Hasbro has been treading water for the past six months, recording a small return of 1.2% while holding steady at $57.50. The stock also fell short of the S&P 500’s 7% gain during that period.

Is there a buying opportunity in Hasbro, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.We're sitting this one out for now. Here are three reasons why there are better opportunities than HAS and a stock we'd rather own.

Why Do We Think Hasbro Will Underperform?

Credited with the creation of toys such as Mr. Potato Head and the Rubik’s Cube, Hasbro (NASDAQ:HAS) is a global entertainment company offering a diverse range of toys, games, and multimedia experiences for children and families.

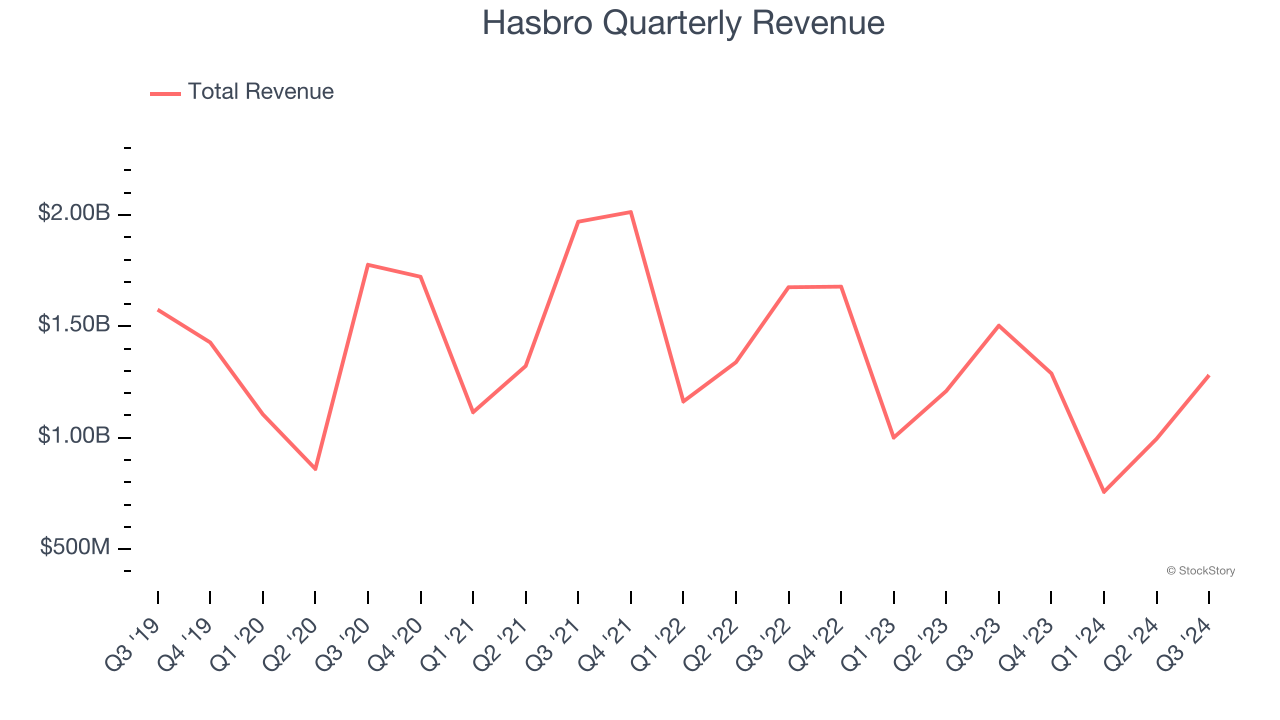

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Hasbro’s demand was weak and its revenue declined by 1.6% per year. This fell short of our benchmarks and is a sign of poor business quality.

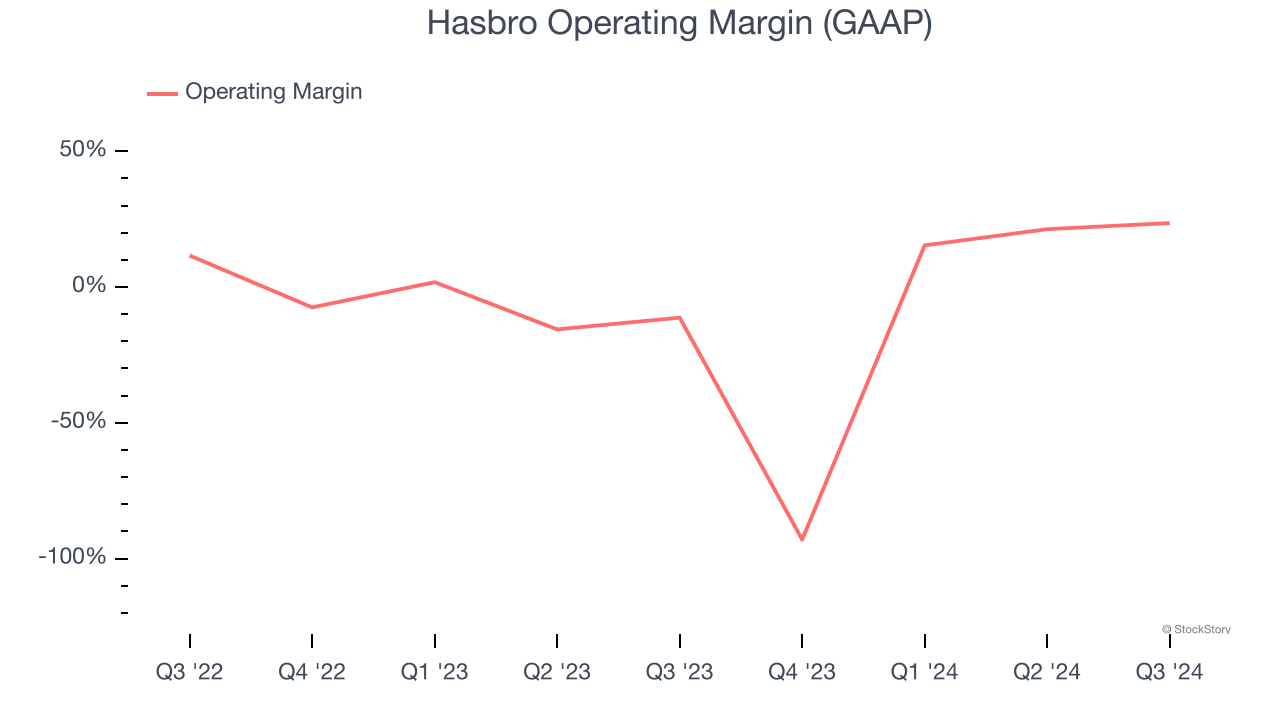

2. Operating Losses Sound the Alarms

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Hasbro’s operating margin has been trending down over the last 12 months and averaged negative 10.6% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

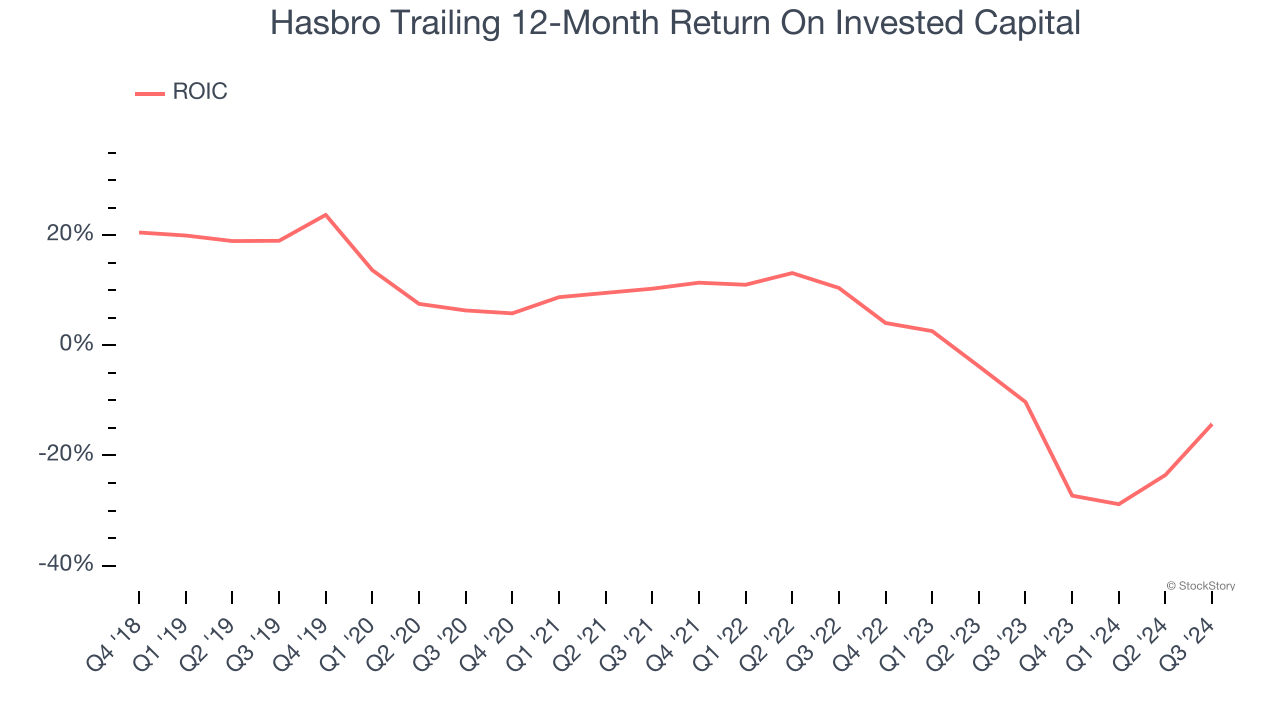

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Unfortunately, Hasbro’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

We see the value of companies helping consumers, but in the case of Hasbro, we’re out. With its shares trailing the market in recent months, the stock trades at 13.2× forward price-to-earnings (or $57.50 per share). This valuation multiple is fair, but we don’t have much confidence in the company. There are better stocks to buy right now. We’d recommend looking at Meta, a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Hasbro

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.