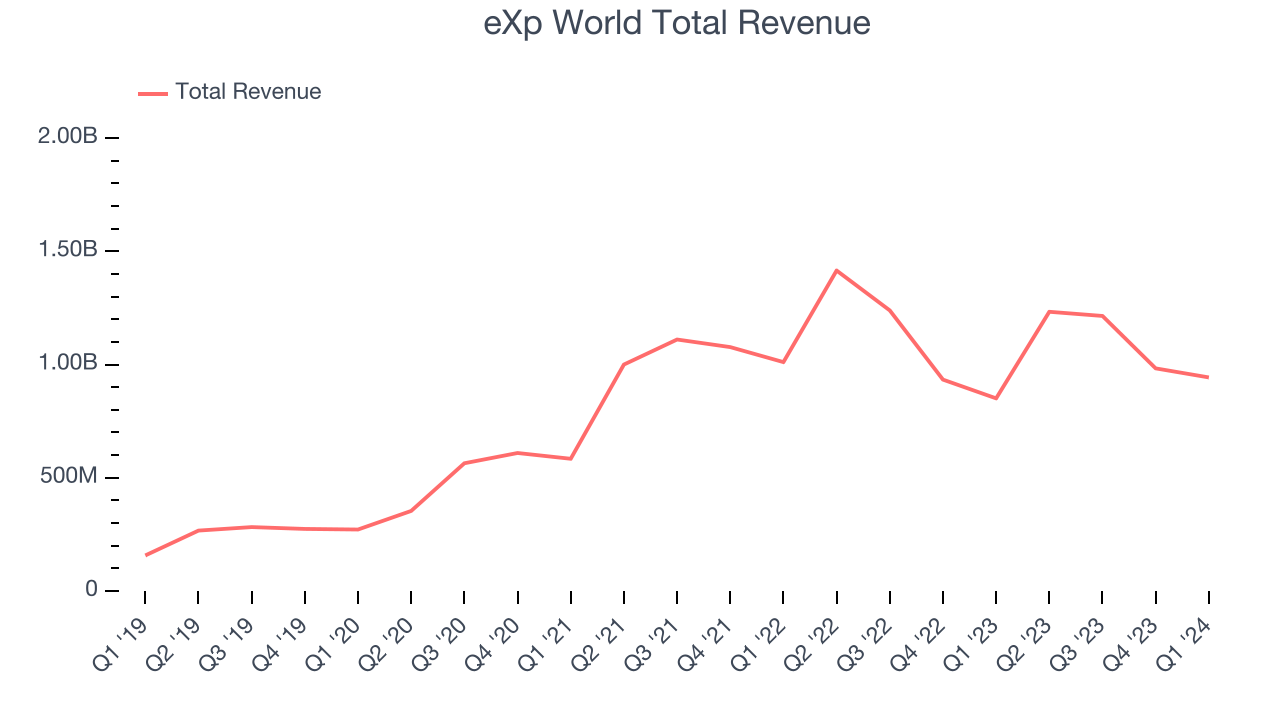

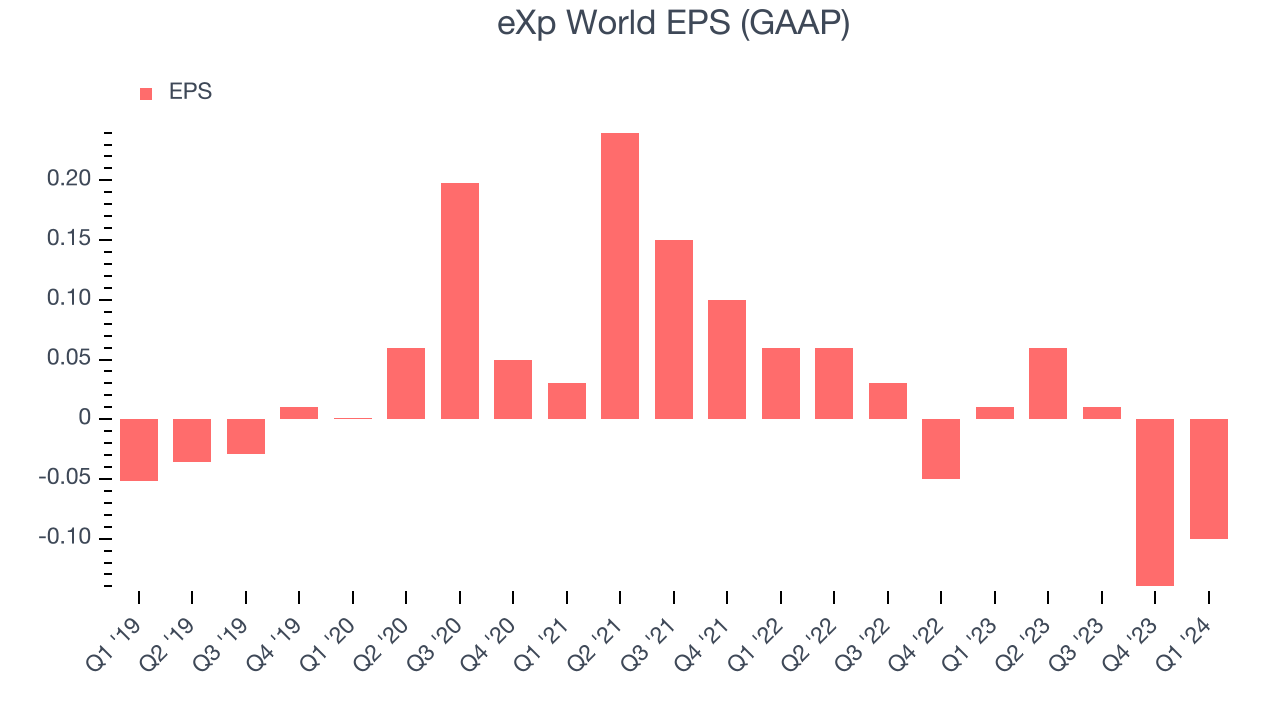

Real estate technology company eXp World (NASDAQ:EXPI) reported Q1 CY2024 results topping analysts' expectations, with revenue up 10.9% year on year to $943.1 million. It made a GAAP loss of $0.10 per share, down from its profit of $0.01 per share in the same quarter last year.

eXp World (EXPI) Q1 CY2024 Highlights:

- Revenue: $943.1 million vs analyst estimates of $893.2 million (5.6% beat)

- Adjusted EBITDA: $11.0 million vs analyst estimates of $6.5 million ($4.5 million beat)

- EPS: -$0.10 vs analyst estimates of -$0.06 (-$0.04 miss)

- Gross Margin (GAAP): 8.3%, down from 8.6% in the same quarter last year

- Free Cash Flow of $59.33 million, up 88.7% from the previous quarter

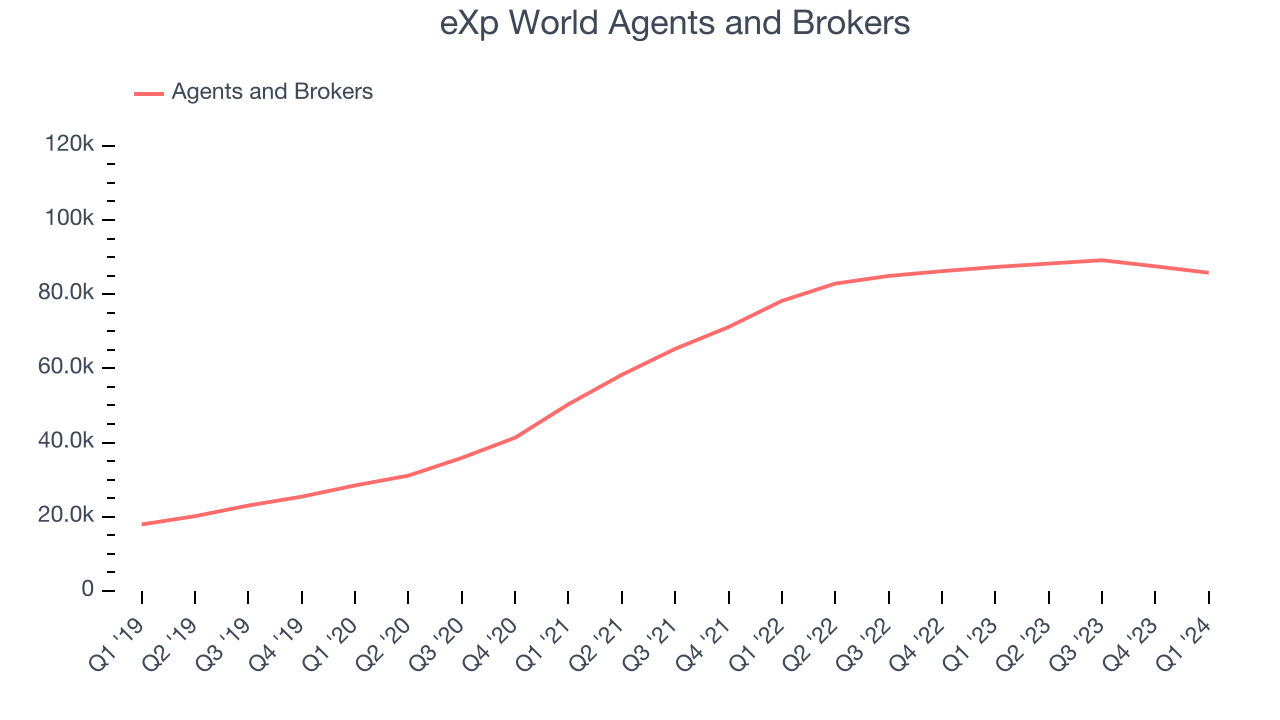

- Agents and Brokers: 85,780

- Market Capitalization: $1.51 billion

Founded in 2009, eXp World (NASDAQ:EXPI) is a real estate company known for its virtual, cloud-based approach to real estate brokerage.

At the core of eXp World's business model is eXp Realty, a full-service real estate brokerage. eXp Realty offers agents and brokers an array of tools and services that include lead generation, training, and an online collaborative platform. This model supports a remote and flexible working environment, attracting a growing network of real estate professionals worldwide.

Another significant aspect of eXp World is its agent ownership model. The company offers a unique financial model for its agents and brokers, including revenue sharing and an opportunity to earn equity awards for contributing to the growth of the company.

In addition to real estate brokerage services, eXp World also operates Virbela, a technology company that develops virtual world solutions for remote work, education, and events.

Real Estate Services

Technology has been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

eXp World's primary competitors include Realogy Holdings (NYSE:RLGY), Zillow (NASDAQ:ZG), Redfin (NASDAQ:RDFN), and Compass (NYSE:COMP).Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. eXp World's annualized revenue growth rate of 49% over the last five years was incredible for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. eXp World's recent history shows its momentum has slowed as its annualized revenue growth of 2.1% over the last two years is below its five-year trend.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. eXp World's recent history shows its momentum has slowed as its annualized revenue growth of 2.1% over the last two years is below its five-year trend.

We can better understand the company's revenue dynamics by analyzing its number of agents and brokers, which reached 85,780 in the latest quarter. Over the last two years, eXp World's agents and brokers averaged 14.6% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company's monetization of its consumers has fallen.

This quarter, eXp World reported robust year-on-year revenue growth of 10.9%, and its $943.1 million of revenue exceeded Wall Street's estimates by 5.6%. Looking ahead, Wall Street expects sales to grow 4.7% over the next 12 months, a deceleration from this quarter.

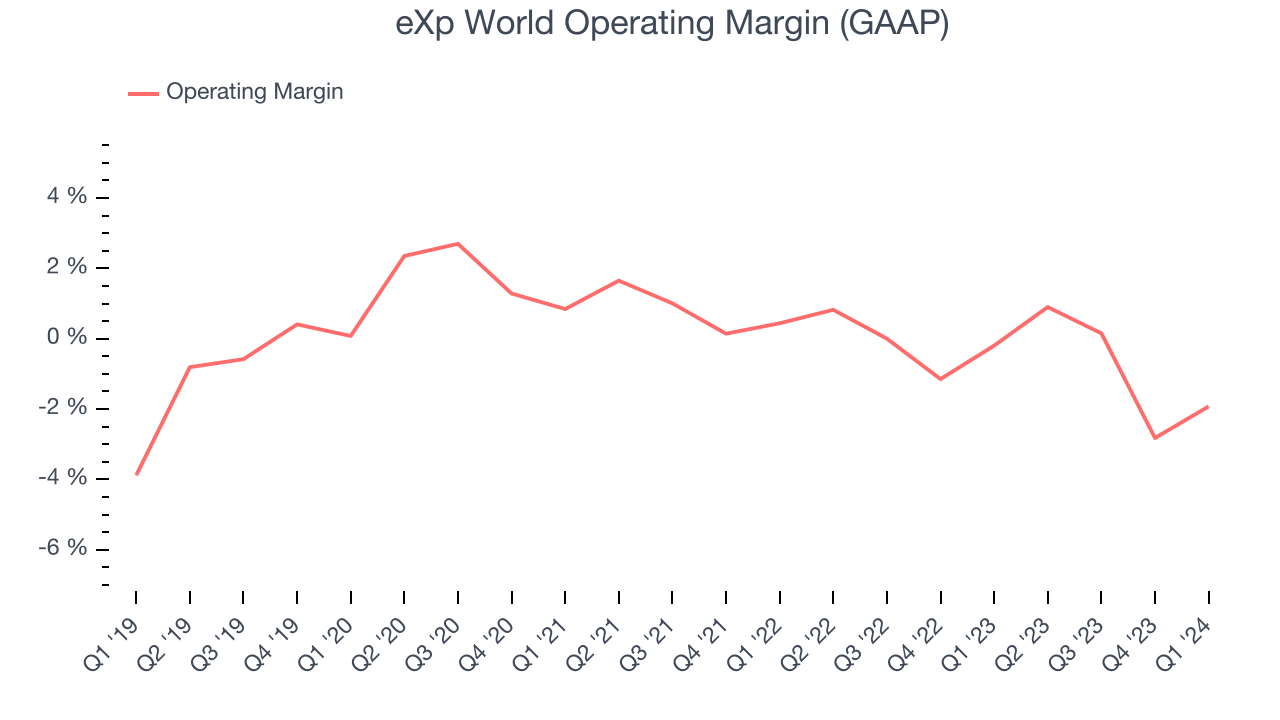

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

eXp World was roughly breakeven when averaging the last two years of quarterly operating profits, weak for a consumer discretionary business.

This quarter, eXp World generated an operating profit margin of negative 1.9%, down 1.7 percentage points year on year.

Over the next 12 months, Wall Street expects eXp World to maintain its LTM operating margin of negative 0.8%. We hope things change so the business can be profitable over the long term.EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability and efficiency of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Over the last five years, eXp World cut its earnings losses and improved its EPS by 7.8% each year. Furthermore, this performance is worse than its 49% annualized revenue growth over the same period. Let's dig into why.

A five-year view shows eXp World has diluted its shareholders, growing its share count by 27.4%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS growth, but they don't tell us as much about a company's fundamentals.In Q1, eXp World reported EPS at negative $0.10, down from $0.01 in the same quarter last year. This print unfortunately missed analysts' estimates. Over the next 12 months, Wall Street is optimistic. Analysts are projecting eXp World's LTM EPS of negative $0.17 to reach break even.

Cash Is King

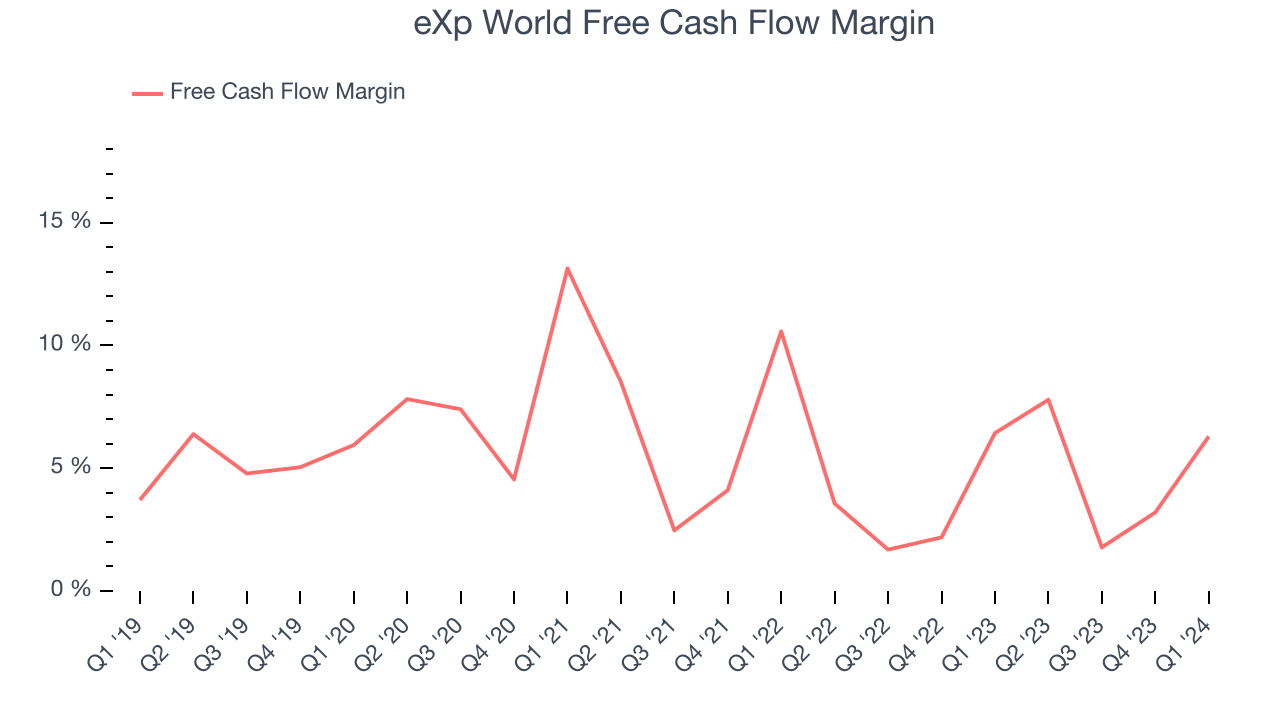

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, eXp World has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 4%, subpar for a consumer discretionary business.

eXp World's free cash flow came in at $59.33 million in Q1, equivalent to a 6.3% margin and up 8.4% year on year.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

eXp World's five-year average return on invested capital was negative 32.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

eXp World is a well-capitalized company with $109.2 million of cash and $7,000 of debt, meaning it could pay back all its debt tomorrow and still have $109.2 million of cash on its balance sheet. This net cash position gives eXp World the freedom to raise more debt, return capital to shareholders, or invest in growth initiatives.

Key Takeaways from eXp World's Q1 Results

We enjoyed seeing eXp World exceed analysts' revenue and adjusted EBITDA expectations this quarter. Overall, this was a solid quarter for eXp World. The stock is flat after reporting and currently trades at $10.15 per share.

Is Now The Time?

eXp World may have had a tough quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of eXp World, we'll be cheering from the sidelines. Although its revenue growth has been exceptional over the last five years, its relatively low ROIC suggests it has historically struggled to find compelling business opportunities. And while its projected EPS for the next year implies the company's fundamentals will improve, the downside is its operating margins reveal poor profitability compared to other consumer discretionary companies.

eXp World's price-to-earnings ratio based on the next 12 months is 39.0x. While we've no doubt one can find things to like about eXp World, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $12.25 per share right before these results (compared to the current share price of $10.15).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.