

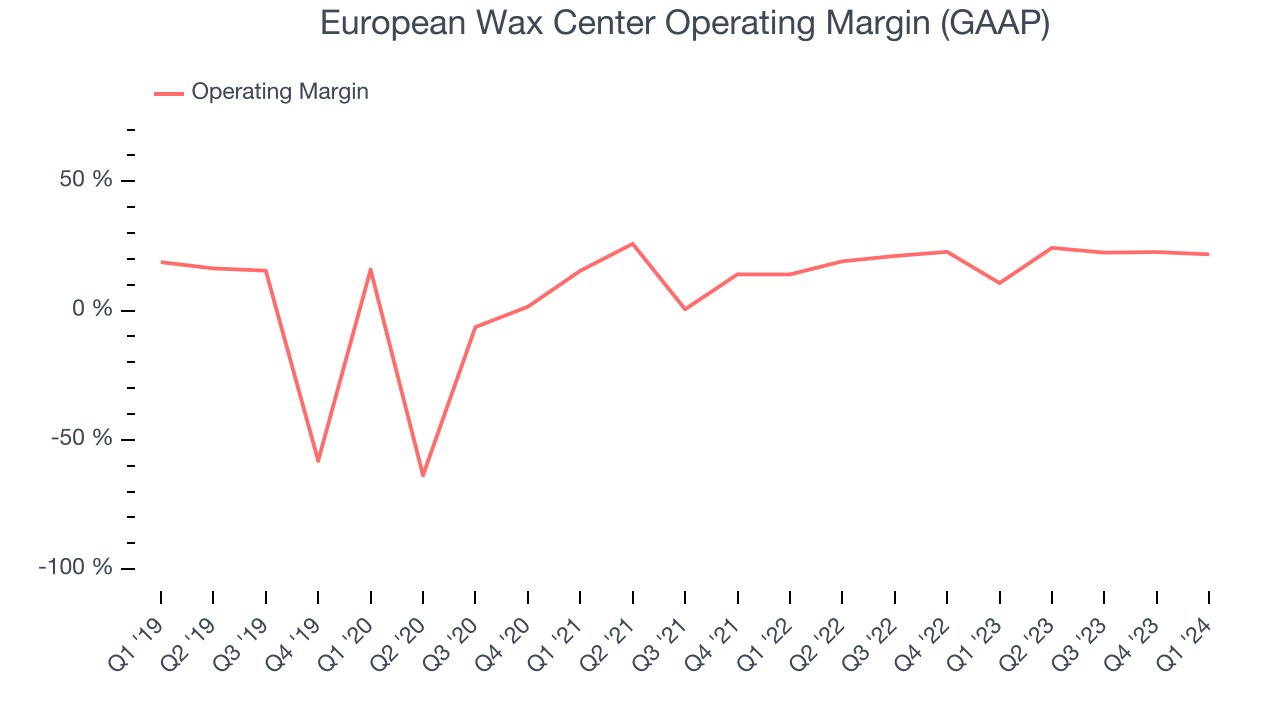

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

European Wax Center has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 20.7%.

In Q1, European Wax Center generated an operating profit margin of 21.7%, up 11.1 percentage points year on year.

Over the next 12 months, Wall Street expects European Wax Center to maintain its LTM operating margin of 22.8%.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last four years, European Wax Center cut its earnings losses and improved its EPS by 31.6% each year. This performance is materially higher than its 10.4% annualized revenue growth over the same period. Let's dig into why.

European Wax Center's operating margin has expanded 6 percentage points over the last four years while its share count has shrunk 23.7%. Improving profitability and share buybacks are positive signs as they juice EPS growth relative to revenue growth.In Q1, European Wax Center reported EPS at $0.08, up from negative $0.02 in the same quarter last year. This print easily cleared analysts' estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects European Wax Center to perform poorly. Analysts are projecting its LTM EPS of $0.29 to shrink to break even.

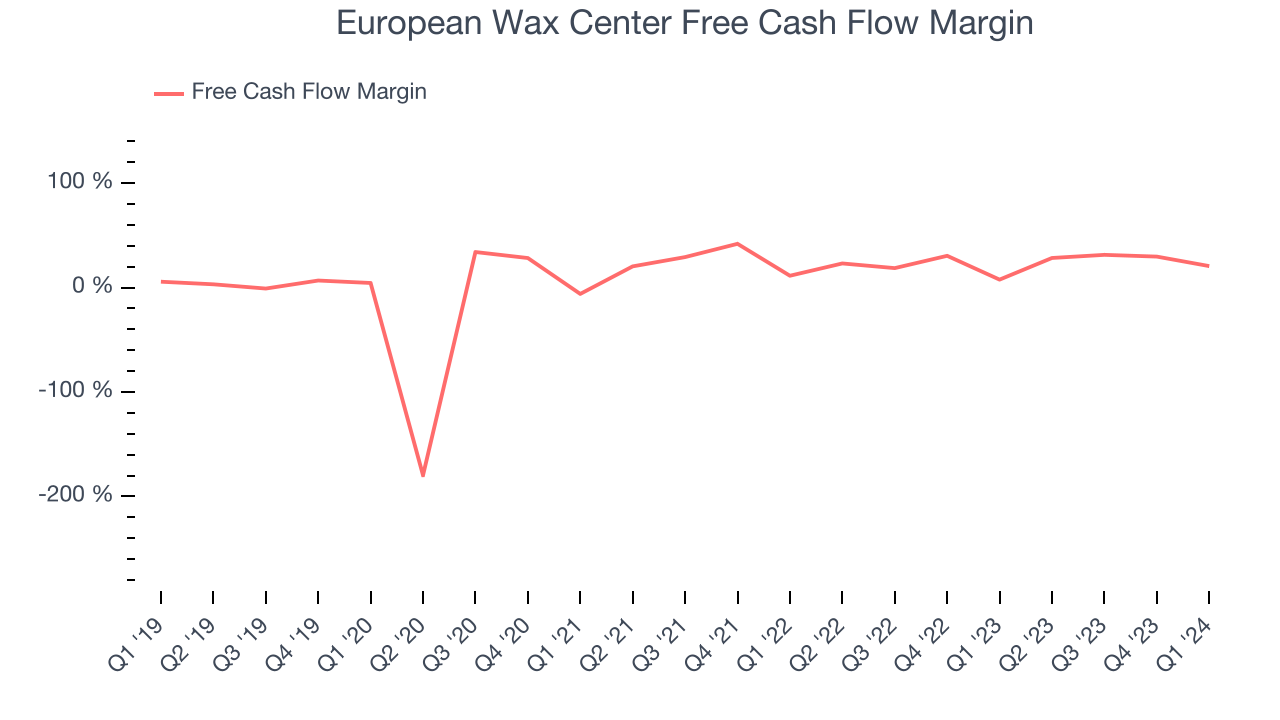

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, European Wax Center has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining a robust cash balance. The company's free cash flow margin has been among the best in the consumer discretionary sector, averaging 24%.

European Wax Center's free cash flow came in at $10.69 million in Q1, equivalent to a 20.6% margin and up 180% year on year.

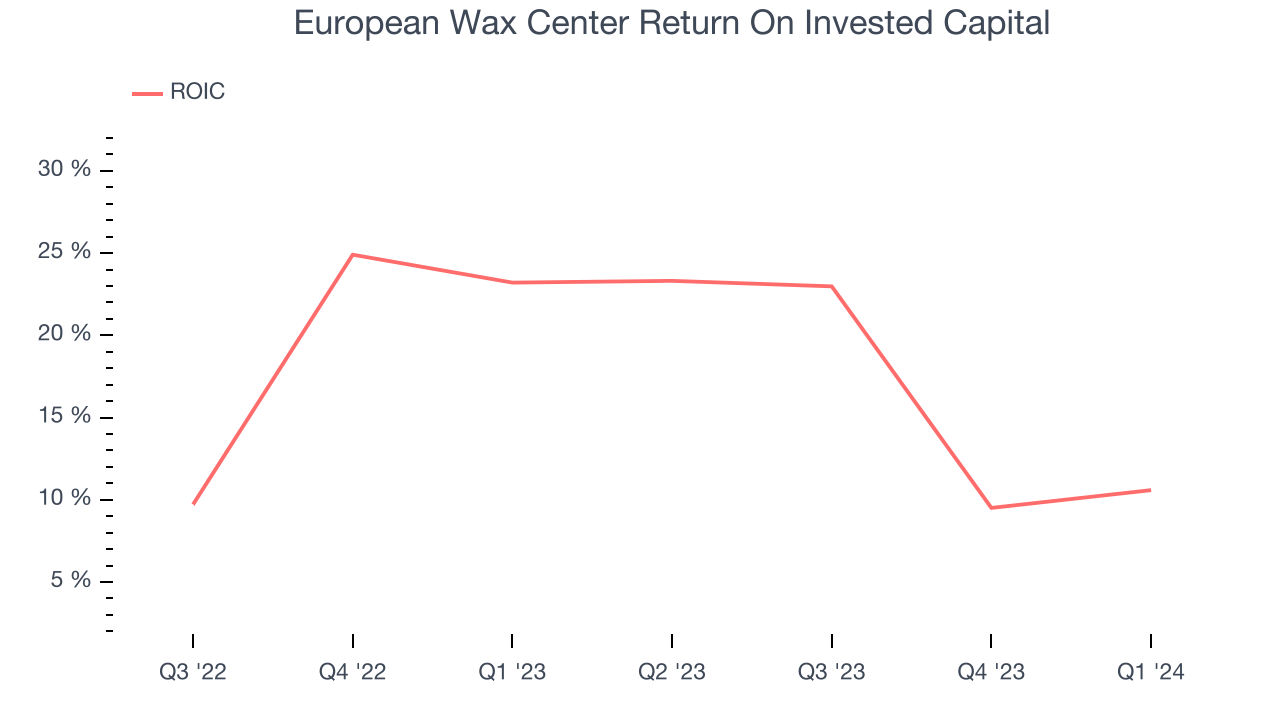

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

European Wax Center's five-year average return on invested capital was 16.9%, slightly better than the broader sector. Just as you’d like your investment dollars to generate returns, European Wax Center's invested capital has produced decent profits.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

European Wax Center reported $60.36 million of cash and $380.8 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $77.22 million of EBITDA over the last 12 months, we view European Wax Center's 4.1x net-debt-to-EBITDA ratio as safe. We also see its $13.49 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from European Wax Center's Q1 Results

We were impressed that European Wax Center beat analysts' adjusted EBITDA and EPS expectations this quarter. On the other hand, same-store sales in the quarter underwhelmed and the company's and its full-year revenue guidance slightly fell short of Wall Street's estimates, although full year adjusted EBITDA guidance was roughly in line. Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is flat after reporting and currently trades at $10.8 per share.

Is Now The Time?

European Wax Center may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

European Wax Center isn't a bad business, but it probably wouldn't be one of our picks. Its revenue growth has been a little slower over the last four years, and analysts expect growth to deteriorate from here. And while its EPS growth over the last four years has been fantastic, unfortunately, its same-store sales performance has been disappointing.

European Wax Center's price-to-earnings ratio based on the next 12 months is 26.7x. We don't really see a big opportunity in the stock at the moment, but in the end, beauty is in the eye of the beholder. If you like European Wax Center, it seems to be trading at a reasonable price.

Wall Street analysts covering the company had a one-year price target of $18 per share right before these results (compared to the current share price of $10.80).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.