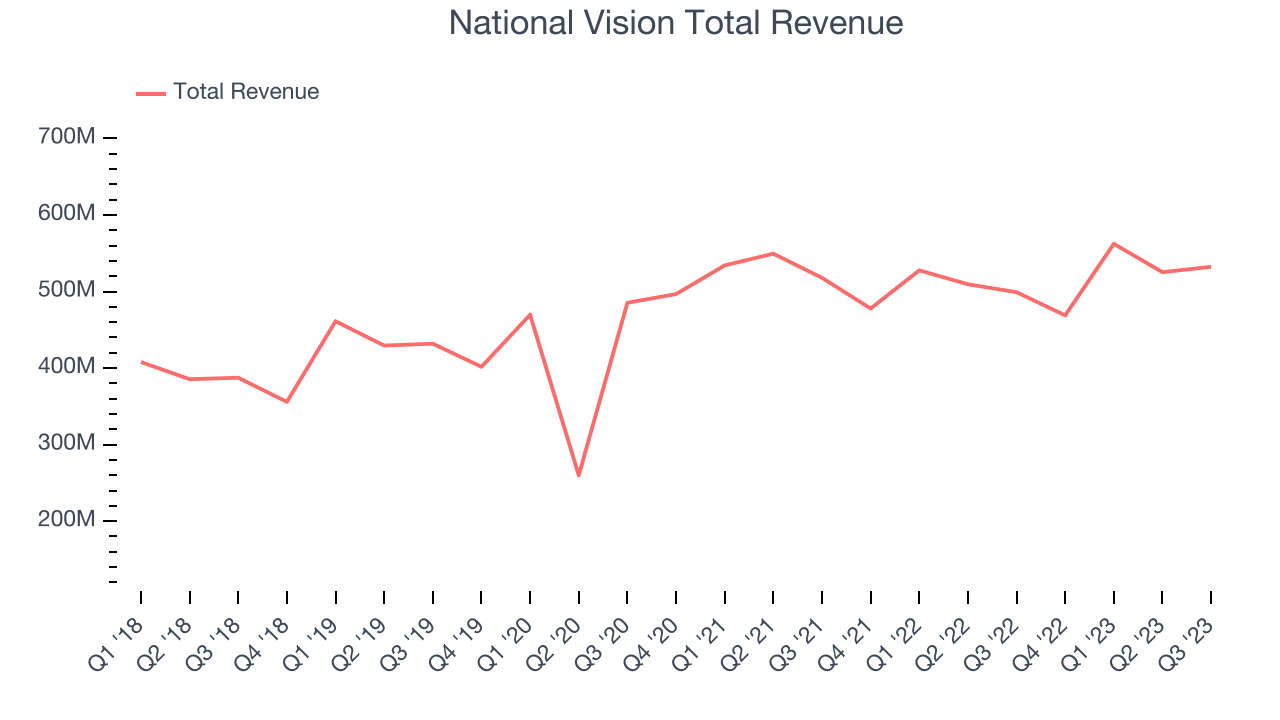

Optical retailer National Vision (NYSE:EYE) reported Q3 FY2023 results beating Wall Street analysts' expectations, with revenue up 6.6% year on year to $532.4 million. Its full-year revenue guidance of $2.12 billion at the midpoint came in slightly above analysts' estimates. Turning to EPS, National Vision's non-GAAP profit of $0.15 per share was flat year on year.

Is now the time to buy National Vision? Find out by accessing our full research report, it's free.

National Vision (EYE) Q3 FY2023 Highlights:

- Revenue: $532.4 million vs analyst estimates of $526.7 million (1.1% beat)

- EPS (non-GAAP): $0.15 vs analyst estimates of $0.10 (49.1% beat)

- The company reconfirmed its revenue guidance for the full year of $2.12 billion at the midpoint (raised full year EPS guidance)

- Free Cash Flow of $13.21 million, up from $2.9 million in the same quarter last year

- Gross Margin (GAAP): 52.7%, down from 53.4% in the same quarter last year

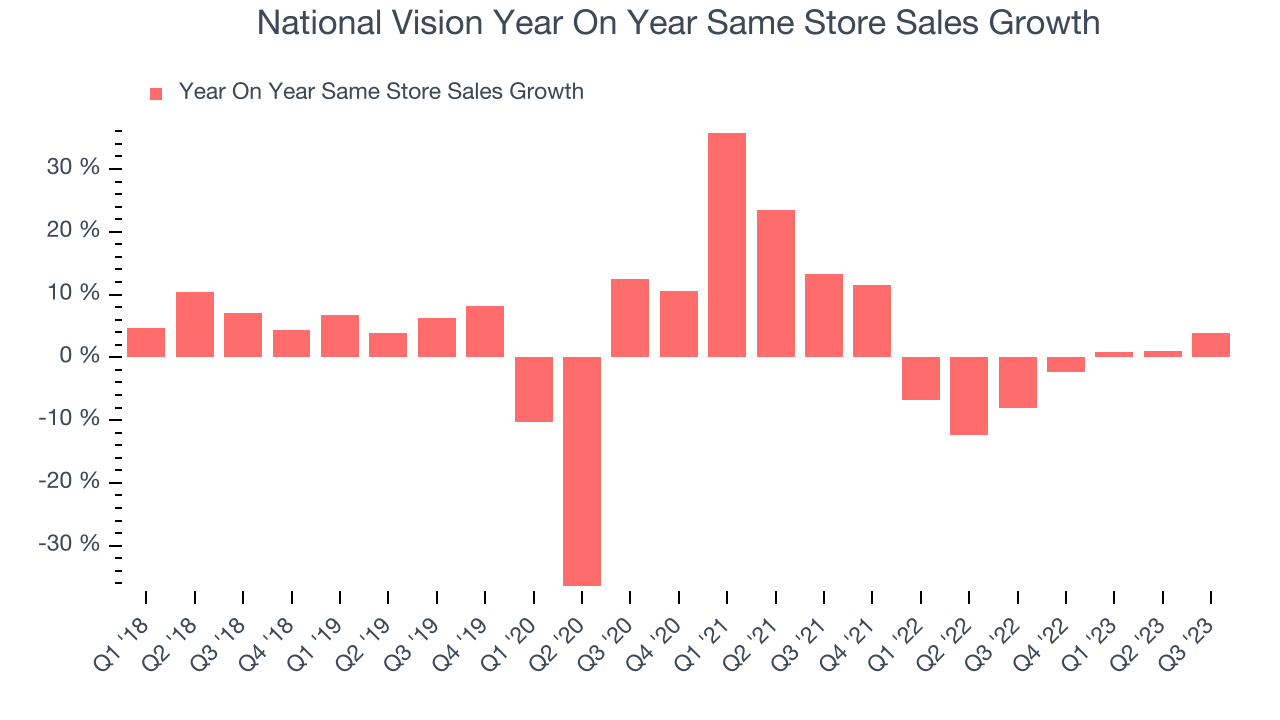

- Same-Store Sales were up 3.8% year on year (beat vs. expectations)

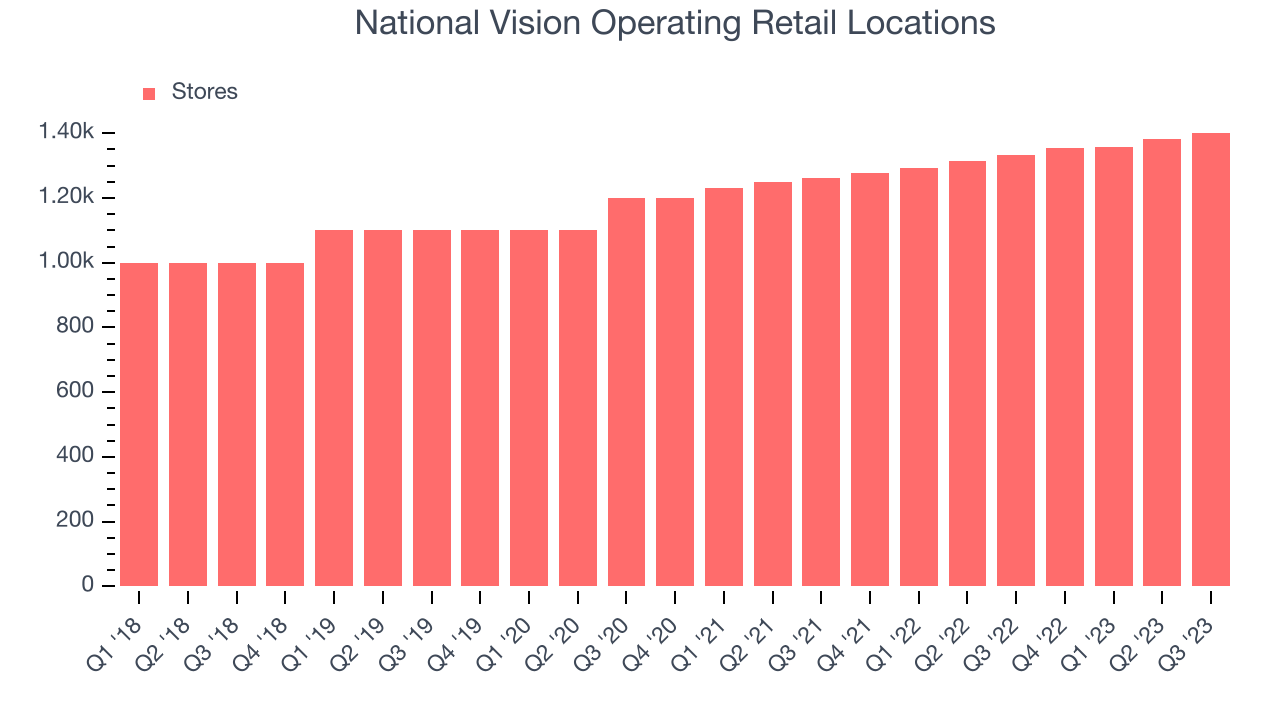

- Store Locations: 1,402 at quarter end, increasing by 70 over the last 12 months

Reade Fahs, National Vision's CEO, said, “Our third quarter results reflect ongoing strength in our managed care business as well as continued progress on our strategic initiatives focused on expanding exam capacity, particularly within America’s Best. We delivered a solid Back to School selling season, supported by our focus on delivering incredible value while offering exceptional customer service.”

Operating under multiple brands, National Vision (NYSE:EYE) sells optical products such as eyeglasses and provides optical services such as eye exams.

Specialty Retail

Some retailers try to sell everything under the sun, while others—appropriately called Specialty Retailers—focus on selling a narrow category and aiming to be exceptional at it. Whether it’s eyeglasses, sporting goods, or beauty and cosmetics, these stores win with depth of product in their category as well as in-store expertise and guidance for shoppers who need it. E-commerce competition exists and waning retail foot traffic impacts these retailers, but the magnitude of the headwinds depends on what they sell and what extra value they provide in their stores.

Sales Growth

National Vision is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 5.6% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre , but to its credit, it opened new stores and expanded its reach.

This quarter, National Vision reported solid year-on-year revenue growth of 6.6% and its revenue of $532.4 million outperformed analysts' estimates by 1.1%. Looking ahead, the Wall Street analysts covering the company expect revenue to remain relatively flat over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Number of Stores

When a retailer like National Vision is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, National Vision's store count increased by 70 locations, or 5.3%, to 1,402 total retail locations in the most recently reported quarter.

Taking a step back, the company has opened new stores quickly over the last eight quarters, averaging 5.5% annual growth in new locations. This store growth outpaces the broader consumer retail sector. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

National Vision's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 1.6% year on year. This performance is quite concerning and the company should reconsider its strategy before investing its precious capital into new store buildouts.

In the latest quarter, National Vision's same-store sales rose 3.8% year on year. This growth was a well-appreciated turnaround from the 8.1% year-on-year decline it posted 12 months ago, showing the business is regaining momentum.

Key Takeaways from National Vision's Q3 Results

With a market capitalization of $1.32 billion, National Vision is among smaller companies, but its $265.8 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

We were impressed by how significantly National Vision blew past analysts' EPS expectations this quarter, driven by comparable store sales and revenue beats. While full year revenue guidance was maintained, operating income and EPS guidance was riased. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is flat after reporting and currently trades at $16.84 per share.

So should you invest in National Vision right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.