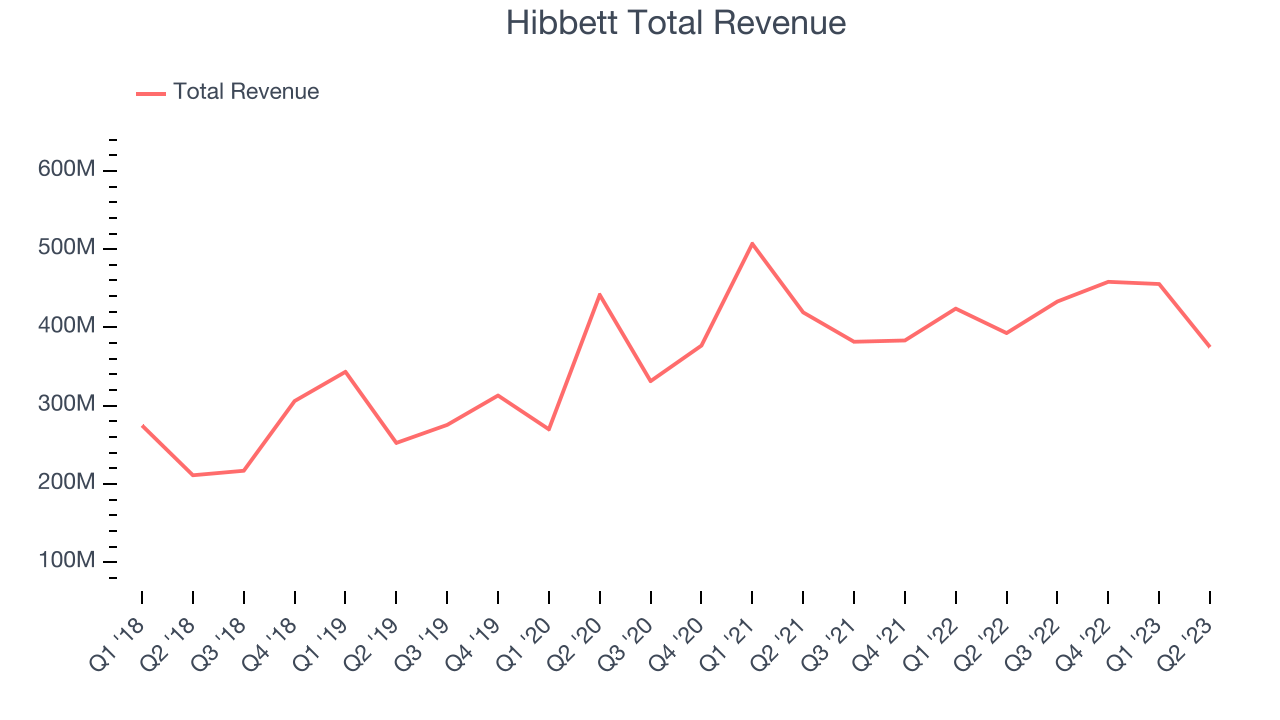

Athletic apparel and footwear retailer Hibbett (NASDAQ:HIBB) fell short of analysts' expectations in Q2 FY2024, with revenue down 4.56% year on year to $374.9 million. The company also reiterated its full-year guidance. Hibbett made a GAAP profit of $10.9 million, down from its profit of $24.7 million in the same quarter last year.

Is now the time to buy Hibbett? Find out by accessing our full research report, it's free.

Hibbett (HIBB) Q2 FY2024 Highlights:

- Revenue: $374.9 million vs analyst estimates of $376.1 million (small miss)

- EPS: $0.85 vs analyst estimates of $0.73 (16.2% beat)

- Gross Margin (GAAP): 32.8%, down from 34.4% in the same quarter last year

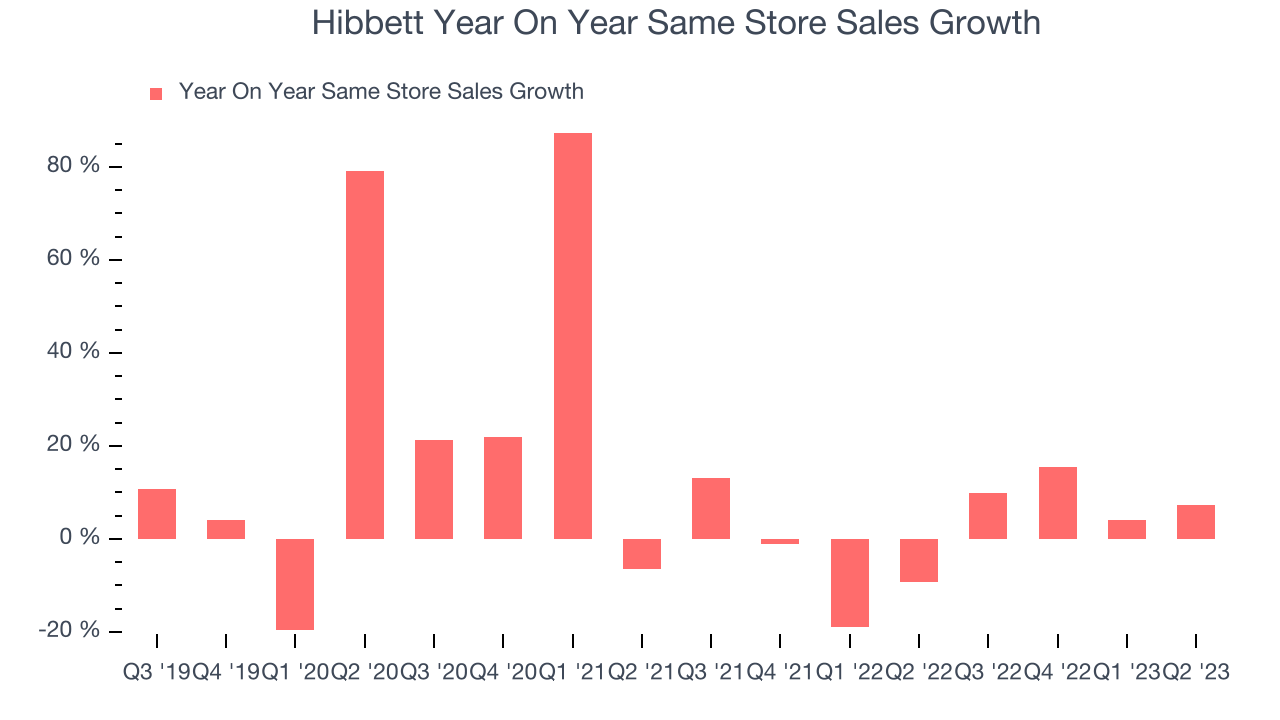

- Same-Store Sales were down 7.3% year on year

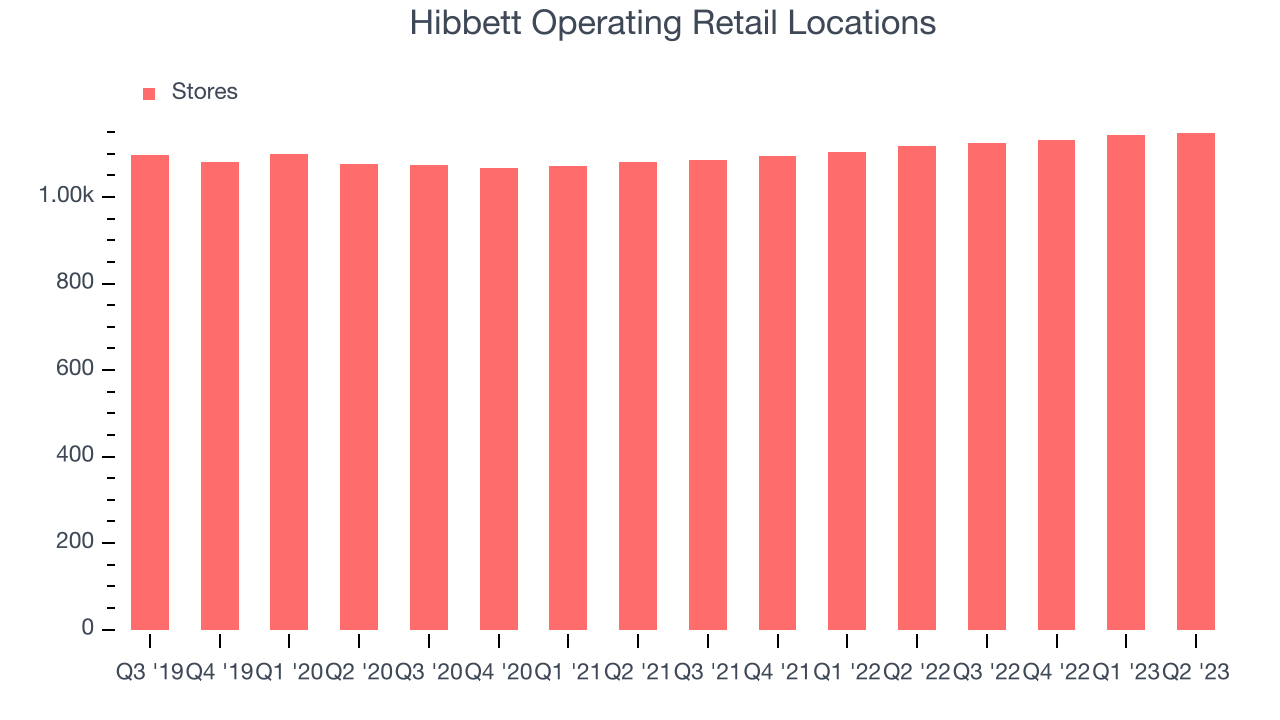

- Store Locations: 1,148 at quarter end, increasing by 31 over the last 12 months

Mike Longo, President and Chief Executive Officer, stated, “We are pleased with our performance for the second quarter of Fiscal 2024. Our business model focuses on providing an exceptional consumer experience in underserved markets and produced solid financial results despite a challenging retail environment. Our sales for the second quarter were supported by a strong start to the busy back-to-school season and we also benefited from a positive customer response to new product launches during the quarter. Our strong relationships with valued brand partners continue to provide us the ability to offer a compelling product assortment and as a result, we believe we continue to gain market share”.

With a focus on small and mid-sized markets, Hibbett (NASDAQ:HIBB) is a specialty retailer that sells athletic apparel and footwear as well as select sports equipment.

Apparel and footwear was once a category thought to be relatively safe from major e-commerce penetration because of the need to try on, touch, and feel products, but the category is now meaningfully transacted online. Everyone still needs clothes and shoes to go outside unless they want some curious (or horrified) looks. But this ongoing digitization is forcing apparel and footwear retailers–that once only had brick-and-mortar stores–to respond with omnichannel offerings. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stagnate, so the evolution of clothing and shoes sellers marches on.

Sales Growth

Hibbett is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 11.4% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was impressive as it opened new stores and grew sales at existing, established stores.

This quarter, Hibbett reported a rather uninspiring 4.56% year-on-year revenue decline, missing analysts' expectations.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

The number of stores a retailer operates is a major determinant of how much it can sell, and its growth is a critical driver of how quickly company-level sales can grow.

When a retailer like Hibbett is opening new stores, it usually means that demand is greater than supply, and in turn, it's investing for growth. Hibbett's store count increased by 31 locations, or 2.78%, over the last 12 months to 1,148 total retail locations in the most recently reported quarter.

Over the last two years, the company has generally opened new stores and averaged 2.96% annual growth in its physical footprint, which is decent and on par with the broader sector. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for retailers.

Hibbett's demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company's same-store sales have grown by 2.59% year on year. With positive same-store sales growth amid an increasing physical footprint of stores, Hibbett is reaching more customers and growing sales.

In the latest quarter, Hibbett's same-store sales rose 7.3% year on year. This decrease was another deceleration on top of the 9.2% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Hibbett's Q2 Results

With a market capitalization of $469.8 million and more than $33.1 million in cash on hand, Hibbett can continue prioritizing growth.

We enjoyed seeing Hibbett exceed analysts' EPS expectations this quarter. That really stood out as a positive in these results. On the other hand, the company missed analysts' revenue expectations, driven by underperformance in same-store sales growth, and its gross margin dropped due to higher promotional activity across both footwear and apparel. At face value, this could signal that demand will deteriorate even further in the future, but Hibbett reiterated its full-year guidance during the quarter. Overall, the results could have been better. The stock is down 1% after reporting and currently trades at $38.76 per share.

So should you invest in Hibbett right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.