Cable news and media network Fox (NASDAQ:FOXA) reported results in line with analysts' expectations in Q2 FY2024, with revenue down 8.1% year on year to $4.23 billion. It made a non-GAAP profit of $0.34 per share, down from its profit of $0.48 per share in the same quarter last year.

FOX (FOXA) Q2 FY2024 Highlights:

- Revenue: $4.23 billion vs analyst estimates of $4.21 billion (small beat)

- EPS (non-GAAP): $0.34 vs analyst estimates of $0.12 ($0.22 beat)

- Free Cash Flow was -$615 million compared to -$70 million in the previous quarter

- Gross Margin (GAAP): 19.9%, down from 23.4% in the same quarter last year

- Market Capitalization: $14.73 billion

Founded in 1915, Fox (NASDAQ:FOXA) is a diversified media company, operating prominent cable news, television broadcasting, and digital media platforms.

FOX was initially established to meet early 20th-century demands for entertainment and news. Over the decades, the company has significantly evolved, branching into various media segments and adopting digital platforms.

FOX provides a broad spectrum of media services including news coverage, sports broadcasting, and other entertainment. FOX caters to a large audience, seeking engagement with diverse viewers, from news aficionados to entertainment consumers.

The company's revenue is primarily derived from advertising, subscription fees, and content licensing. Furthermore, it must produce quality content to maintain its channel space.

A notable aspect of FOX's value proposition is its focus on delivering content that resonates with specific viewer segments, particularly those seeking a certain perspective on news and entertainment. This targeted content strategy has enabled FOX to carve out a niche in the competitive media landscape.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Competitors in the media and entertainment industry include Comcast Corporation (NASDAQ:CMCSA), Walt Disney (NYSE:DIS), and Paramount Global (NASDAQ:PARA).Sales Growth

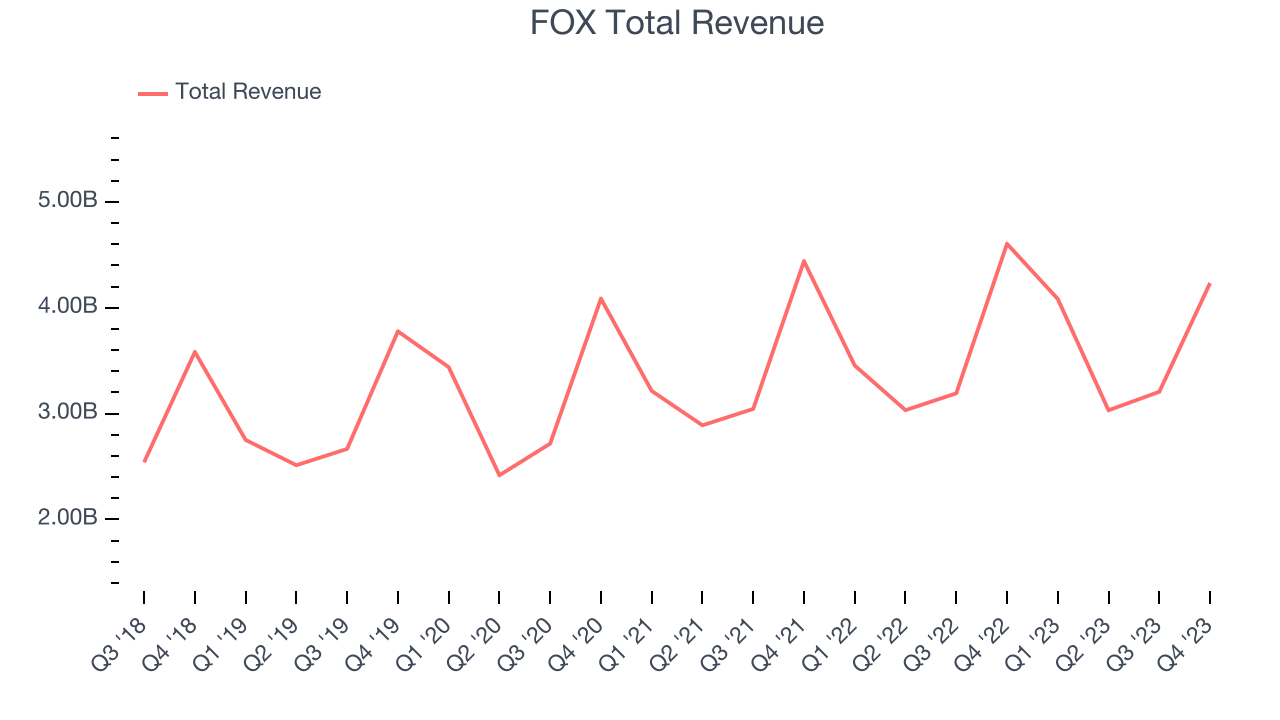

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. FOX's annualized revenue growth rate of 5.8% over the last 5 years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. FOX's recent history shows the business has slowed, as its annualized revenue growth of 3.5% over the last 2 years is below its 5-year trend.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. FOX's recent history shows the business has slowed, as its annualized revenue growth of 3.5% over the last 2 years is below its 5-year trend.

We can understand the company's revenue dynamics even better by analyzing its most important segments, Cable Network Programming and Television, which are 39.2% and 60% of revenue. Over the last 2 years, FOX's Cable Network Programming revenue (licensing, retransmission, advertising) was flat while its Television revenue (advertising) averaged 7.3% year-on-year growth.

This quarter, FOX reported a rather uninspiring 8.1% year-on-year revenue decline to $4.23 billion of revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

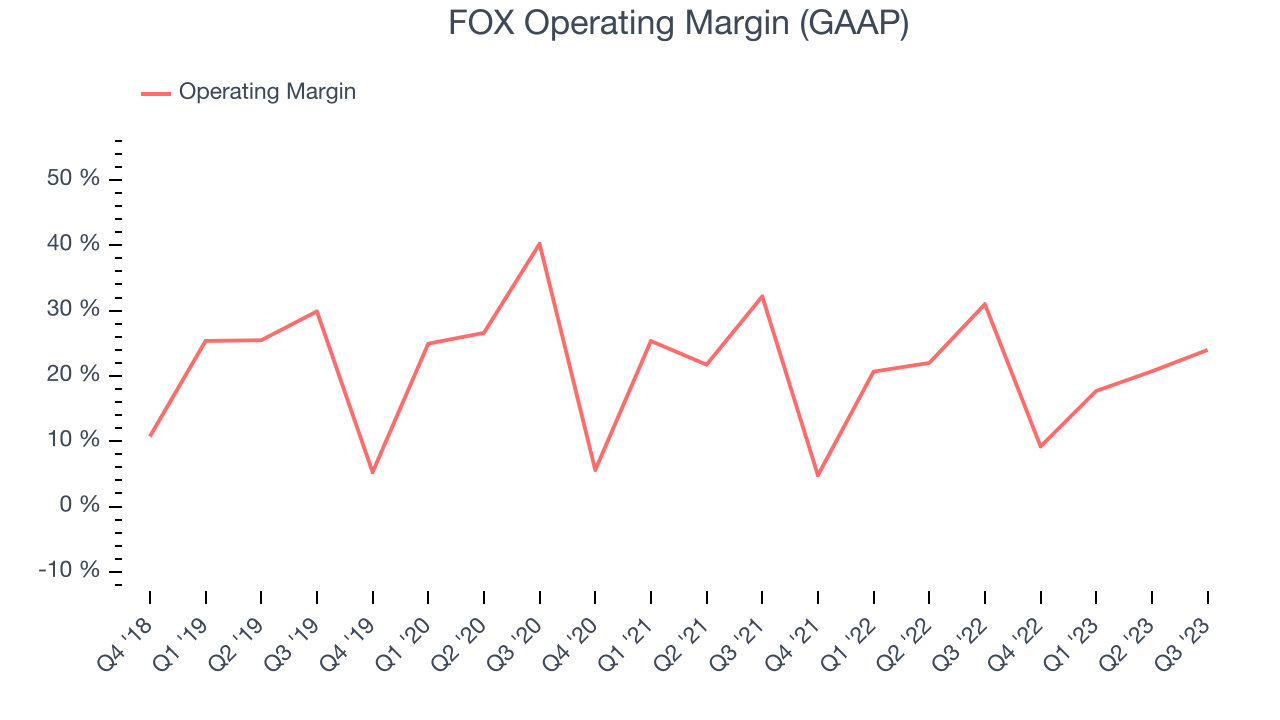

Operating Margin

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

FOX has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 20.7%.

in line with the same quarter last year. This indicates the company's costs have been relatively stable.

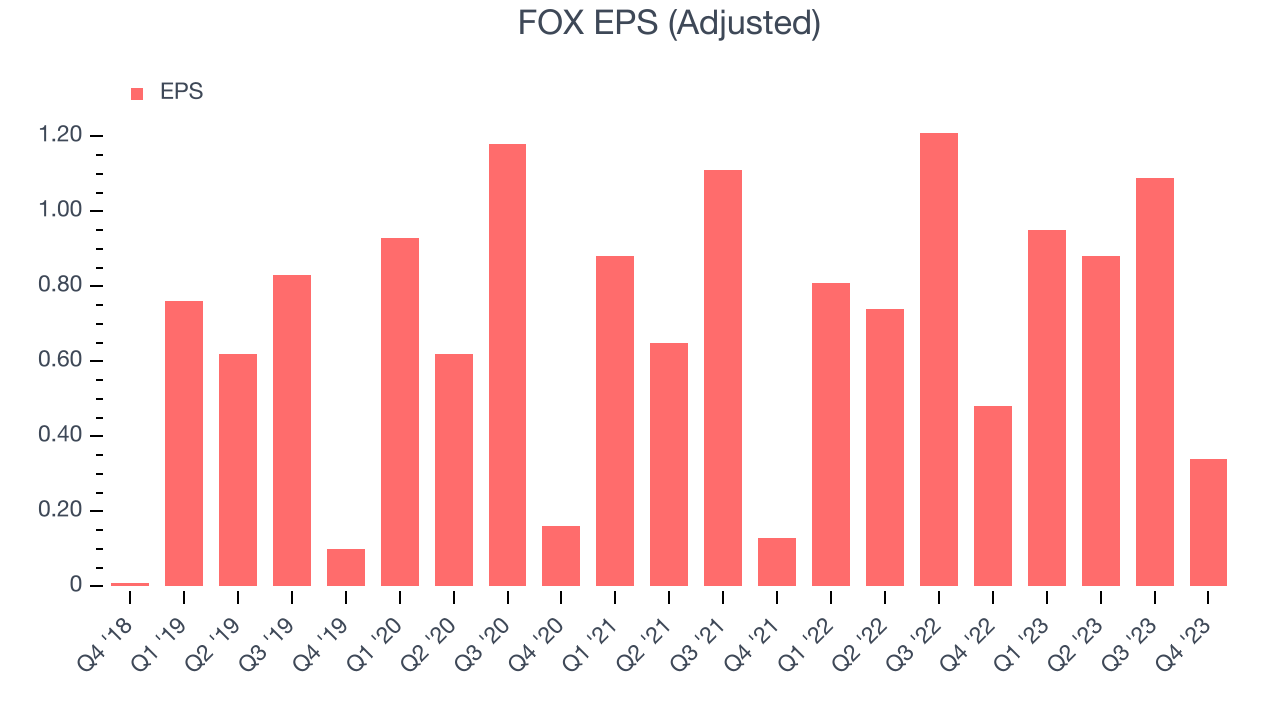

EPS

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last 5 years, FOX's EPS grew 22.6%, translating into a weak 4.2% compounded annual growth rate. Furthermore, This performance is lower than its 5.8% annualized revenue growth over the same period. Let's dig into why.

FOX's operating margin and share count have improved over the last 5 years, meaning its EPS growth lagged its revenue growth because it had a higher tax rate and interest expenses as a percentage of revenue. This isn't great, but we put less emphasis on the results as they don’t tell us as much about business fundamentals as operating margins and share buybacks.In Q2, FOX reported EPS at $0.34, down from $0.48 in the same quarter a year ago. This print easily cleared analysts' estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects FOX to grow its earnings. Analysts are projecting its LTM EPS of $3.26 to climb by 9.1% to $3.56.

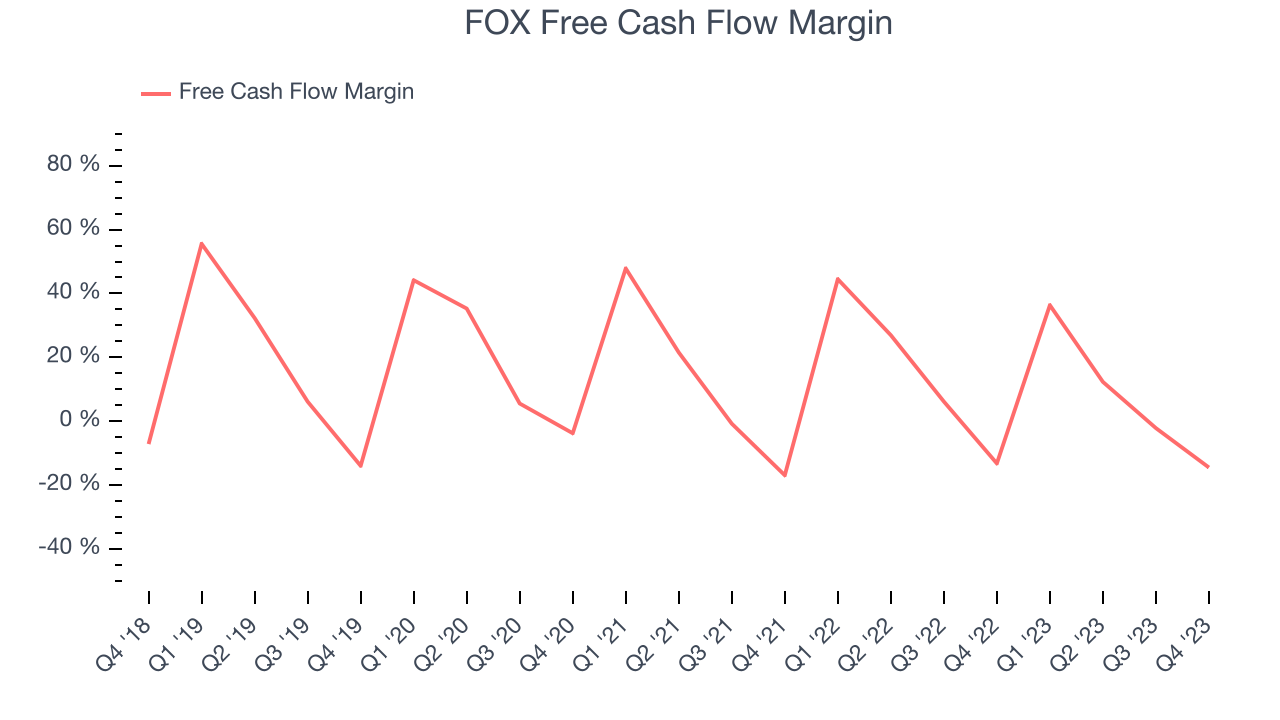

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Over the last two years, FOX has shown decent cash profitability, giving it some reinvestment opportunities. The company's free cash flow margin has averaged 12%, slightly better than the broader consumer discretionary sector.

FOX burned through $615 million of cash in Q2, equivalent to a negative 14.5% margin, in line with its cash burn last year. Over the next year, analysts predict FOX's cash profitability will improve. Their consensus estimates imply its LTM free cash flow margin of 8.1% will increase to 11.6%.

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company's revenue growth was profitable. But was it capital-efficient? If two companies had equal growth, we’d prefer the one with lower reinvestment requirements.

Understanding a company’s ROIC (return on invested capital) gives us insight into this because it factors the total debt and equity needed to generate operating profits. This metric is a proxy for not only the capital efficiency of a business but also a management team's ability to allocate limited resources.

FOX's five-year average return on invested capital was 14.1%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable growth initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. FOX's ROIC has stayed the same over the last two years. If FOX wants to become an investable business, it will need to increase its returns.

Key Takeaways from FOX's Q2 Results

We were impressed by how significantly FOX blew past analysts' EBITDA and EPS estimates this quarter. Its revenue, although down year on year, also slightly beat thanks to better-than-expected affiliate (retransmission fee) and advertising revenue. Revenue was down this quarter because of the absence of FIFA Men's World Cup games. This headwind, however, was partially offset by its renewed NFL contract. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is up 5% after reporting and currently trades at $33.2 per share.

Is Now The Time?

FOX may have had a favorable quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of FOX, we'll be cheering from the sidelines. Its revenue growth has been uninspiring over the last five years, and analysts expect growth to deteriorate from here. And while its strong operating margins show it's a well-run business, unfortunately, its average annual EPS growth over the last five years has been disappointing.

FOX's price-to-earnings ratio based on the next 12 months is 8.9x. While we've no doubt one can find things to like about FOX, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.