Healthcare software provider Health Catalyst (NASDAQ:HCAT) reported results ahead of analysts' expectations in Q2 CY2024, with revenue up 3.7% year on year to $75.9 million. On the other hand, next quarter's revenue guidance of $76 million was less impressive, coming in 2.5% below analysts' estimates. It made a non-GAAP profit of $0.12 per share, improving from its profit of $0.05 per share in the same quarter last year.

Is now the time to buy Health Catalyst? Find out by accessing our full research report, it's free.

Health Catalyst (HCAT) Q2 CY2024 Highlights:

- Revenue: $75.9 million vs analyst estimates of $75.02 million (1.2% beat)

- EPS (non-GAAP): $0.12 vs analyst estimates of $0.08 ($0.04 beat)

- Revenue Guidance for Q3 CY2024 is $76 million at the midpoint, below analyst estimates of $77.93 million

- The company reconfirmed its revenue guidance for the full year of $308 million at the midpoint

- Gross Margin (GAAP): 47.2%, in line with the same quarter last year

- Free Cash Flow was -$2.44 million, down from $7.53 million in the previous quarter

- Market Capitalization: $350.1 million

“For the second quarter of 2024, I am pleased by our strong financial results, including total revenue of $75.9 million and Adjusted EBITDA of $7.5 million, with these results exceeding the mid-point of our quarterly guidance on each metric. I am also pleased with our bookings performance through Q2 2024, especially as it relates to our net new Platform Subscription Clients. In the first half of 2024 we signed more net new Platform Subscription Clients than in all of 2023, and our updated expectations of low-20s net new Platform Subscription Clients would represent the strongest year in the company’s history for this metric.” said Dan Burton, CEO of Health Catalyst.

Founded by healthcare professionals Tom Burton and Steve Barlow in 2008, Health Catalyst (NASDAQ:HCAT) provides data and analytics technology to healthcare organizations, enabling them to improve care and lower costs.

Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Sales Growth

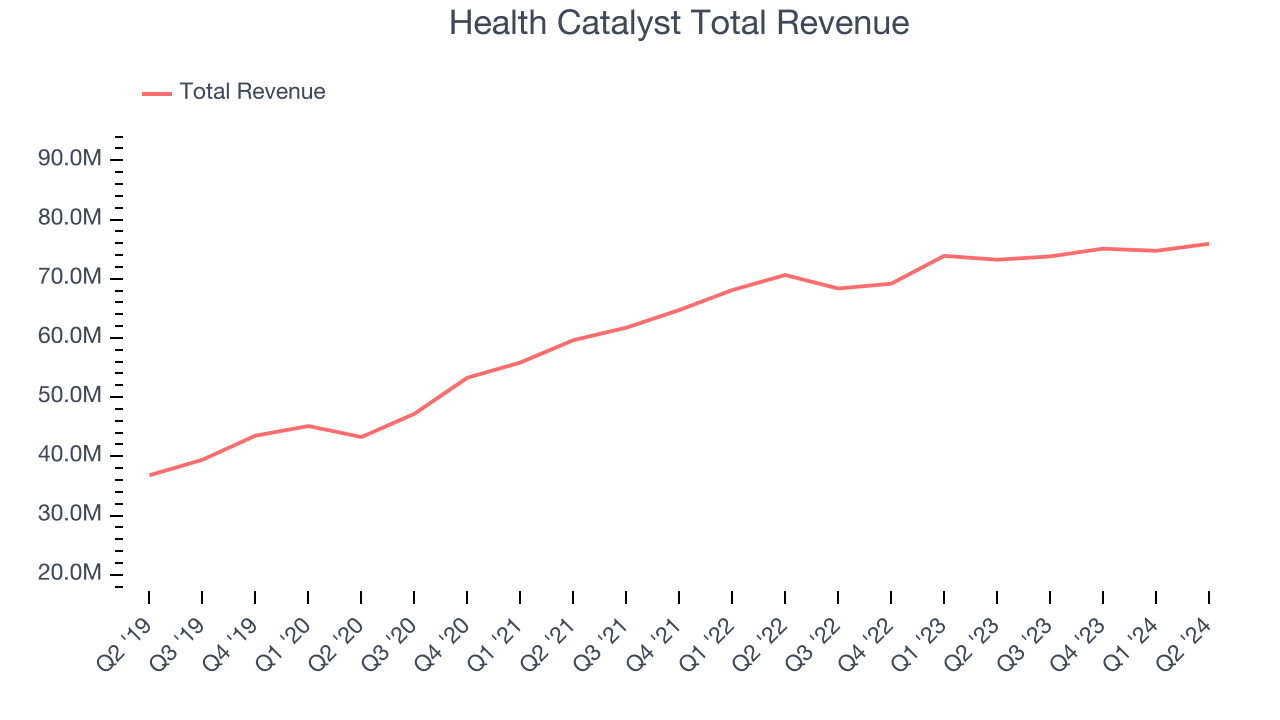

As you can see below, Health Catalyst's 11.5% annualized revenue growth over the last three years has been sluggish, and its sales came in at $75.9 million this quarter.

Health Catalyst's quarterly revenue was only up 3.7% year on year, which might disappoint some shareholders. However, its revenue increased $1.18 million quarter on quarter, a strong improvement from the $361,000 decrease in Q1 CY2024. This is a sign of acceleration of growth and very nice to see indeed.

Next quarter's guidance suggests that Health Catalyst is expecting revenue to grow 3% year on year to $76 million, slowing down from the 7.9% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 8.6% over the next 12 months before the earnings results announcement.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

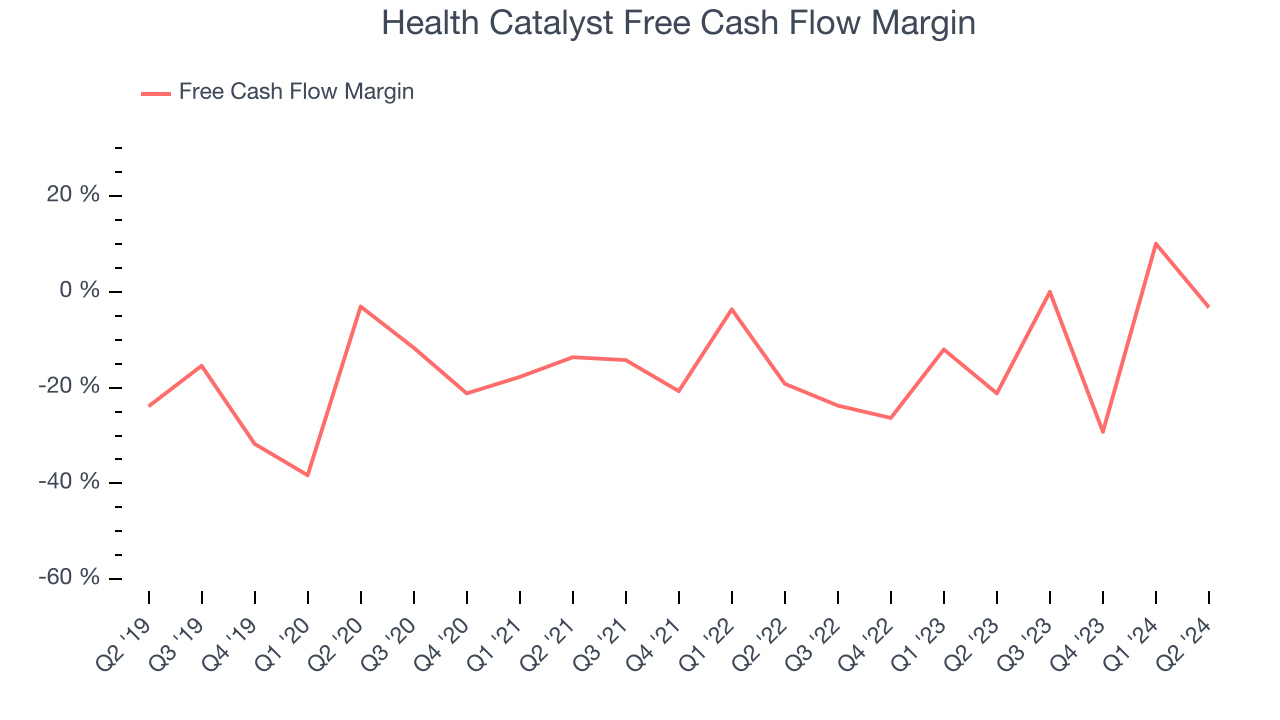

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Health Catalyst's demanding reinvestments have consumed many resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 5.6%, poor for a software business.

Health Catalyst burned through $2.44 million of cash in Q2, equivalent to a negative 3.2% margin. The company's cash burn decreased meaningfully year on year while its free cash flow margin climbed 18 percentage points. This relationship shows Health Catalyst's management team brought in more revenue this quarter despite spending less cash - a mark of higher short-term efficiency.

Key Takeaways from Health Catalyst's Q2 Results

It was encouraging to see Health Catalyst narrowly top analysts' revenue expectations this quarter. On the other hand, its revenue guidance for next quarter missed analysts' expectations and its gross margin shrunk. This quarter featured some positives but overall could have been better. The stock traded up 4.4% to $5.74 immediately following the results.

So should you invest in Health Catalyst right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.