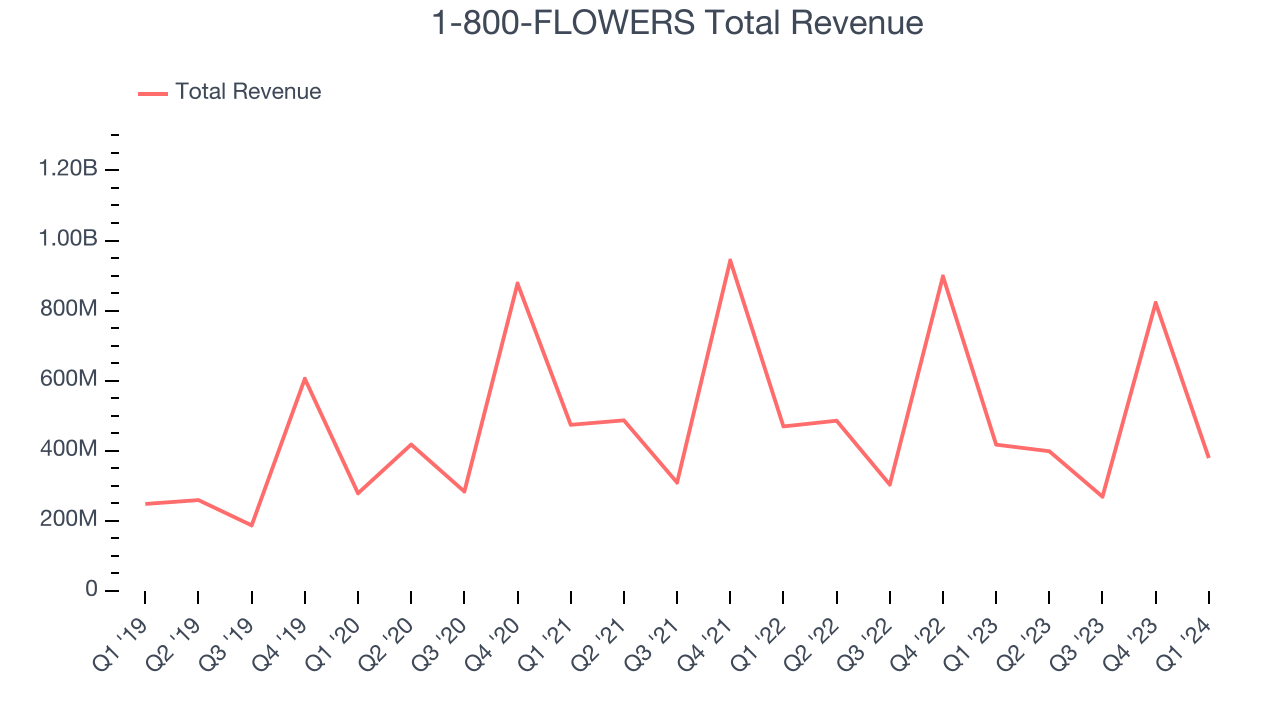

E-commerce florist and gift retailer 1-800-FLOWERS (NASDAQ:FLWS) fell short of analysts' expectations in Q1 CY2024, with revenue down 9.1% year on year to $379.4 million. It made a GAAP loss of $0.26 per share, improving from its loss of $1.10 per share in the same quarter last year.

Is now the time to buy 1-800-FLOWERS? Find out by accessing our full research report, it's free.

1-800-FLOWERS (FLWS) Q1 CY2024 Highlights:

- Revenue: $379.4 million vs analyst estimates of $383.8 million (1.2% miss)

- EPS: -$0.26 vs analyst expectations of -$0.25 (6.1% miss)

- Gross Margin (GAAP): 36.6%, up from 33.6% in the same quarter last year

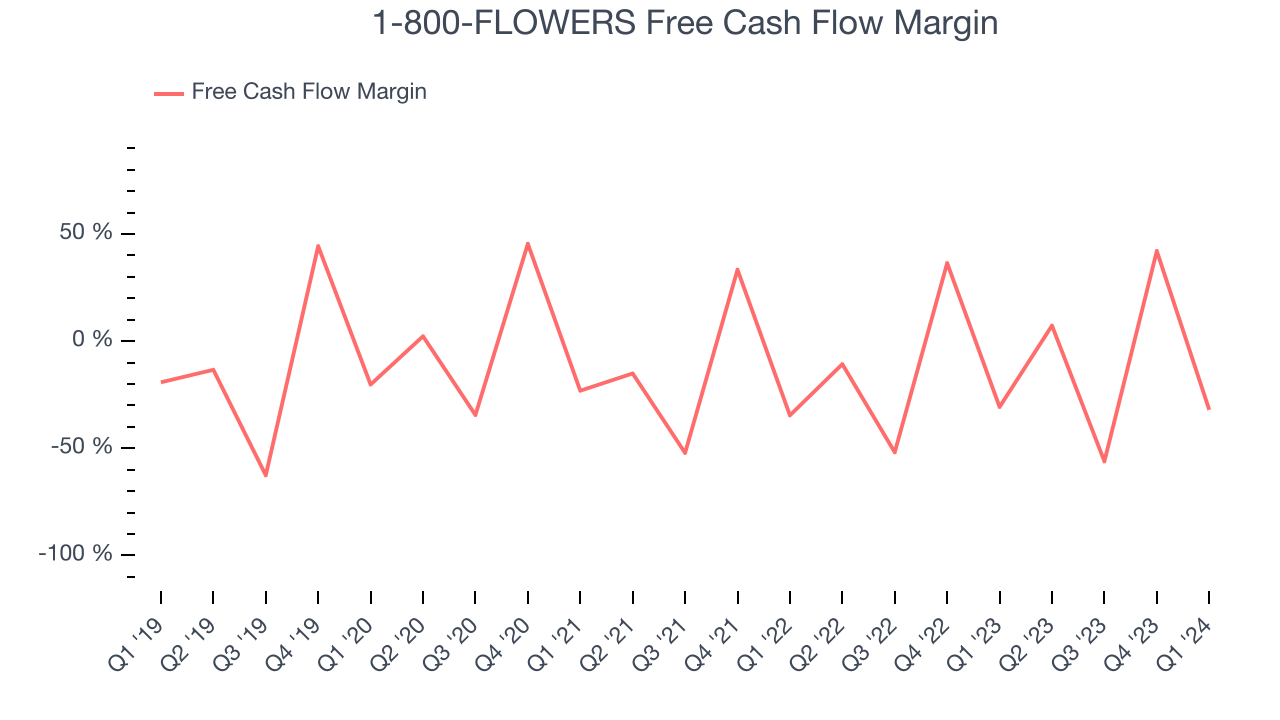

- Free Cash Flow was -$121.4 million, down from $345.8 million in the previous quarter

- Market Capitalization: $584.3 million

“As we continue on our reversion to the mean path, our gross margin continued its significant recovery, improving 300 basis points during the third quarter,” said Jim McCann, Chairman and Chief Executive Officer of 1-800-FLOWERS.COM.

Founded in 1976, 1-800-FLOWERS (NASDAQ:FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

Specialized Consumer Services

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one may grow for years. 1-800-FLOWERS's annualized revenue growth rate of 8.3% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. 1-800-FLOWERS's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 8% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. 1-800-FLOWERS's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 8% over the last two years.

This quarter, 1-800-FLOWERS missed Wall Street's estimates and reported a rather uninspiring 9.1% year-on-year revenue decline, generating $379.4 million of revenue. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, 1-800-FLOWERS has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 2.3%, subpar for a consumer discretionary business.

1-800-FLOWERS burned through $121.4 million of cash in Q1, equivalent to a negative 32% margin, increasing its cash burn by 5.2% year on year. Over the next year, analysts predict 1-800-FLOWERS's cash profitability will fall. Their consensus estimates imply its LTM free cash flow margin of 5.5% will decrease to 1.6%.

Key Takeaways from 1-800-FLOWERS's Q1 Results

We struggled to find many strong positives in these results. Its revenue, operating margin, and EPS fell short of Wall Street's estimates. Management cited a weak demand environment for consumer discretionary products, echoing what other companies in the sector have shared this quarter. Looking ahead, the company expects sales to continue declining, but its full-year EBITDA guidance of $97.5 million at the midpoint beat analysts' expectations. Overall, the results could have been better. The company is down 3.4% on the results and currently trades at $8.73 per share.

1-800-FLOWERS may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.