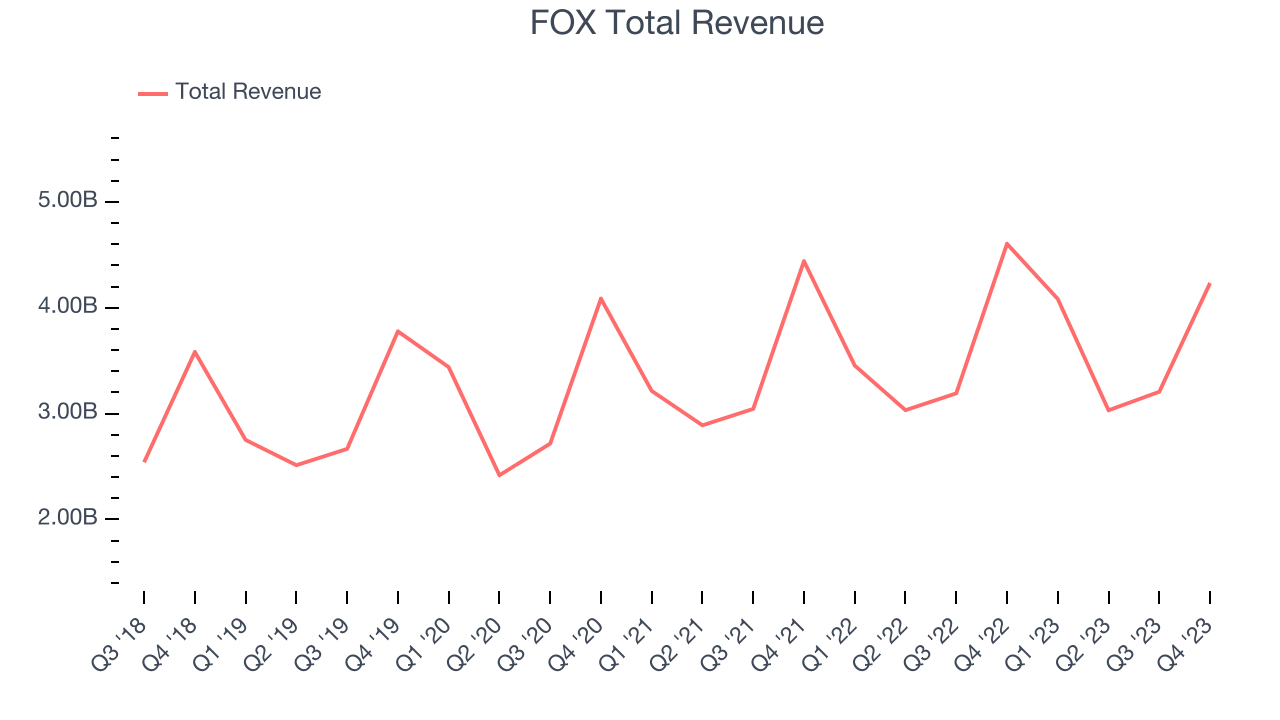

Cable news and media network Fox (NASDAQ:FOXA) reported results in line with analysts' expectations in Q2 FY2024, with revenue down 8.1% year on year to $4.23 billion. It made a non-GAAP profit of $0.34 per share, down from its profit of $0.48 per share in the same quarter last year.

Is now the time to buy FOX? Find out by accessing our full research report, it's free.

FOX (FOXA) Q2 FY2024 Highlights:

- Revenue: $4.23 billion vs analyst estimates of $4.21 billion (small beat)

- EPS (non-GAAP): $0.34 vs analyst estimates of $0.12 ($0.22 beat)

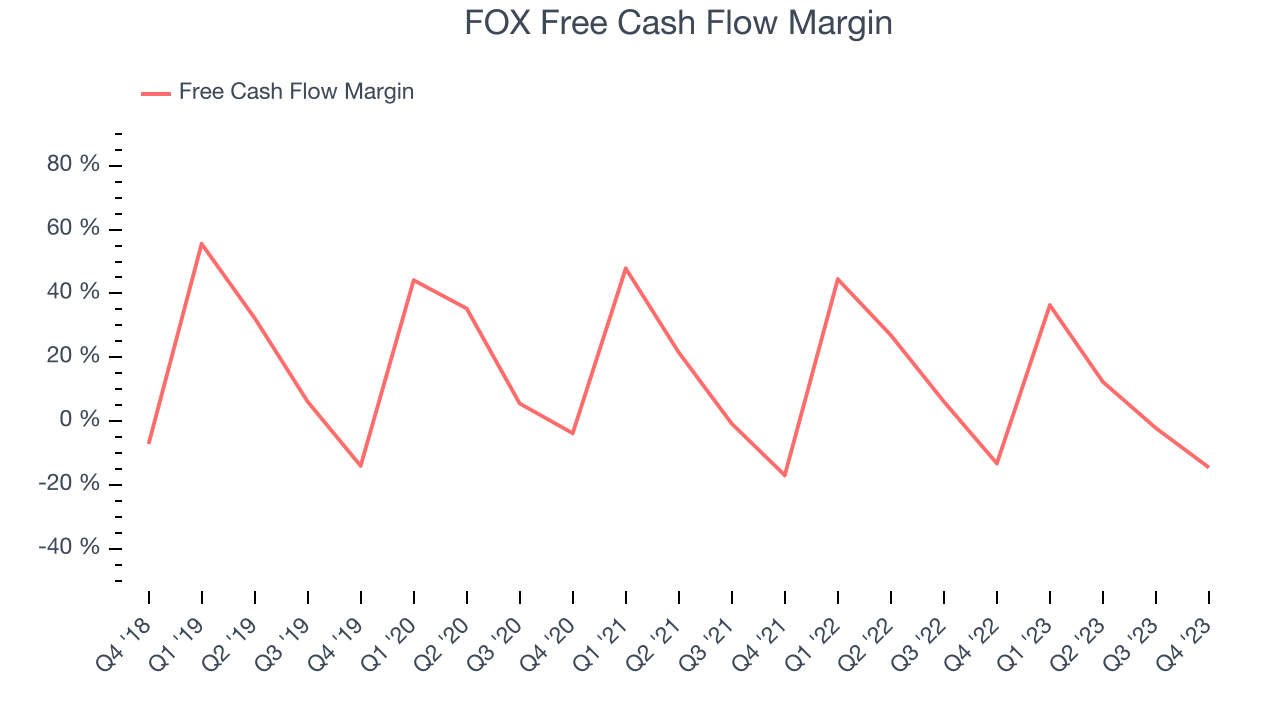

- Free Cash Flow was -$615 million compared to -$70 million in the previous quarter

- Gross Margin (GAAP): 19.9%, down from 23.4% in the same quarter last year

- Market Capitalization: $14.73 billion

Founded in 1915, Fox (NASDAQ:FOXA) is a diversified media company, operating prominent cable news, television broadcasting, and digital media platforms.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Sales Growth

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. FOX's annualized revenue growth rate of 5.8% over the last 5 years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. FOX's recent history shows the business has slowed, as its annualized revenue growth of 3.5% over the last 2 years is below its 5-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. FOX's recent history shows the business has slowed, as its annualized revenue growth of 3.5% over the last 2 years is below its 5-year trend.

We can dig even further into the company's revenue dynamics by analyzing its most important segments, Cable Network Programming and Television, which are 39.2% and 60% of revenue. Over the last 2 years, FOX's Cable Network Programming revenue (licensing, retransmission, advertising) was flat while its Television revenue (advertising) averaged 7.3% year-on-year growth.

This quarter, FOX reported a rather uninspiring 8.1% year-on-year revenue decline to $4.23 billion of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, FOX has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 12%, slightly better than the broader consumer discretionary sector.

FOX burned through $615 million of cash in Q2, equivalent to a negative 14.5% margin, in line with its cash burn last year. Over the next year, analysts predict FOX's cash profitability will improve. Their consensus estimates imply its LTM free cash flow margin of 8.1% will increase to 11.6%.

Key Takeaways from FOX's Q2 Results

We were impressed by how significantly FOX blew past analysts' EBITDA and EPS estimates this quarter. Its revenue, although down year on year, also slightly beat thanks to better-than-expected affiliate (retransmission fee) and advertising revenue. Revenue was down this quarter because of the absence of FIFA Men's World Cup games. This headwind, however, was partially offset by its renewed NFL contract. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 5% after reporting and currently trades at $33.2 per share.

So should you invest in FOX right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.