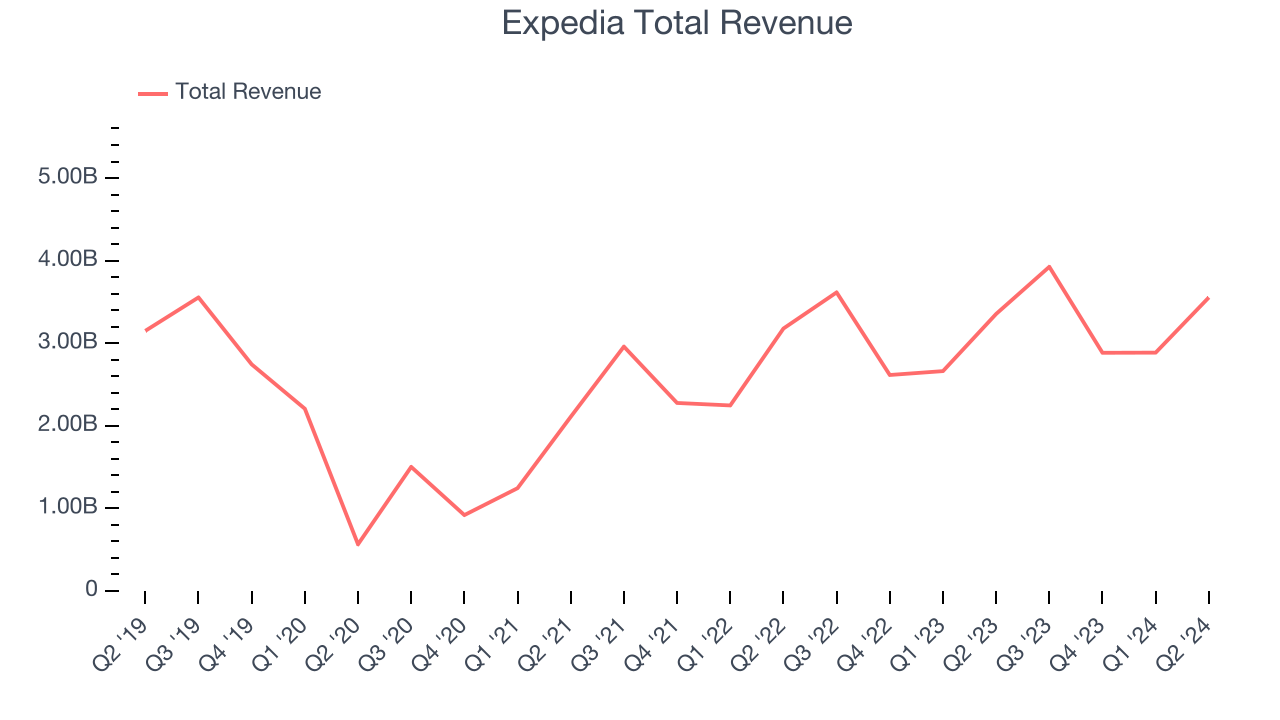

Online travel agency Expedia (NASDAQ:EXPE) reported results in line with analysts' expectations in Q2 CY2024, with revenue up 6% year on year to $3.56 billion. It made a non-GAAP profit of $3.51 per share, improving from its profit of $2.54 per share in the same quarter last year.

Is now the time to buy Expedia? Find out by accessing our full research report, it's free.

Expedia (EXPE) Q2 CY2024 Highlights:

- Revenue: $3.56 billion vs analyst estimates of $3.53 billion (small beat)

- Adjusted EBITDA: $786 million vs analyst estimates of $749 million (4.9% beat)

- EPS (non-GAAP): $3.51 vs analyst estimates of $3.16 (10.9% beat)

- Gross Margin (GAAP): 89.8%, up from 87.9% in the same quarter last year

- EBITDA Margin: 22.1%, in line with the same quarter last year

- Free Cash Flow of $1.31 billion, down 51.6% from the previous quarter

- Room Nights Booked: 98.9 million, up 9.2 million year on year

- Market Capitalization: $15 billion

“Our second quarter results came in at the high end of our expectations, with gross bookings and revenue growing 6%. We're pleased with our momentum and the sequential improvement in our consumer brands. However, in July, we have seen a more challenging macro environment and a softening in travel demand. We are therefore adjusting our expectations for the rest of the year,” said Ariane Gorin, CEO of Expedia Group.

Originally founded as a part of Microsoft, Expedia (NASDAQ:EXPE) is one of the world’s leading online travel agencies.

Online Travel

Because of the enormous number of flights, hotels, and accommodations available, travel is a natural fit for marketplaces that aggregate suppliers, simplifying the shopping process for consumers. Online travel platforms today make up over 50% of the industry’s bookings, a percentage that has been rising for 20 years, and will likely continue in the years ahead.

Sales Growth

Expedia's revenue growth over the last three years has been very strong, averaging 39.2% annually. This quarter, Expedia reported mediocre 6% year-on-year revenue growth, in line with analysts' expectations.

Ahead of the earnings results, analysts were projecting sales to grow 7.5% over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Usage Growth

As an online travel company, Expedia generates revenue growth by increasing both the number of stays (or experiences) booked and the commission charged on those bookings.

Over the last two years, Expedia's nights booked, a key performance metric for the company, grew 13.9% annually to 98.9 million. This is solid growth for a consumer internet company.

In Q2, Expedia added 9.2 million nights booked, translating into 10.3% year-on-year growth.

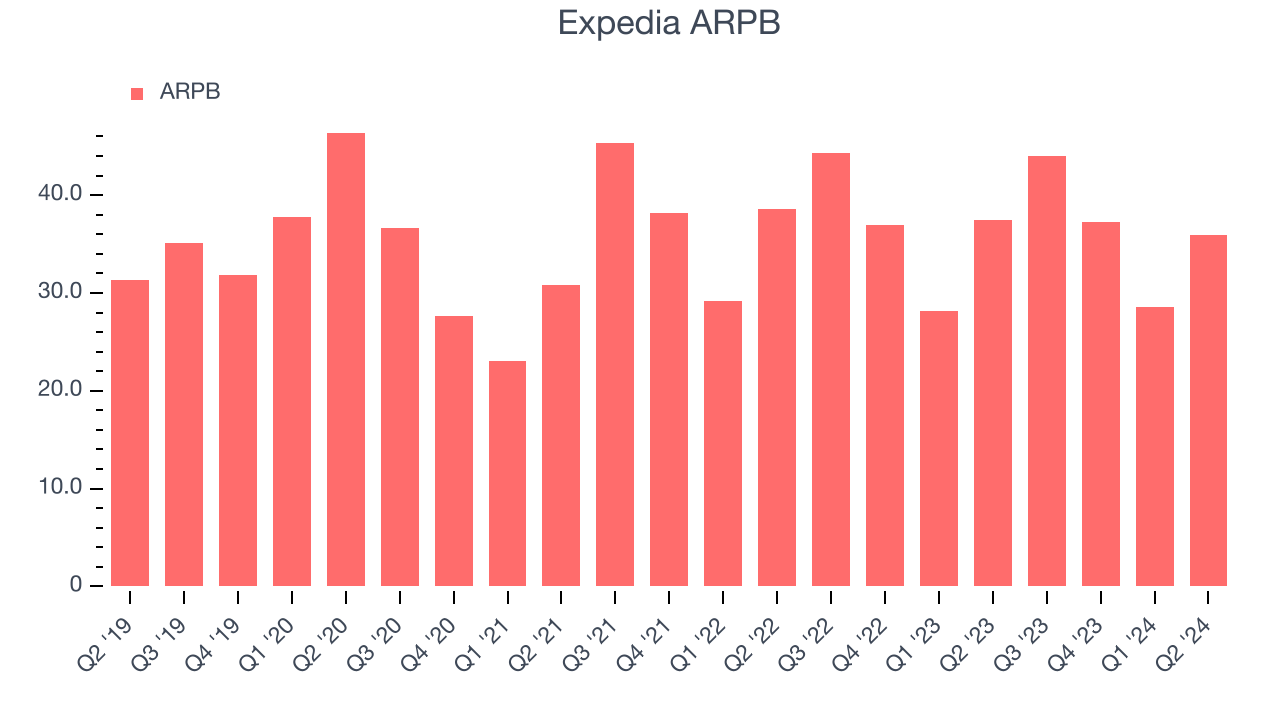

Revenue Per Booking

Average revenue per booking (ARPB) is a critical metric to track for consumer internet businesses like Expedia because it not only measures how much users book on its platform but also the commission that Expedia can charge.

Expedia's ARPB has declined over the last two years, averaging 1.8%. Although the company's bookings have continued to grow, it's lost its pricing power and will have to make improvements soon. This quarter, ARPB declined 3.9% year on year to $35.98 per booking.

Key Takeaways from Expedia's Q2 Results

It was good to see Expedia beat analysts' booking expectations this quarter. We were also glad it expanded its number of bookings. The company also beat on adjusted EBITDA. On the other hand, its revenue growth regrettably slowed. Zooming out, we think this was a mixed quarter. The areas below expectations seem to be driving the stock move, and the stock traded down 2.2% to $115.38 immediately after reporting.

So should you invest in Expedia right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.