Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at GitLab (NASDAQ:GTLB) and the best and worst performers in the software development industry.

As legendary VC investor Marc Andreessen says, "Software is eating the world", and it touches virtually every industry. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming.

The 11 software development stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was in line.

Stocks--especially those trading at higher multiples--had a strong end of 2023, but this year has seen periods of volatility. Mixed signals about inflation have led to uncertainty around rate cuts. However, software development stocks have held steady amidst all this with share prices up 1.9% on average since the latest earnings results.

Best Q2: GitLab (NASDAQ:GTLB)

Founded as an open-source project in 2011, GitLab (NASDAQ:GTLB) is a leading software development tools platform.

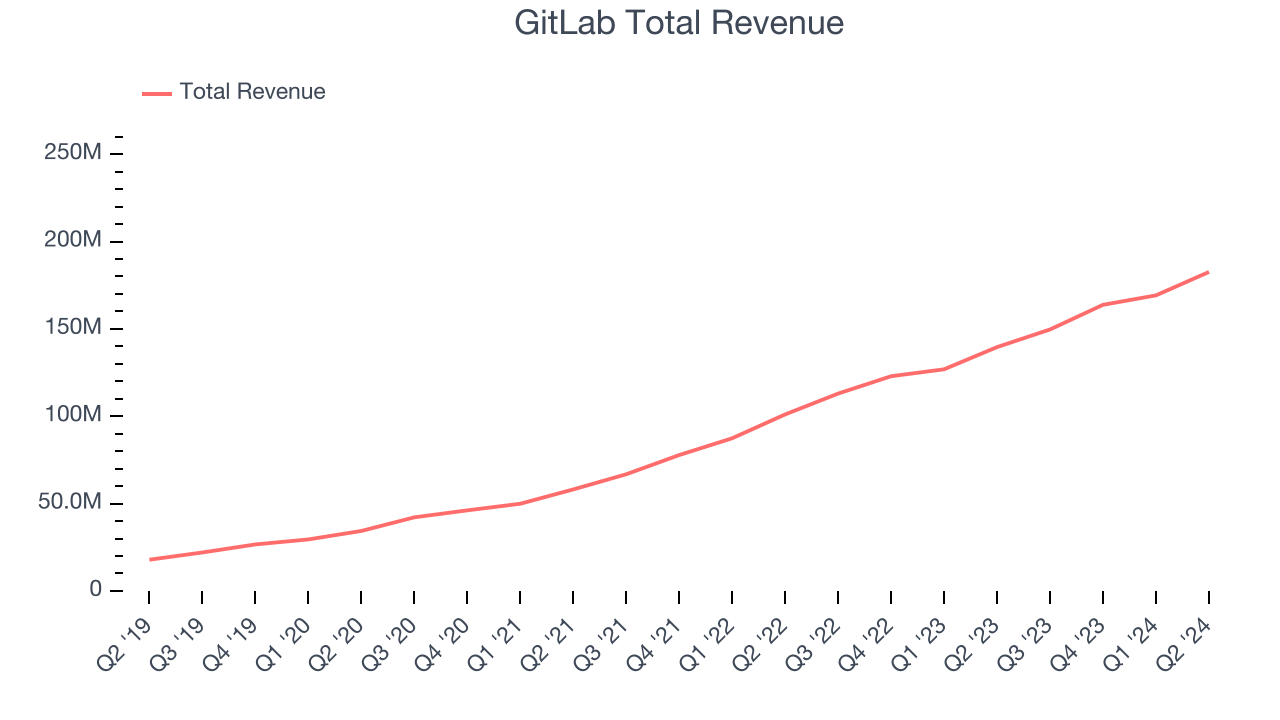

GitLab reported revenues of $182.6 million, up 30.8% year on year. This print exceeded analysts’ expectations by 3.1%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ billings estimates and a narrow beat of analysts’ ARR (annual recurring revenue) estimates.

“Organizations need to deliver software faster to accelerate performance and respond to intense competition,” said Sid Sijbrandij, GitLab CEO and co-founder.

GitLab achieved the fastest revenue growth and highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 23.4% since reporting and currently trades at $55.15.

PagerDuty (NYSE:PD)

Started by three former Amazon engineers, PagerDuty (NYSE:PD) is a software-as-a-service platform that helps companies respond to IT incidents fast and make sure that any downtime is minimized.

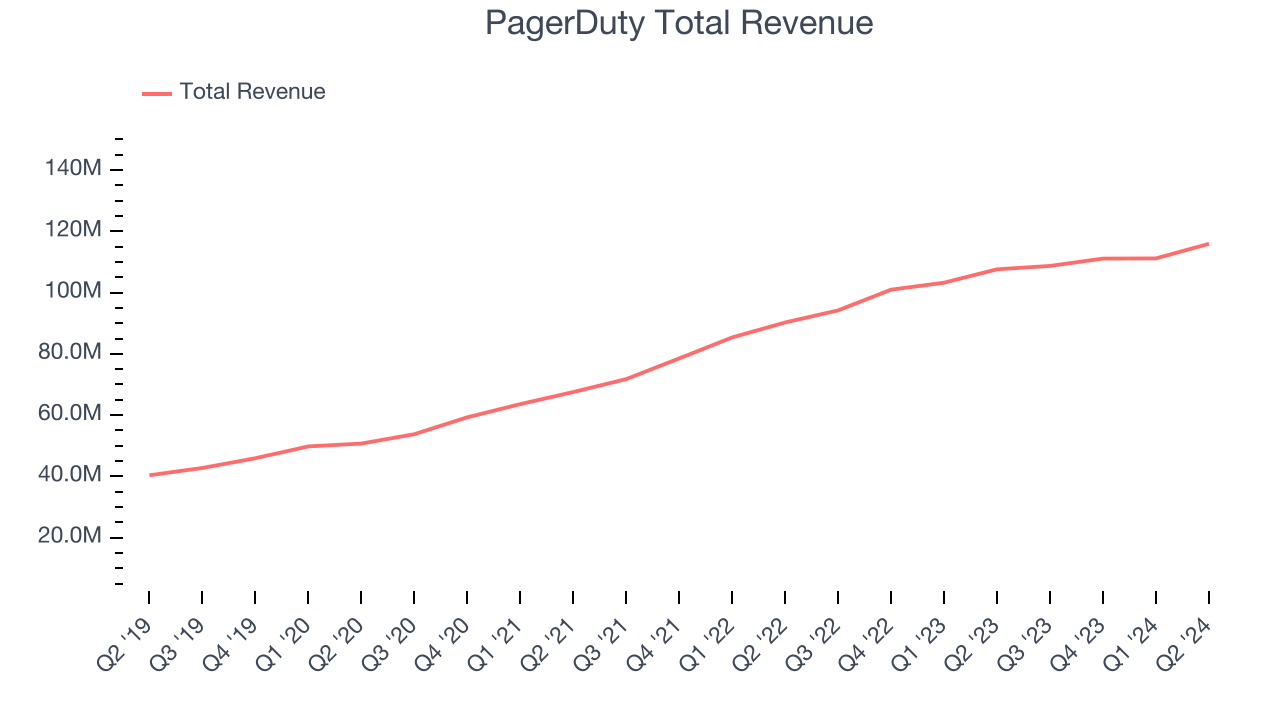

PagerDuty reported revenues of $115.9 million, up 7.7% year on year, in line with analysts’ expectations. The business performed better than its peers, but it was unfortunately a softer quarter with underwhelming revenue guidance for the next quarter and decelerating customer growth.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 3.2% since reporting. It currently trades at $17.69.

Is now the time to buy PagerDuty? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: JFrog (NASDAQ:FROG)

Named after the founders' affinity for frogs, JFrog (NASDAQ:FROG) provides a software-as-a-service platform that makes developing and releasing software easier and faster, especially for large teams.

JFrog reported revenues of $103 million, up 22.4% year on year, in line with analysts’ expectations. It was a softer quarter as it posted underwhelming revenue guidance for the next quarter and decelerating growth in large customers.

JFrog delivered the weakest performance against analyst estimates in the group. The company added 17 enterprise customers paying more than $100,000 annually to reach a total of 928. As expected, the stock is down 18.9% since the results and currently trades at $27.61.

Read our full analysis of JFrog’s results here.

Cloudflare (NYSE:NET)

Founded by two grad students of Harvard Business School, Cloudflare (NYSE:NET) is a software as a service platform that helps improve security, reliability and loading times of internet applications and websites.

Cloudflare reported revenues of $401 million, up 30% year on year. This number beat analysts’ expectations by 1.6%. Aside from that, it was a weak quarter as it recorded a miss of analysts’ billings estimates.

The stock is up 3.2% since reporting and currently trades at $76.81.

Read our full, actionable report on Cloudflare here, it’s free.

HashiCorp (NASDAQ:HCP)

Initially created as a research project at the University of Washington, HashiCorp (NASDAQ:HCP) provides software that helps companies operate their own applications in a multi-cloud environment.

HashiCorp reported revenues of $165.1 million, up 15.3% year on year. This result surpassed analysts’ expectations by 5.1%. Aside from that, it was a weak quarter with decelerating growth in large customers.

HashiCorp pulled off the biggest analyst estimates beat among its peers. The company added 16 enterprise customers paying more than $100,000 annually to reach a total of 934. The stock is flat since reporting and currently trades at $33.85.

Read our full, actionable report on HashiCorp here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.