Software development tools maker JFrog (NASDAQ:FROG) beat analysts' expectations in Q1 CY2024, with revenue up 25.7% year on year to $100.3 million. The company expects next quarter's revenue to be around $103.5 million, in line with analysts' estimates. It made a non-GAAP profit of $0.16 per share, improving from its profit of $0.06 per share in the same quarter last year.

Is now the time to buy JFrog? Find out by accessing our full research report, it's free.

JFrog (FROG) Q1 CY2024 Highlights:

- Revenue: $100.3 million vs analyst estimates of $98.62 million (1.7% beat)

- EPS (non-GAAP): $0.16 vs analyst estimates of $0.14 (11.8% beat)

- Revenue Guidance for Q2 CY2024 is $103.5 million at the midpoint, roughly in line with what analysts were expecting (operating profit guidance also in line at the midpoint)

- The company slightly raised its revenue guidance for the full year to $427.5 million at the midpoint (slightly above expectations, full year operating profit guidance in line)

- Gross Margin (GAAP): 79.5%, up from 76.9% in the same quarter last year

- Free Cash Flow of $16.63 million, down 48% from the previous quarter

- Net Revenue Retention Rate: 118%, in line with the previous quarter

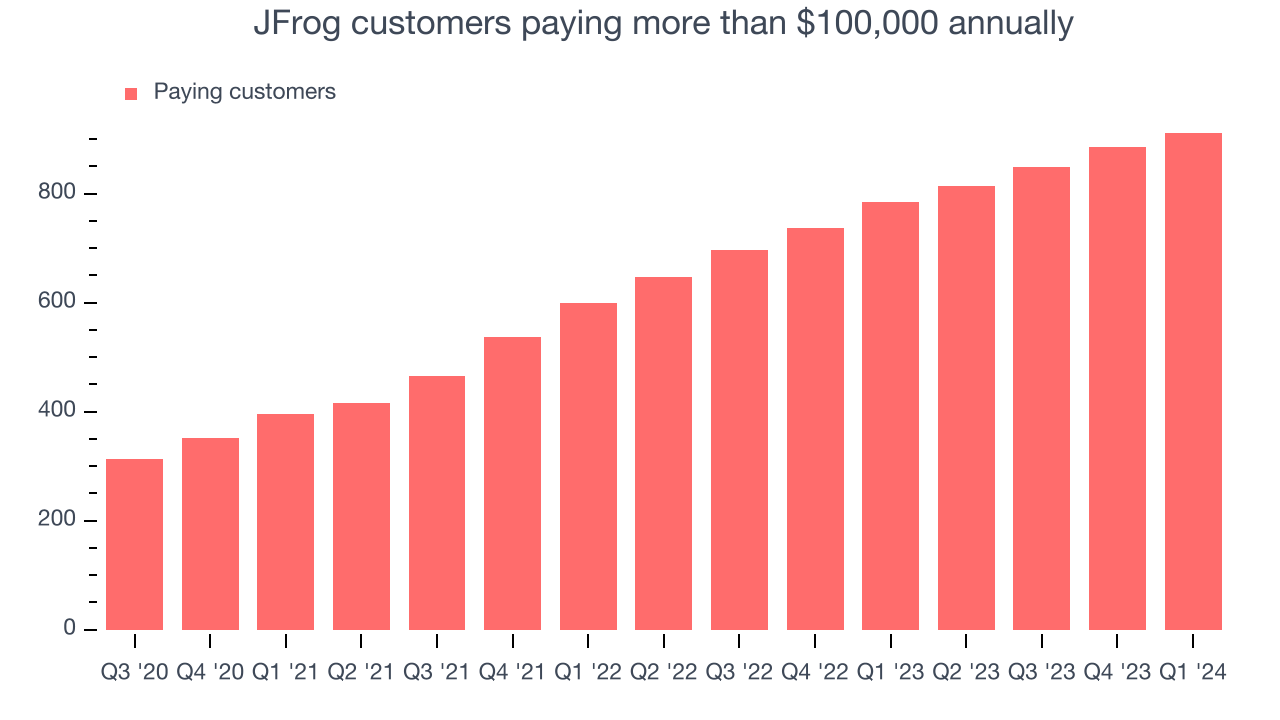

- Customers: 911 customers paying more than $100,000 annually

- Market Capitalization: $4.41 billion

"The landscape of DevOps and security is undergoing dramatic change, and I'm thrilled about the future prospects for JFrog. Our platform's evolution into a comprehensive solution spanning DevOps, DevSecOps, MLOps and MLSecOps sets a new standard in enterprise capabilities,” stated Shlomi Ben Haim, JFrog CEO and Co-founder.

Named after the founders' affinity for frogs, JFrog (NASDAQ:FROG) provides a software-as-a-service platform that makes developing and releasing software easier and faster, especially for large teams.

Developer Operations

As Marc Andreessen says, "software is eating the world" which means the volume of software produced is exploding. But building software is complex and difficult work which drives demand for software tools that help increase the speed, quality, and security of software deployment.

Sales Growth

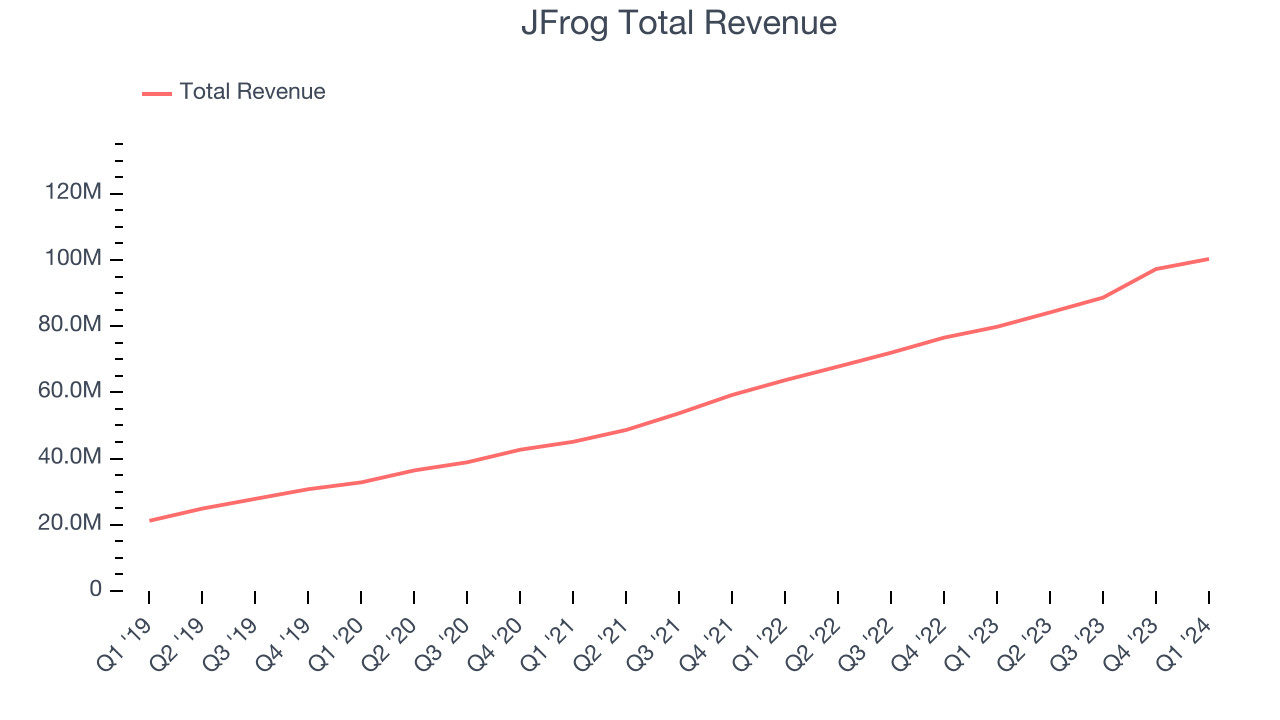

As you can see below, JFrog's revenue growth has been very strong over the last three years, growing from $45.09 million in Q1 2021 to $100.3 million this quarter.

This quarter, JFrog's quarterly revenue was once again up a very solid 25.7% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $3.05 million in Q1 compared to $8.62 million in Q4 CY2023. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that JFrog is expecting revenue to grow 23% year on year to $103.5 million, in line with the 24.1% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 20.7% over the next 12 months before the earnings results announcement.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Large Customers Growth

This quarter, JFrog reported 911 enterprise customers paying more than $100,000 annually, an increase of 25 from the previous quarter. That's a bit fewer contract wins than last quarter and quite a bit below what we've typically observed over the past four quarters, suggesting that its sales momentum with large customers is slowing.

Key Takeaways from JFrog's Q1 Results

It was encouraging to see JFrog narrowly top analysts' revenue expectations this quarter. On the other hand, its billings unfortunately missed analysts' expectations and its new large contract wins shrunk. Guidance for next quarter and the full year were roughly in line with expectations. Overall, this was a mixed quarter for JFrog and not as exciting as some of their previous convincing beats. The company is down 10.2% on the results and currently trades at $36.5 per share.

JFrog may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.