Toy and entertainment company Hasbro (NASDAQ:HAS) announced better-than-expected results in Q1 CY2024, with revenue down 24.3% year on year to $757.3 million. It made a non-GAAP profit of $0.61 per share, improving from its profit of $0.01 per share in the same quarter last year.

Hasbro (HAS) Q1 CY2024 Highlights:

- Revenue: $757.3 million vs analyst estimates of $740.9 million (2.2% beat)

- EPS (non-GAAP): $0.61 vs analyst estimates of $0.28 (115% beat)

- Gross Margin (GAAP): 65.2%, up from 52.4% in the same quarter last year

- Free Cash Flow of $132 million, down 61.4% from the previous quarter

- Market Capitalization: $9.05 billion

Credited with the creation of toys such as Mr. Potato Head and the Rubik’s Cube, Hasbro (NASDAQ:HAS) is a global entertainment company offering a diverse range of toys, games, and multimedia experiences for children and families.

Hasbro's journey began in 1923, established by the Hassenfeld brothers as a small textile remnant company that sold school supplies. The company's transition into toy manufacturing was driven by a vision to create products that sparked imagination and joy in children. Eventually, Hasbro evolved into one of the world's largest toy makers.

Today, Hasbro provides an extensive portfolio of toys, board games, and digital gaming experiences that cater to a variety of ages and interests. The company offers everything from action figures and dolls to digital gaming platforms.

Hasbro generates revenue through product sales, licensing agreements, and digital gaming subscriptions. Its multifaceted business model includes partnerships with entertainment franchises, leveraging iconic characters and stories to create toys that complement various media. This synergy has created a unique value in the market, appealing to generations of consumers who cherish both nostalgia and modern media.

Toys and Electronics

The toys and electronics industry presents both opportunities and challenges for investors. Established companies often enjoy strong brand recognition and customer loyalty while smaller players can carve out a niche if they develop a viral, hit new product. The downside, however, is that success can be short-lived because the industry is very competitive: the barriers to entry for developing a new toy are low, which can lead to pricing pressures and reduced profit margins, and the rapid pace of technological advancements necessitates continuous product updates, increasing research and development costs, and shortening product life cycles for electronics companies. Furthermore, these players must navigate various regulatory requirements, especially regarding product safety, which can pose operational challenges and potential legal risks.

Competitors in the toy and entertainment sector include Mattel (NASDAQ:MAT), Funko (NASDAQ:FNKO), and Jakks Pacific (NASDAQ:JAKK).Sales Growth

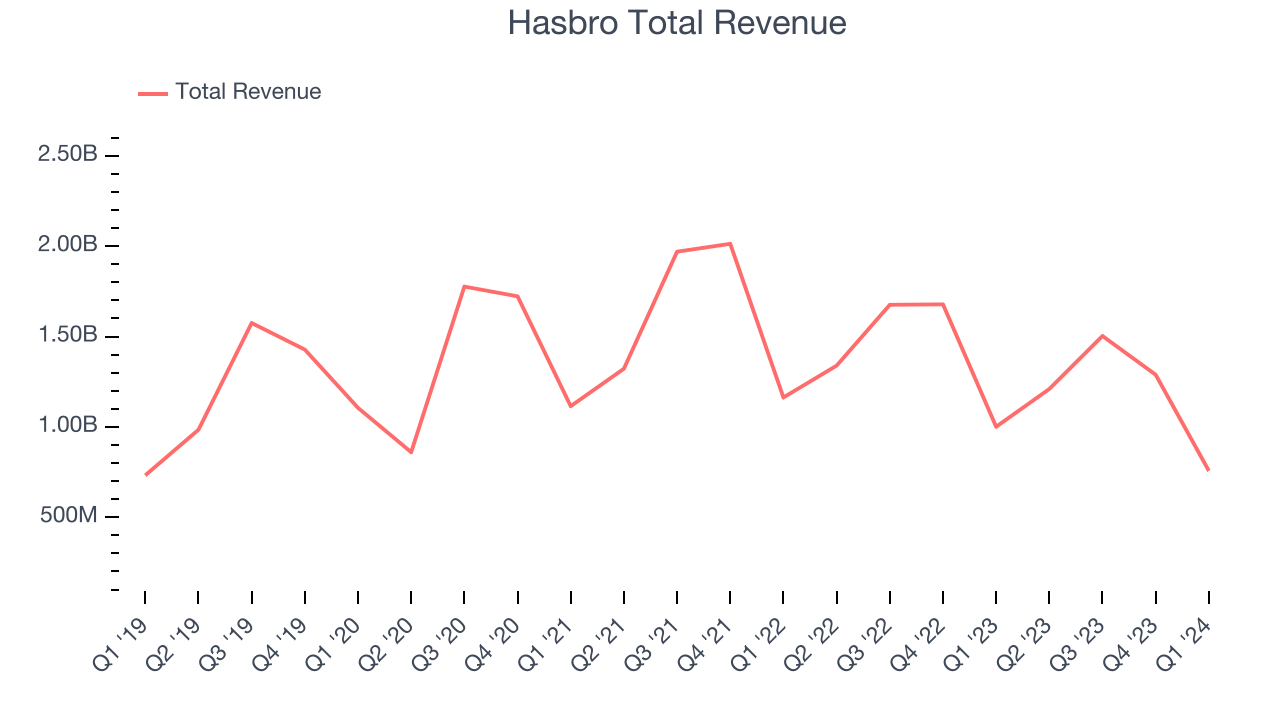

A company's long-term performance can indicate its business quality. Any business can enjoy short-lived success, but best-in-class ones sustain growth over many years. Hasbro's revenue was flat over the last five years.  Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Hasbro's recent history shows a reversal from its five-year trend as its revenue has shown annualized declines of 14.2% over the last two years.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Hasbro's recent history shows a reversal from its five-year trend as its revenue has shown annualized declines of 14.2% over the last two years.

We can better understand the company's revenue dynamics by analyzing its three most important segments: , , and , which are 54.5%, 3.7%, and 41.8% of revenue. Over the last two years, Hasbro's () and () revenues averaged year-on-year declines of 15.7% and 32.8% while () averaged 8.2% growth.

This quarter, Hasbro's revenue fell 24.3% year on year to $757.3 million but beat Wall Street's estimates by 2.2%. Looking ahead, Wall Street expects revenue to decline 12.6% over the next 12 months.

Operating Margin

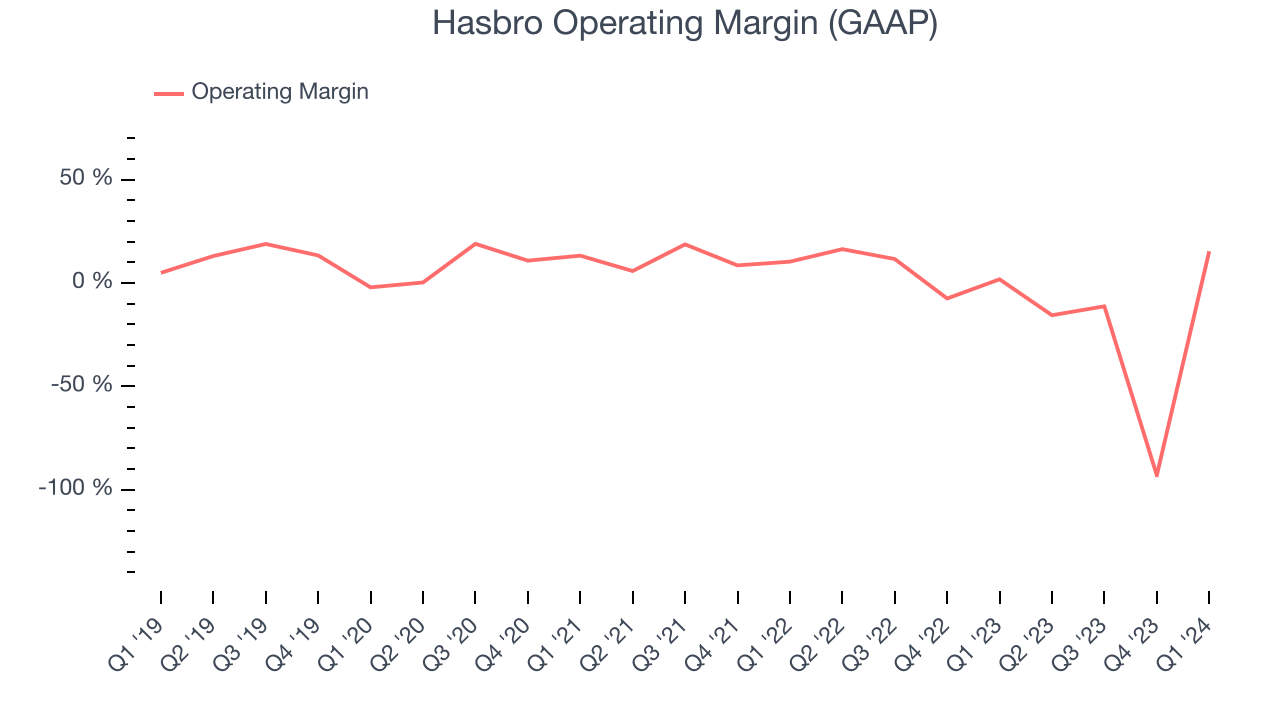

Operating margin is an important measure of profitability. It’s the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. Operating margin is also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Although Hasbro was profitable this quarter from an operational perspective, it's generally struggled when zooming out. Its high expenses have contributed to an average operating margin of negative 10.9% over the last two years. This performance isn't ideal as demand in the consumer discretionary sector is volatile. We prefer to invest in companies that can weather industry downturns through consistent profitability.

In Q1, Hasbro generated an operating profit margin of 15.3%, up 13.6 percentage points year on year.

Over the next 12 months, Wall Street expects Hasbro to become profitable. Analysts are expecting the company’s LTM operating margin of negative 30.3% to rise to positive 18%.EPS

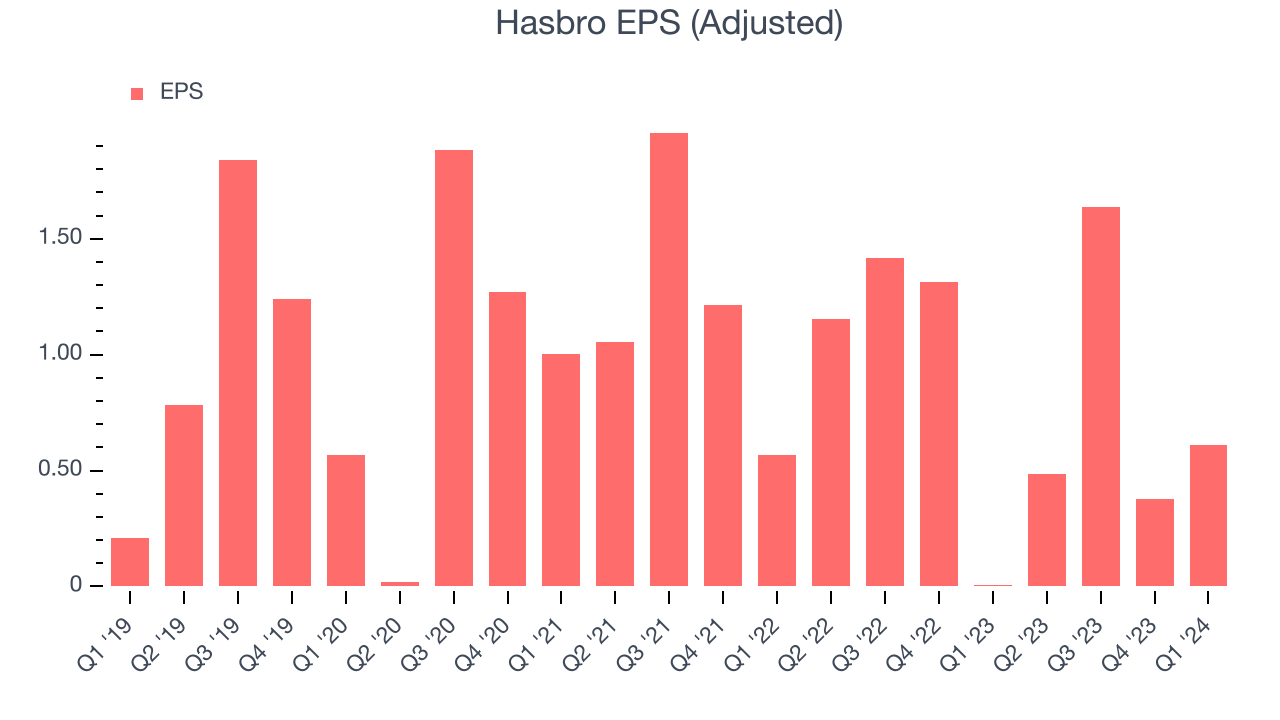

We track long-term historical earnings per share (EPS) growth for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Over the last five years, Hasbro's EPS dropped 25.7%, translating into 4.7% annualized declines. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends or consumer preferences. Consumer discretionary companies are particularly exposed to this, leaving a low margin of safety around the company (making the stock susceptible to large downward swings).

In Q1, Hasbro reported EPS at $0.61, up from $0.01 in the same quarter last year. This print easily cleared analysts' estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Hasbro to grow its earnings. Analysts are projecting its LTM EPS of $3.11 to climb by 7.9% to $3.35.

Cash Is King

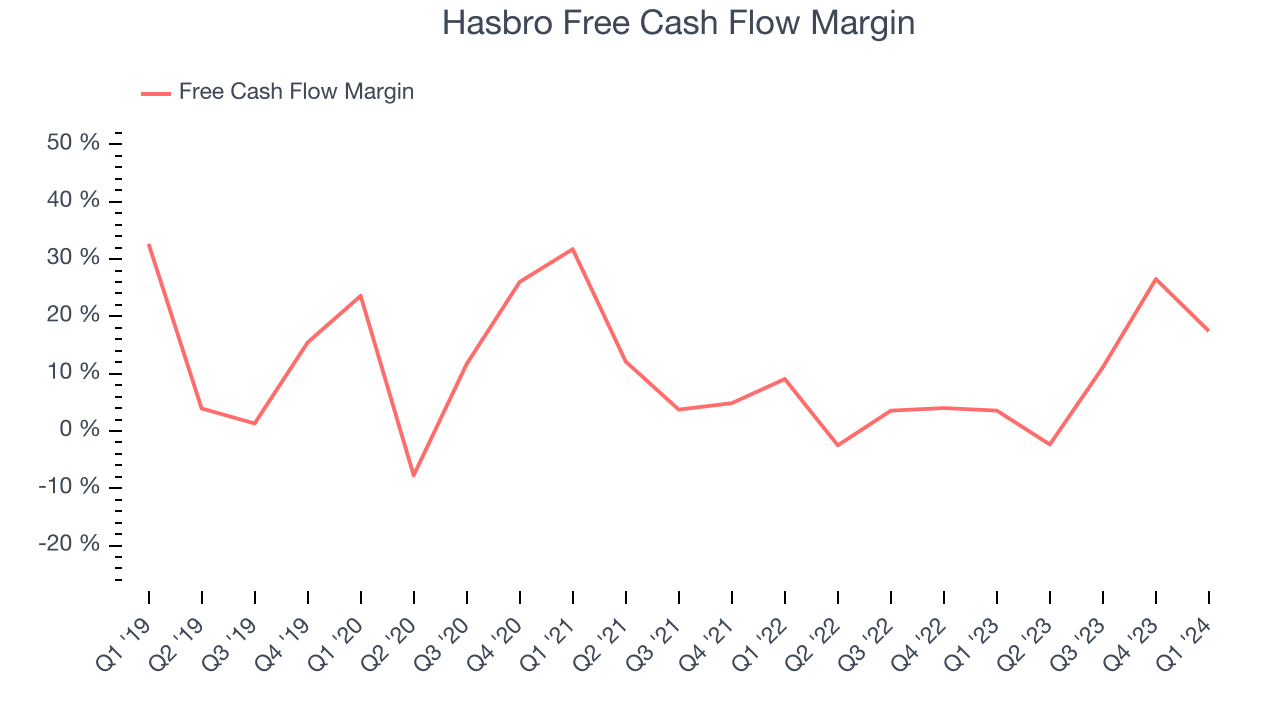

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Hasbro has shown mediocre cash profitability, putting it in a pinch as it gives the company limited opportunities to reinvest, pay down debt, or return capital to shareholders. Its free cash flow margin has averaged 7.1%, subpar for a consumer discretionary business.

Hasbro's free cash flow came in at $132 million in Q1, equivalent to a 17.4% margin and up 271% year on year.

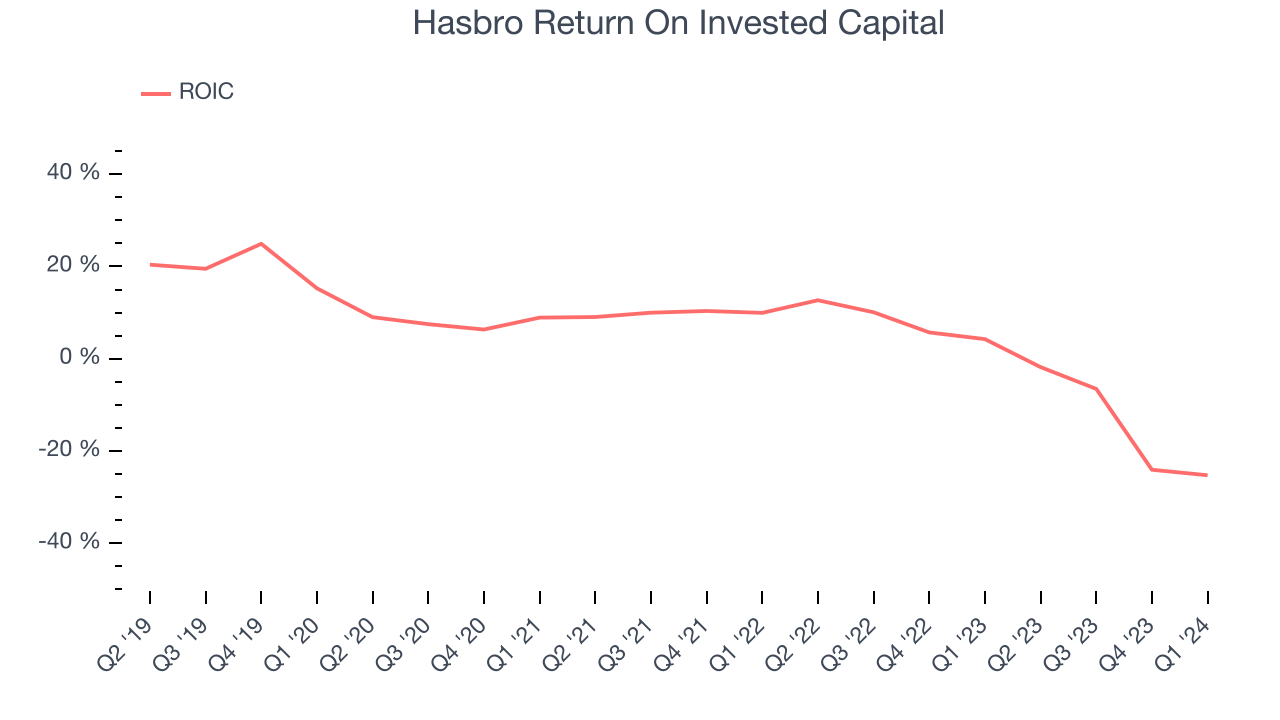

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Hasbro's five-year average return on invested capital was 2.6%, somewhat low compared to the best consumer discretionary companies that pump out 25%+. Its returns suggest it historically did a subpar job investing in profitable business initiatives.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Hasbro's ROIC significantly decreased over the last few years. Paired with its already low returns, these declines suggest the company's profitable business opportunities are few and far between.

Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly.

Hasbro reported $570.2 million of cash and $3.47 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company's debt level isn't too high and 2) that its interest payments are not excessively burdening the business.

With $783.5 million of EBITDA over the last 12 months, we view Hasbro's 3.7x net-debt-to-EBITDA ratio as safe. We also see its $153.2 million of annual interest expenses as appropriate. The company's profits give it plenty of breathing room, allowing it to continue investing in new initiatives.

Key Takeaways from Hasbro's Q1 Results

We were impressed by how significantly Hasbro blew past analysts' EPS expectations this quarter. We were also excited its operating margin outperformed Wall Street's estimates. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. Investors were likely expecting more, however, and the stock is down 1.8% after reporting, trading at $63.81 per share.

Is Now The Time?

Hasbro may have had a good quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for all companies serving consumers, but in the case of Hasbro, we'll be cheering from the sidelines. Its revenue growth has been weak over the last five years, and analysts expect growth to deteriorate from here. On top of that, its relatively low ROIC suggests it has historically struggled to find compelling business opportunities, and its operating margins reveal poor profitability compared to other consumer discretionary companies.

Hasbro's price-to-earnings ratio based on the next 12 months is 19.4x. While we've no doubt one can find things to like about Hasbro, we think there are better opportunities elsewhere in the market. We don't see many reasons to get involved at the moment.

Wall Street analysts covering the company had a one-year price target of $60.96 per share right before these results (compared to the current share price of $63.81), implying they didn't see much short-term potential in Hasbro.

To get the best start with StockStory, check out our most recent stock picks, and then sign up for our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.