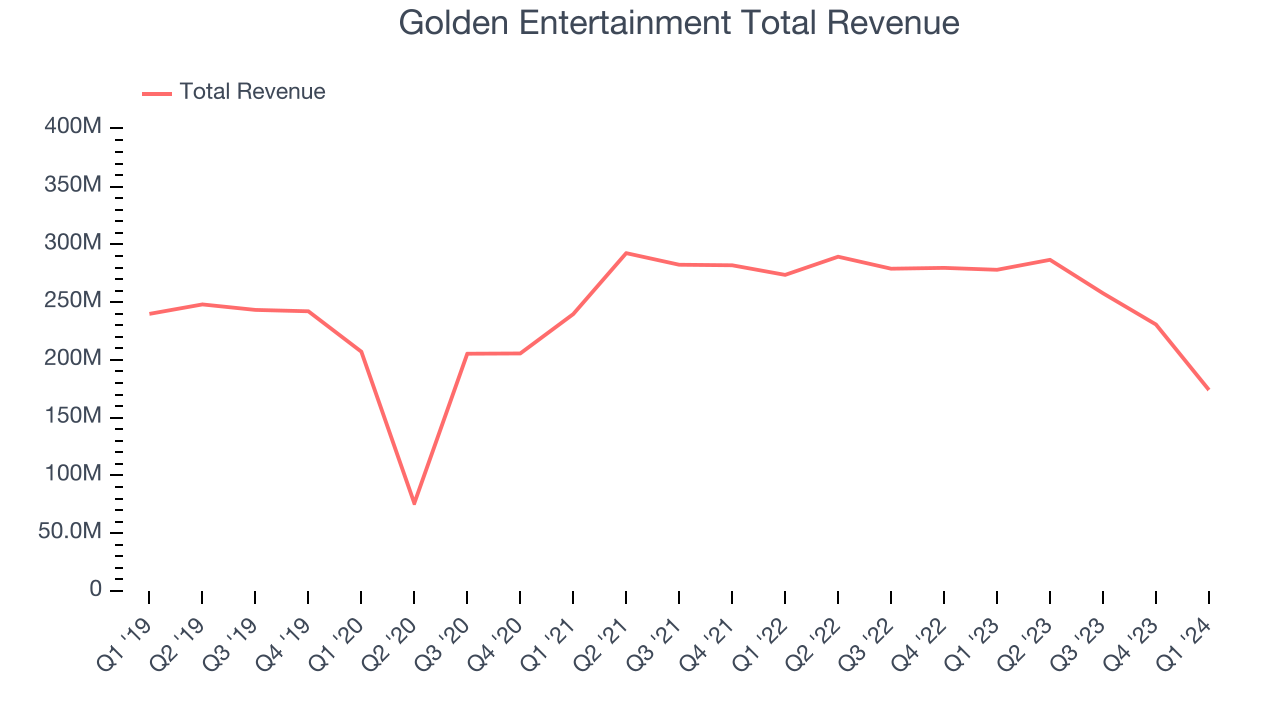

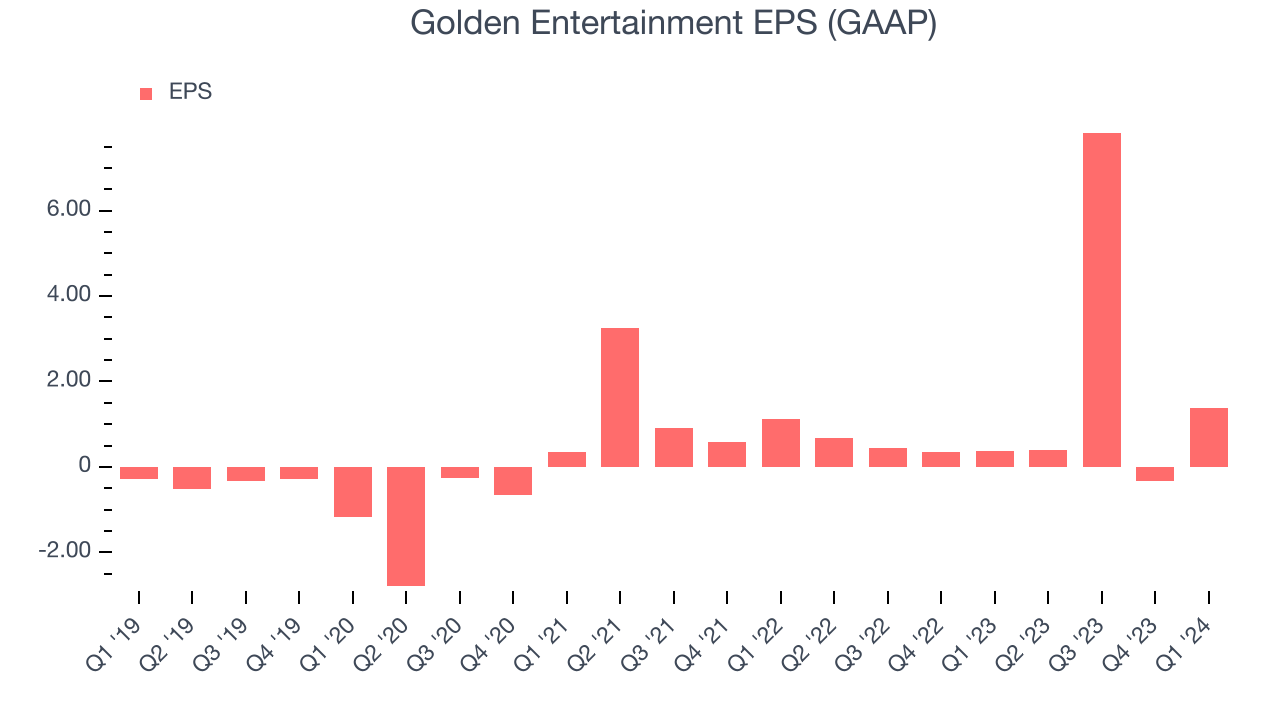

Casino, tavern, and slot machine operator Golden Entertainment (NASDAQ:GDEN) reported results ahead of analysts' expectations in Q1 CY2024, with revenue down 37.4% year on year to $174 million. It made a GAAP profit of $1.37 per share, improving from its profit of $0.38 per share in the same quarter last year.

Golden Entertainment (GDEN) Q1 CY2024 Highlights:

- Revenue: $174 million vs analyst estimates of $168.7 million (3.2% beat)

- Adjusted EBITDA: $40.5 million vs analyst estimates of $42.5 million (4.7% miss)

- One-time gain on sale helped reported operating income and EPS, although we'd highlight that this is not recurring or fundamental

- Gross Margin (GAAP): 53.2%, up from 42.6% in the same quarter last year

- Market Capitalization: $892.5 million

Founded in 2001, Golden Entertainment (NASDAQ:GDEN) is a gaming company operating casinos, taverns, and distributed gaming platforms.

Golden Entertainment emerged to provide a diversified gaming experience, capturing a unique market position by offering both traditional casino gaming and localized tavern gaming experiences. The company seeks to serve both casual gamers and gambling enthusiasts.

Golden Entertainment's services encompass comprehensive gaming options, including slot machines and table games. It also manages distributed gaming platforms, where it sells its slot machines to various non-casino locations like restaurants and convenience stores. This range caters to different customer preferences, from the vibrant casino environment to the convenience of casual neighborhood tavern gaming.

The company's revenues are derived from its casino operations, distributed gaming platforms, and tavern gaming and dining.

Casino Operator

Casino operators enjoy limited competition because gambling is a highly regulated industry. These companies can also enjoy healthy margins and profits. Have you ever heard the phrase ‘the house always wins’? Regulation cuts both ways, however, and casinos may face stroke-of-the-pen risk that suddenly limits what they can or can't do and where they can do it. Furthermore, digitization is changing the game, pun intended. Whether it’s online poker or sports betting on your smartphone, innovation is forcing these players to adapt to changing consumer preferences, such as being able to wager anywhere on demand.

Competitors in the gaming and entertainment sector include Boyd Gaming (NYSE:BYD), Caesars Entertainment (NASDAQ:CZR), and Red Rock Resorts (NASDAQ:RRR).Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Golden Entertainment's annualized revenue growth rate of 1.6% over the last five years was weak for a consumer discretionary business.  Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Golden Entertainment's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 8.4% over the last two years.

Within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends. That's why we also follow short-term performance. Golden Entertainment's recent history shows a reversal from its already weak five-year trend as its revenue has shown annualized declines of 8.4% over the last two years.

We can better understand the company's revenue dynamics by analyzing its most important segment, Gaming. Over the last two years, Golden Entertainment's Gaming revenue (Poker, Blackjack) averaged 12.8% year-on-year declines. This segment has lagged the company's overall sales.

This quarter, Golden Entertainment's revenue fell 37.4% year on year to $174 million but beat Wall Street's estimates by 3.2%. Looking ahead, Wall Street expects revenue to decline 25.6% over the next 12 months.

Operating Margin

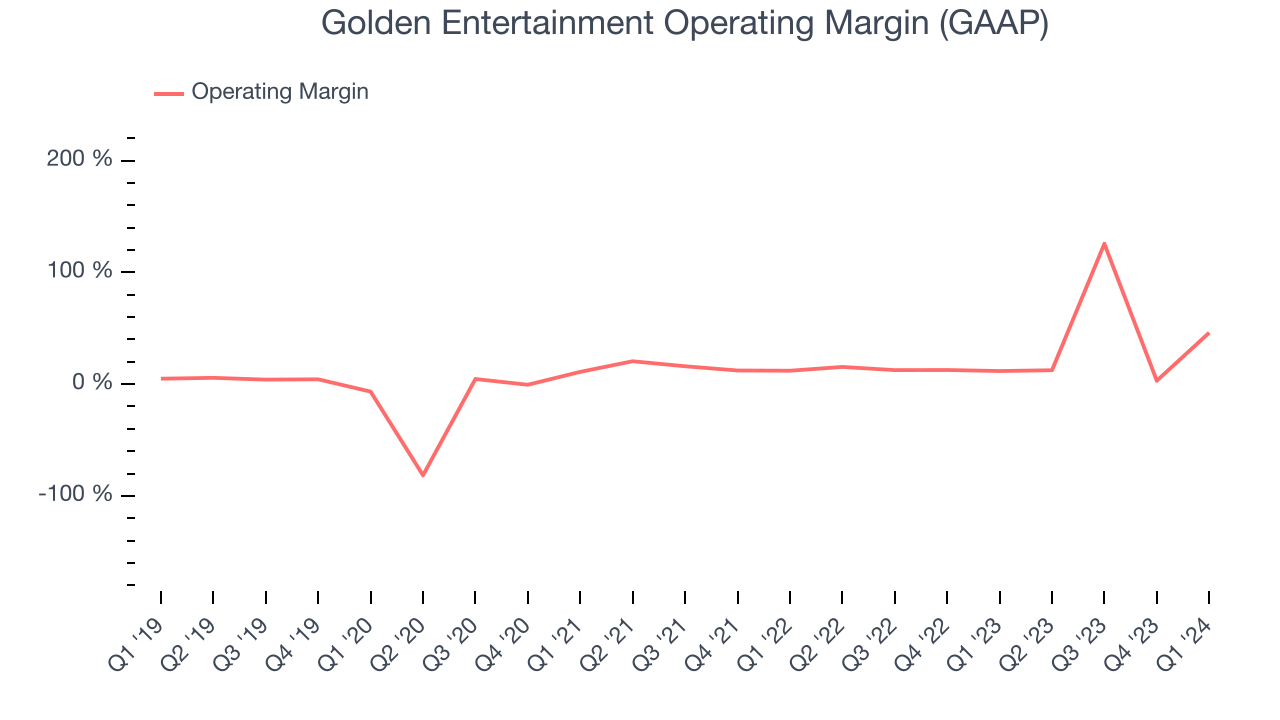

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Golden Entertainment has been a well-oiled machine over the last two years. It's demonstrated elite profitability for a consumer discretionary business, boasting an average operating margin of 28.6%.

This quarter, Golden Entertainment generated an operating profit margin of 46%, up 34.3 percentage points year on year. This was helped by a one-time, extraordinary gain on a sale of a business.

Over the next 12 months, Wall Street expects Golden Entertainment to become less profitable. Analysts are expecting the company’s LTM operating margin of 47.1% to decline to 11.5%.

EPS

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last five years, Golden Entertainment cut its earnings losses and improved its EPS by 58% each year. This performance is materially higher than its 1.6% annualized revenue growth over the same period. There are a few reasons for this, and understanding why can shed light on its fundamentals.

Golden Entertainment's operating margin has expanded 41.2 percentage points over the last five years, leading to higher profitability and earnings. Taxes and interest expenses can also affect EPS growth, but they don't tell us as much about a company's fundamentals.

In Q1, Golden Entertainment reported EPS at $1.37, up from $0.38 in the same quarter last year. This quarter's reported EPS was helped by a one-time, extraordinary gain on a sale of a business. This print easily cleared analysts' estimates. Over the next 12 months, Wall Street expects Golden Entertainment to perform poorly. Analysts are projecting its LTM EPS of $9.27 to shrink by 86% to $1.30.

Return on Invested Capital (ROIC)

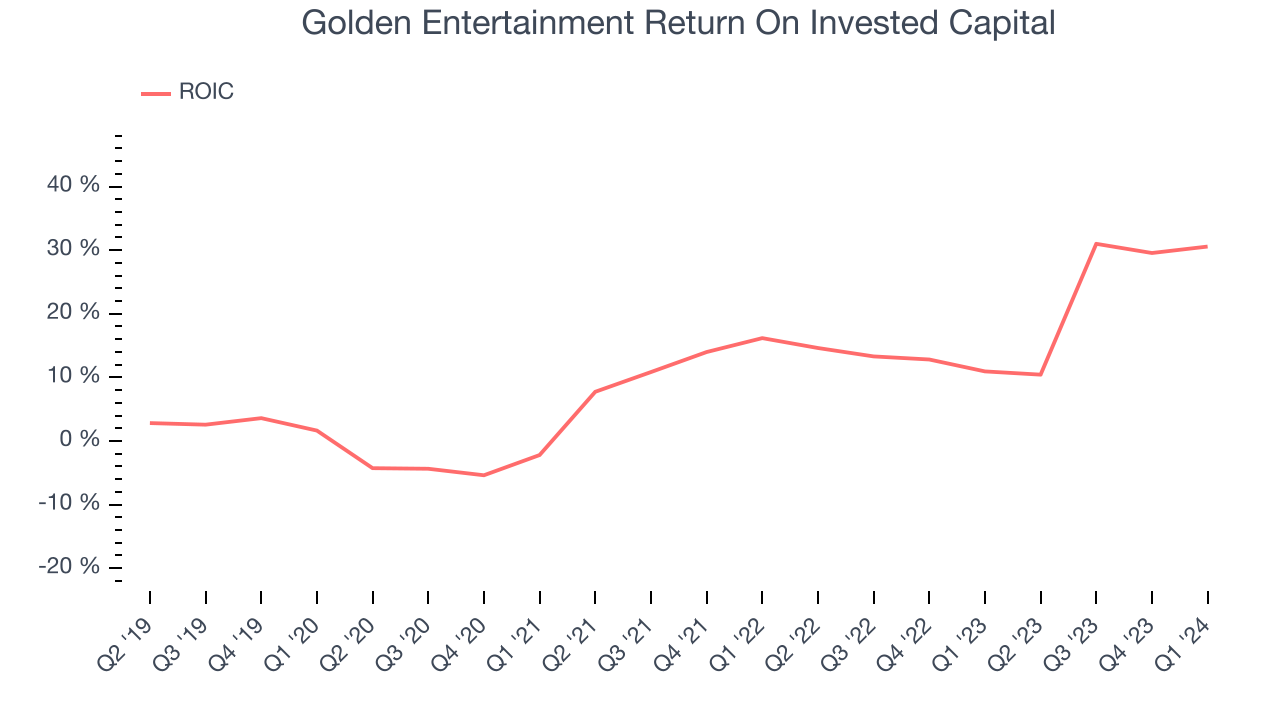

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Golden Entertainment's five-year average return on invested capital was 11.4%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Over the last few years, Golden Entertainment's ROIC has significantly increased. This is a good sign, and we hope the company can continue improving.

Balance Sheet Risk

As long-term investors, the risk we care most about is the permanent loss of capital. This can happen when a company goes bankrupt or raises money from a disadvantaged position and is separate from short-term stock price volatility, which we are much less bothered by.

Golden Entertainment reported $404.3 million of cash and $678.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $200.9 million of EBITDA over the last 12 months, we view Golden Entertainment's 1.4x net-debt-to-EBITDA ratio as safe. We also see its $57.97 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Golden Entertainment's Q1 Results

This was a mixed quarter, with revenue beating but adjusted EBITDA missing. A one-time gain on sale helped the reported operating profit and EPS, although we'd highlight that this is not a fundamental driver. The stock is up 4.8% after reporting and currently trades at $32.1 per share.

Is Now The Time?

Golden Entertainment may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Golden Entertainment, we'll be cheering from the sidelines. Its revenue growth has been weak over the last five years, and analysts expect growth to deteriorate from here. And while its impressive operating margins show it has a highly efficient business model, the downside is its projected EPS for the next year is lacking. On top of that, its low free cash flow margins give it little breathing room.

While there are some things to like about Golden Entertainment and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $44.43 per share right before these results (compared to the current share price of $32.10).

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.