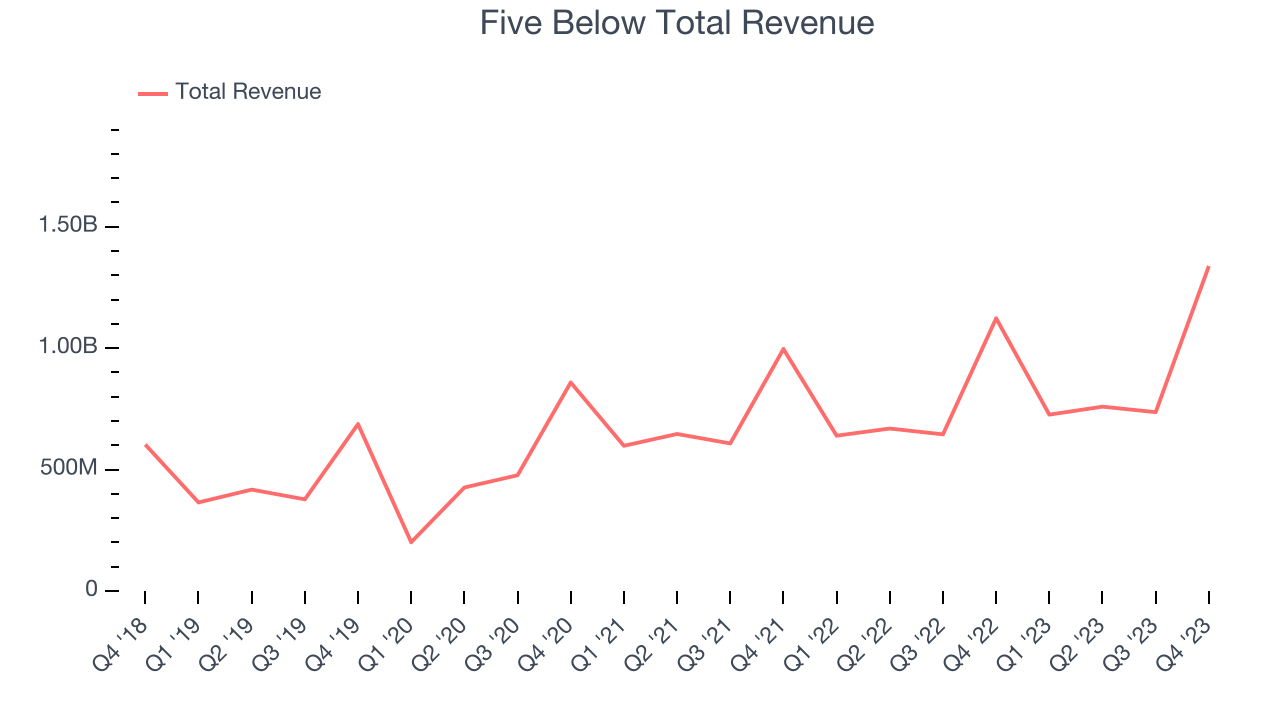

Discount retailer Five Below (NASDAQ:FIVE) fell short of analysts' expectations in Q4 CY2023, with revenue up 19.1% year on year to $1.34 billion. Next quarter's revenue guidance of $836 million also underwhelmed, coming in 1.8% below analysts' estimates. It made a GAAP profit of $3.65 per share, improving from its profit of $3.07 per share in the same quarter last year.

Is now the time to buy Five Below? Find out by accessing our full research report, it's free.

Five Below (FIVE) Q4 CY2023 Highlights:

- Revenue: $1.34 billion vs analyst estimates of $1.35 billion (0.9% miss)

- EPS: $3.65 vs analyst expectations of $3.78 (3.5% miss)

- Revenue Guidance for Q1 CY2024 is $836 million at the midpoint, below analyst estimates of $851.5 million

- Management's revenue guidance for the upcoming financial year 2024 is $4.02 billion at the midpoint, missing analyst estimates by 2.2% and implying 12.9% growth (vs 15.1% in FY2023)

- Gross Margin (GAAP): 41.2%, up from 40.3% in the same quarter last year

- Free Cash Flow of $304.6 million, similar to the same quarter last year

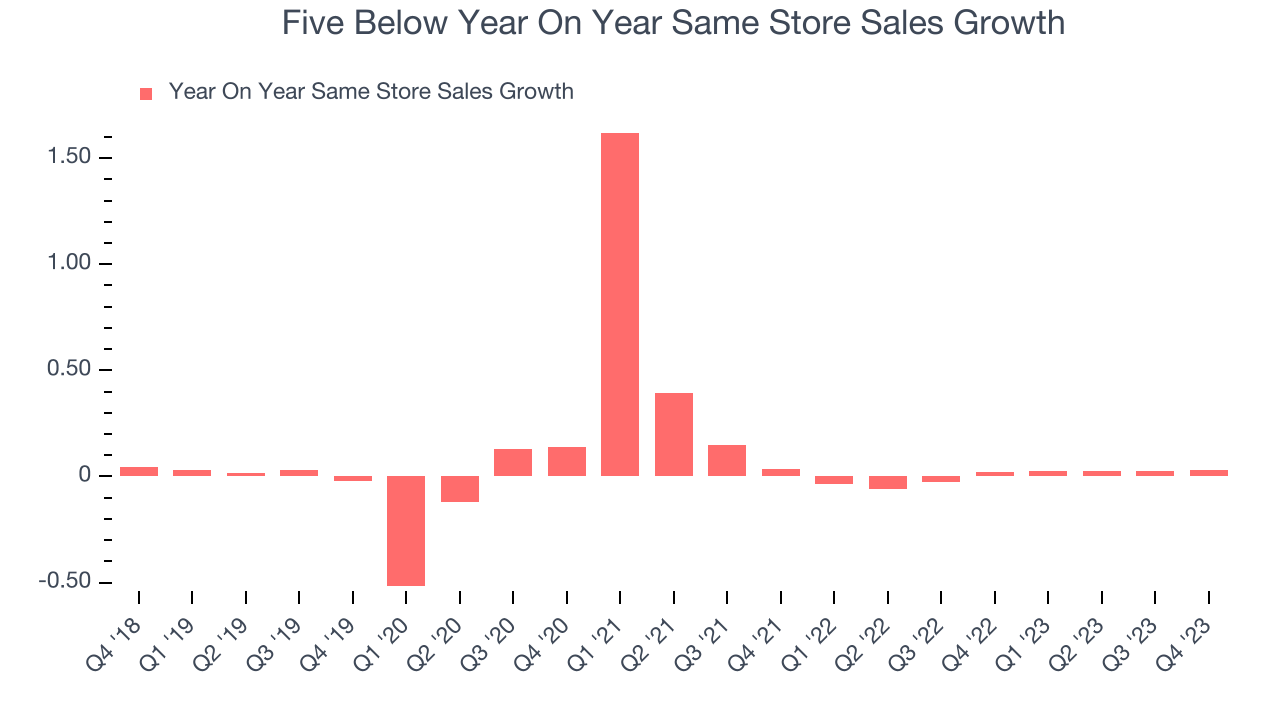

- Same-Store Sales were up 3.1% year on year

- Store Locations: 1,544 at quarter end, increasing by 204 over the last 12 months

- Market Capitalization: $11.41 billion

Joel Anderson, President and CEO of Five Below, stated, "Holiday 2023 marked a strong end to the year for sales performance as our amazing assortment of Wow product drove yet another quarter of comp transaction growth, led by the Five Beyond format stores. In fiscal 2023, we opened a record 205 new stores and ended the year with over half of our comparable stores in the Five Beyond format. The benefit of strong sales performance to our profitability was offset by higher than anticipated shrink headwinds, resulting in earnings at the low end of our guidance range."

Often facilitating a treasure hunt shopping experience, Five Below (NASDAQ:FIVE) is an American discount retailer that sells a variety of products from mobile phone cases to candy to sports equipment for largely $5 or less.

Discount General Merchandise Retailer

Broadline discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Sales Growth

Five Below is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the other hand, it has an edge over smaller competitors with fewer resources and can still flex high growth rates because it's growing off a smaller base than its larger counterparts.

As you can see below, the company's annualized revenue growth rate of 17.8% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was excellent as it added more brick-and-mortar locations and increased sales at existing, established stores.

This quarter, Five Below's revenue grew 19.1% year on year to $1.34 billion, falling short of Wall Street's estimates. The company is guiding for revenue to rise 15.1% year on year to $836 million next quarter, improving from the 13.5% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 15.5% over the next 12 months, a deceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

Five Below's demand within its existing stores has barely increased over the last eight quarters. On average, the company's same-store sales growth has been flat. This performance suggests that Five Below should consider improving its foot traffic and efficiency before expanding its physical footprint.

In the latest quarter, Five Below's same-store sales rose 3.1% year on year. This growth was an acceleration from the 1.9% year-on-year increase it posted 12 months ago, which is always an encouraging sign.

Key Takeaways from Five Below's Q4 Results

We struggled to find many strong positives in these results. Its revenue and EPS slightly missed analysts' estimates, but most importantly, its full-year 2024 revenue and earnings guidance fell short. Investors are punishing the stock for its weak outlook, and the company is down 12.4% on the results. It currently trades at $183 per share.

Five Below may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.