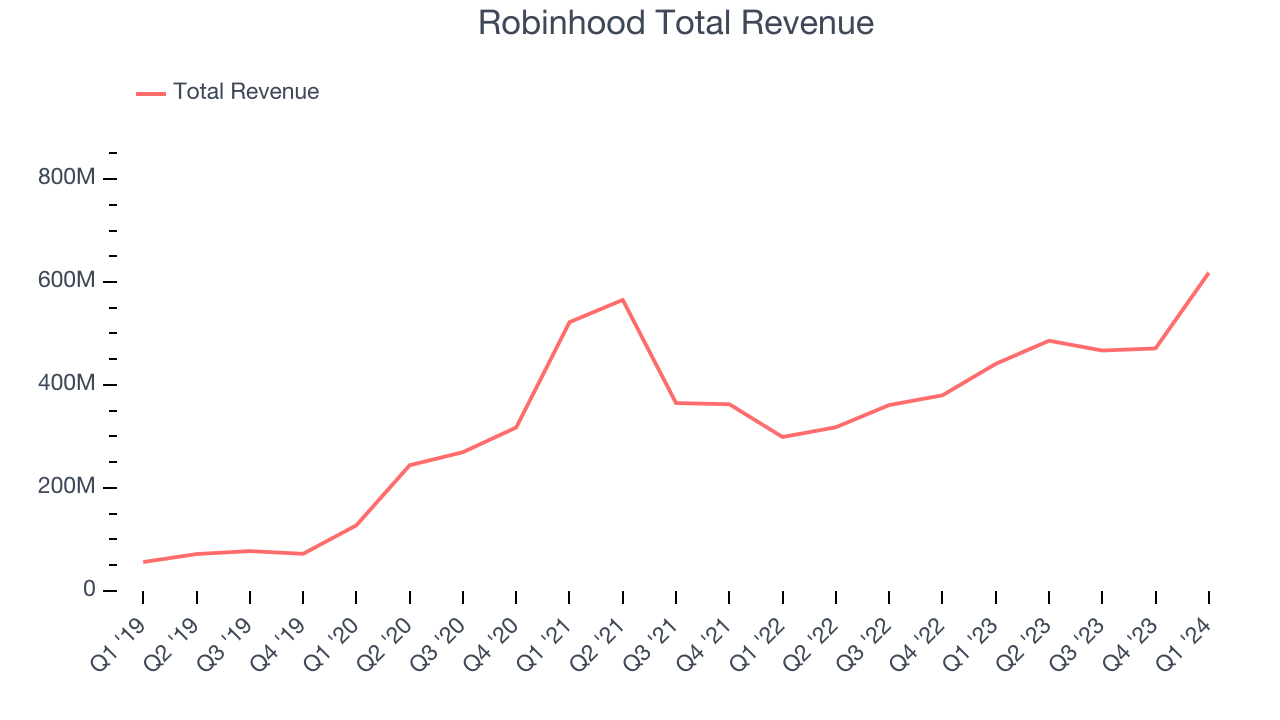

Financial services company Robinhood (NASDAQ:HOOD) announced better-than-expected results in Q1 CY2024, with revenue up 40.1% year on year to $618 million. It made a GAAP profit of $0.18 per share, improving from its loss of $0.57 per share in the same quarter last year.

Robinhood (HOOD) Q1 CY2024 Highlights:

- Revenue: $618 million vs analyst estimates of $555 million (11.4% beat)

- EPS: $0.18 vs analyst estimates of $0.06 ($0.12 beat)

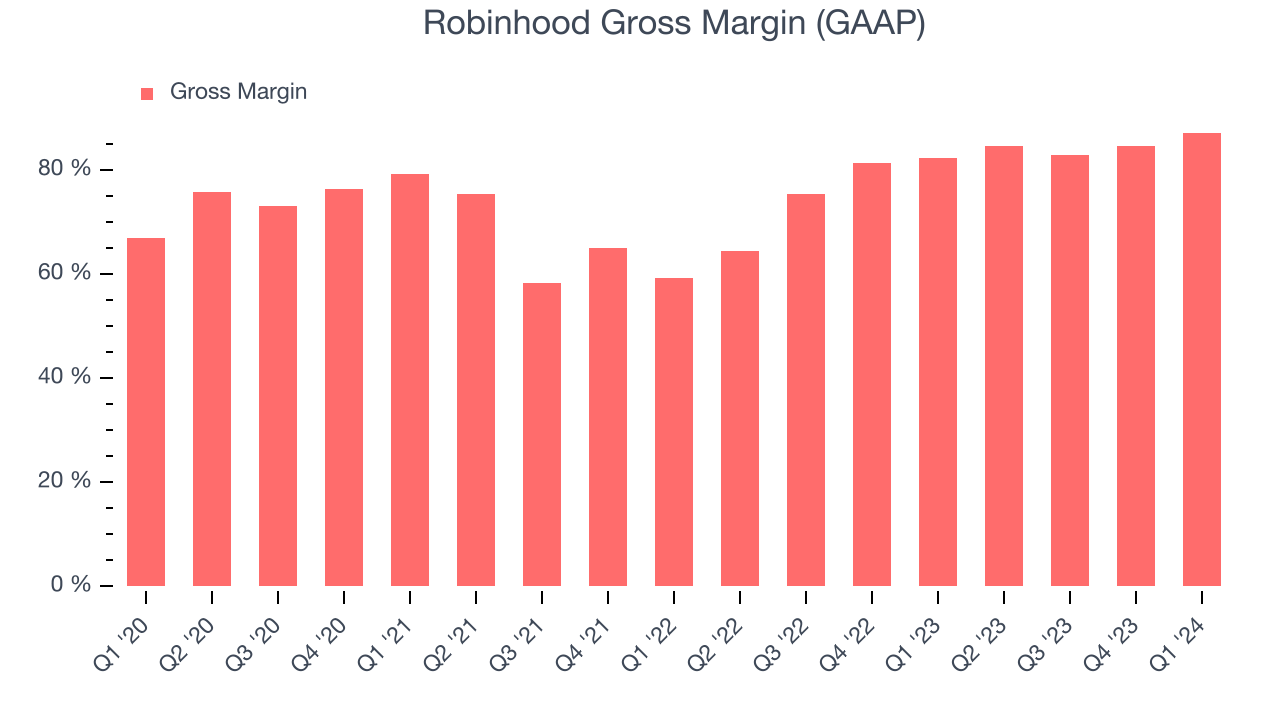

- Gross Margin (GAAP): 87.2%, up from 82.3% in the same quarter last year

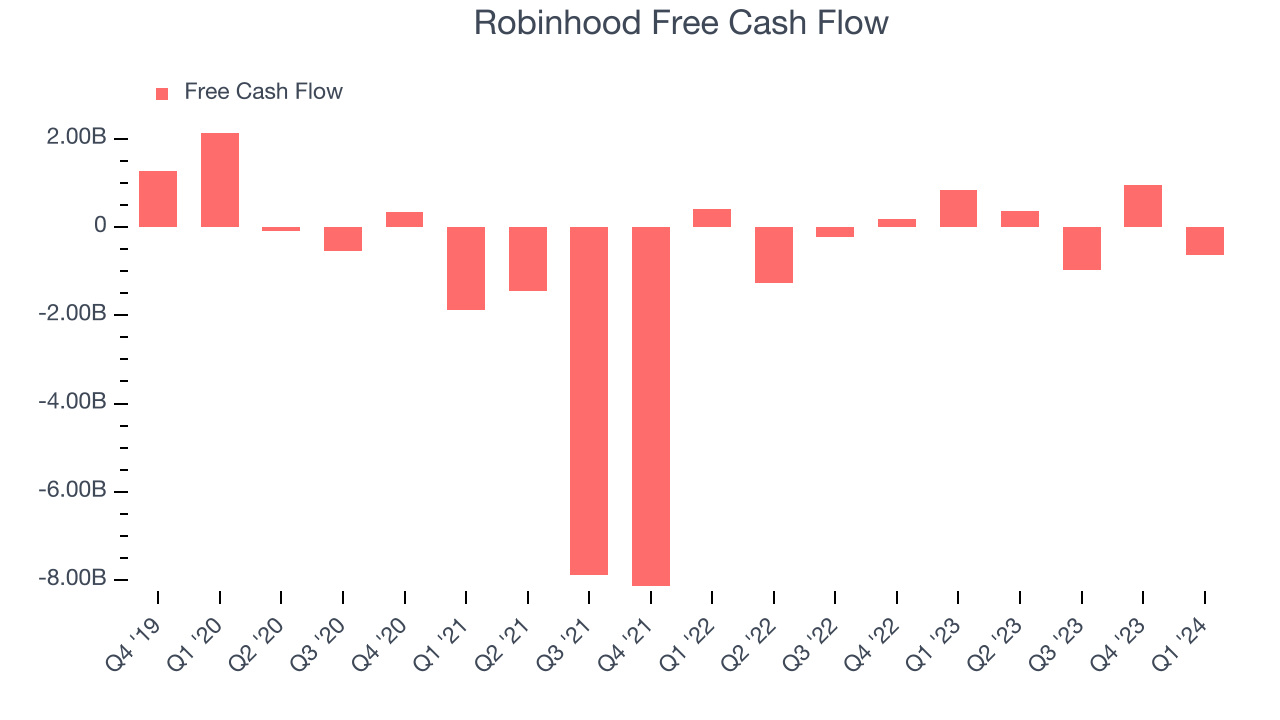

- Free Cash Flow was -$632 million, down from $954 million in the previous quarter

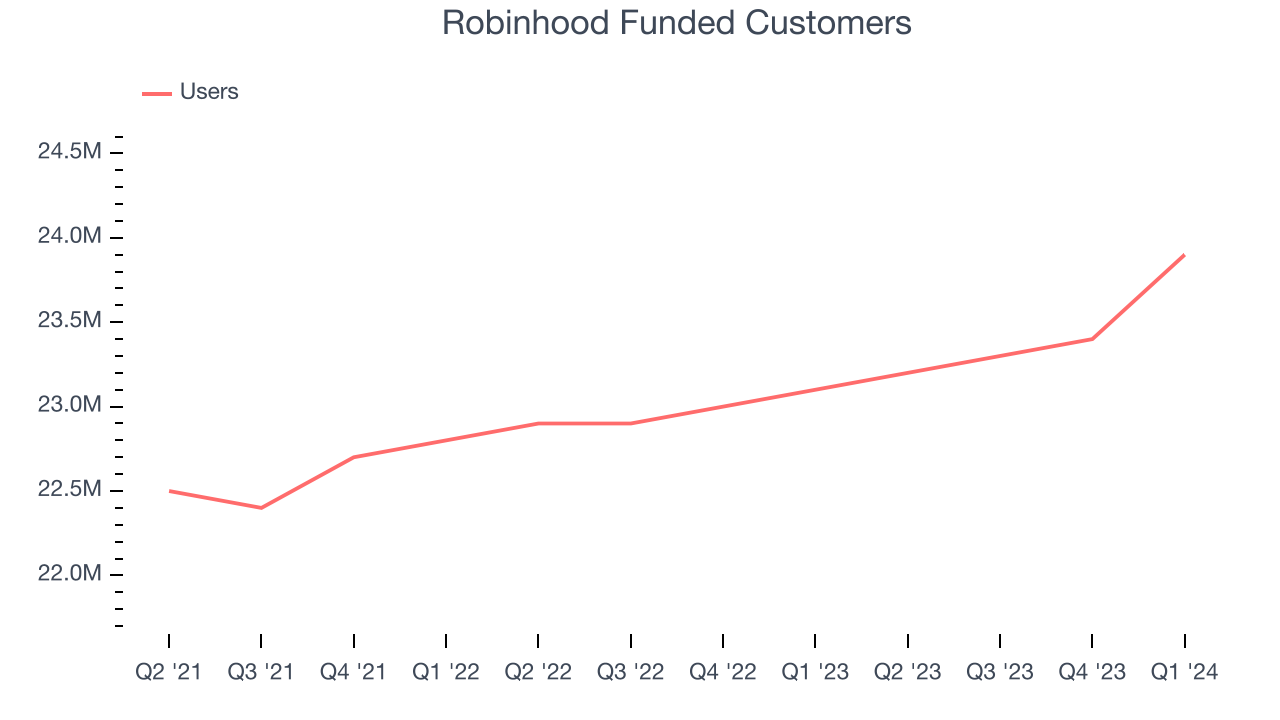

- Funded Customers: 23.9 million, up 800,000 year on year

- Market Capitalization: $15.81 billion

With a mission to democratize finance, Robinhood (NASDAQ:HOOD) is an online consumer finance platform known for its commission-free stock and crypto trading.

Historically, the average person would pay high broker fees to place buy and sell orders. Robinhood’s founders, Vlad Tenev and Baiju Bhatt (mathematicians and roommates at Stanford), sought to lower the barriers to entry by pioneering commission-free trading.

Commission-free trading uses algorithms to take customer orders and route them to market makers. In exchange for sourcing the trade, the router takes a percentage of the market maker's profit. This is called payment for order flow, and it is a huge chunk of Robinhood’s trading revenue.

Today, Robinhood not only generates revenue from payment for order flow but also interest on margin trading loans, interest on uninvested cash, and subscription fees for Robinhood Gold. Robinhood Gold costs $5 per month and gives users access to premium features such as 24/7 trading, cheaper margin loans, boosted interest rates on uninvested cash, and research reports. Because it's a software company, Robinhood has fewer employees and a more efficient cost base than its legacy competitors.

Robinhood's long-term strategy is to increase its users and assets under custody by becoming a one-stop shop for consumer finance. It plans to achieve this by rolling out products like retirement accounts and credit cards. Investors under the age of 35 comprise a majority of Robinhood's user base as it has no account minimums and initially built its products exclusively for mobile devices.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Robinhood’s competitors include Charles Schwab (NYSE:SCHW), Fidelity (NYSE:FNF), Interactive Brokers (NASDAQ:IBKR), Coinbase (NASDAQ:COIN), and private companies M1 Finance and Webull.Sales Growth

Robinhood's revenue growth over the last three years has been strong, averaging 24.3% annually. This quarter, Robinhood beat analysts' estimates and reported impressive 40.1% year-on-year revenue growth.

Ahead of the earnings results, analysts were projecting sales to grow 16.3% over the next 12 months.

Usage Growth

As an online marketplace, Robinhood generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, Robinhood's users, a key performance metric for the company, grew 1.9% annually to 23.9 million. This is one of the lowest rates of growth in the consumer internet sector.

In Q1, Robinhood added 800,000 users, translating into 3.5% year-on-year growth.

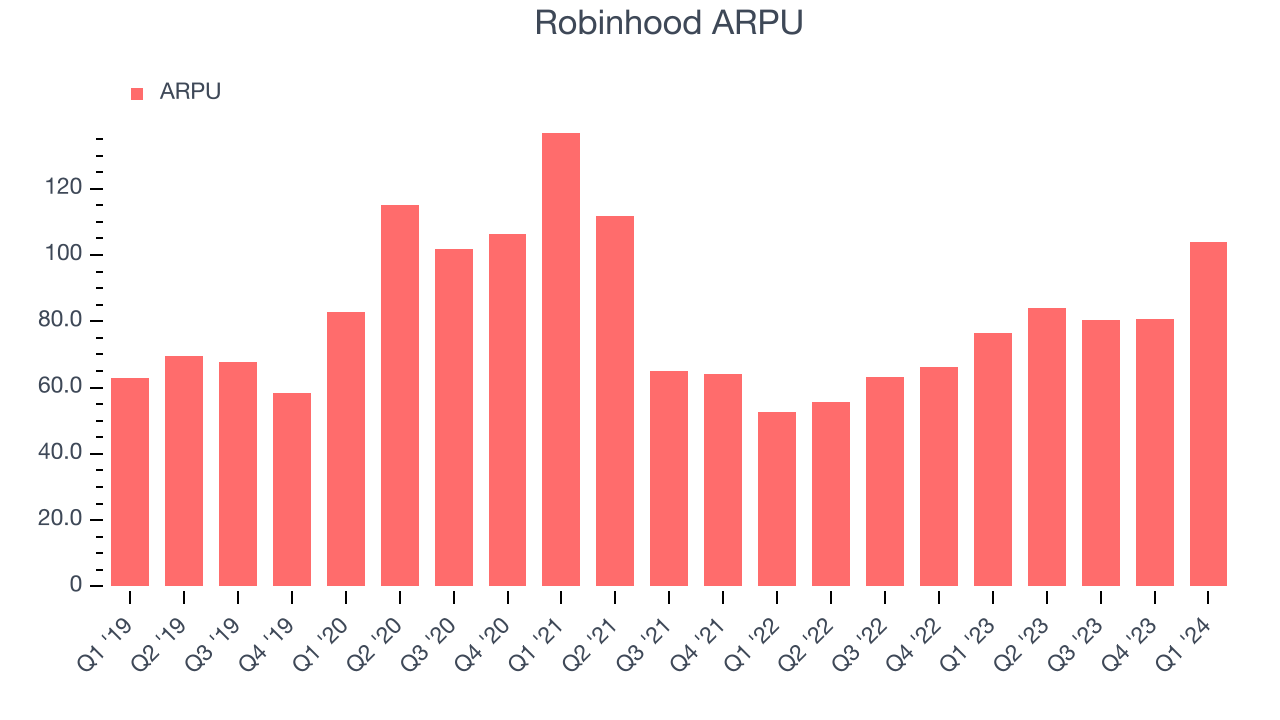

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Robinhood because it measures how much the company earns in transaction fees from each user. Furthermore, ARPU gives us unique insights as it's a function of a user's average order size and Robinhood's take rate, or "cut", on each order.

Robinhood's ARPU growth has been excellent over the last two years, averaging 16.4%. The company's ability to increase prices while growing its users demonstrates its platform's value, as its users are spending significantly more than last year. This quarter, ARPU grew 35.9% year on year to $104 per user.

Pricing Power

A company's gross profit margin has a major impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors may ultimately determine the winner in a competitive market, making it a critical metric to track for the long-term investor.

Robinhood's gross profit margin, which tells us how much money the company gets to keep after covering the base cost of its products and services, came in at 87.2% this quarter, up 4.9 percentage points year on year.

For online marketplaces like Robinhood, these aforementioned costs typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification. After paying for these expenses, Robinhood had $0.87 for every $1 in revenue to invest in marketing, talent, and the development of new products and services.

Robinhood's gross margins have been trending up over the last 12 months, averaging 85%. Its margins are some of the highest in the consumer internet sector, enabling it to fund large investments in product and marketing during periods of rapid growth to stay one step ahead of the competition.

User Acquisition Efficiency

Consumer internet businesses like Robinhood grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

Robinhood is extremely efficient at acquiring new users, spending only 8.9% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and customer acquisition advantages from scale, giving Robinhood the freedom to invest its resources into new growth initiatives while maintaining optionality.

Profitability & Free Cash Flow

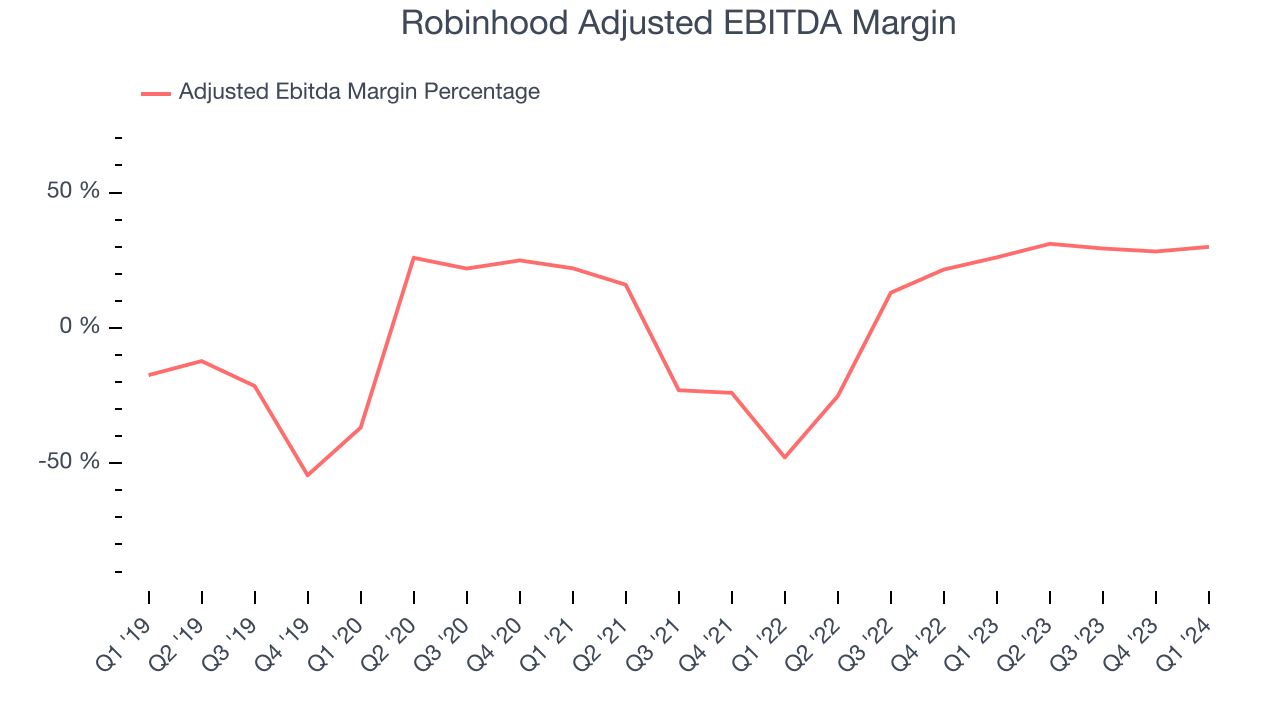

Investors frequently analyze operating income to understand a business's core profitability. Similar to operating income, adjusted EBITDA is the most common profitability metric for consumer internet companies because it removes various one-time or non-cash expenses, offering a more normalized view of a company's profit potential.

Robinhood's EBITDA was $185 million this quarter, translating into a 29.9% margin. Additionally, Robinhood has demonstrated extremely high profitability over the last four quarters, with average EBITDA margins of 29.7%.

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Robinhood burned through $632 million in Q1, with cash flow turning negative year on year.

Robinhood has burned through $286 million of cash over the last 12 months, resulting in a negative 14% free cash flow margin. This low FCF margin stems from Robinhood's need to reinvest in its business to fuel revenue growth.

Key Takeaways from Robinhood's Q1 Results

We were impressed by how significantly Robinhood blew past analysts' revenue and EPS expectations this quarter, driven by better-than-expected transaction volumes, net deposits, account additions, and Gold subscribers. We note it produced negative free cash flow due to some changes in working capital, but we see this as a short-term fluctuation on par with the normal course of business.

During the quarter, Robinhood announced it would launch a credit card product later this year, expanding its market opportunity.

Zooming out, we think this was an impressive quarter that should delight shareholders. The stock is up 4.9% after reporting and currently trades at $18.74 per share.

Is Now The Time?

When considering an investment in Robinhood, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

We think Robinhood is a good business. We'd expect growth rates to moderate from here, but its revenue growth has been good over the last three years. And while its users have declined, the good news is its impressive gross margins are a wonderful starting point for the overall profitability of the business. On top of that, its user acquisition efficiency is best in class.

At the moment, Robinhood trades at 19.5x next 12 months EV-to-EBITDA. There's definitely a lot of things to like about Robinhood and looking at the consumer internet landscape right now, it seems that the company trades at a pretty interesting price.

Wall Street analysts covering the company had a one-year price target of $18.97 per share right before these results (compared to the current share price of $18.74).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.