Apple device management company, Jamf (NASDAQ:JAMF) beat analysts' expectations in Q4 FY2023, with revenue up 15.6% year on year to $150.6 million. On the other hand, next quarter's revenue guidance of $149 million was less impressive, coming in 1.2% below analysts' estimates. It made a non-GAAP profit of $0.13 per share, improving from its profit of $0.06 per share in the same quarter last year.

Jamf (JAMF) Q4 FY2023 Highlights:

- Revenue: $150.6 million vs analyst estimates of $148.5 million (1.4% beat)

- EPS (non-GAAP): $0.13 vs analyst estimates of $0.12 (9.4% beat)

- Revenue Guidance for Q1 2024 is $149 million at the midpoint, below analyst estimates of $150.8 million

- Management's revenue guidance for the upcoming financial year 2024 is $617 million at the midpoint, missing analyst estimates by 3.8% and implying 10.1% growth (vs 17.3% in FY2023)

- Free Cash Flow of $15.51 million, down 52.3% from the previous quarter

- Gross Margin (GAAP): 78%, down from 80% in the same quarter last year

- Market Capitalization: $2.50 billion

Founded in 2002 by Zach Halmstad and Chip Pearson, right around the time when Apple began to dominate the personal computing market, Jamf (NASDAQ:JAMF) provides software for companies to manage Apple devices such as Macs, iPads, and iPhones.

Apple is known for making user-friendly computing devices and it is not surprising that the demand for its products has grown over the years. As their adoption became widespread across the business and education world, so did the need to manage these devices at scale. Keeping hundreds and thousands of devices up-to-date, with all the necessary apps installed and required level of security enforced can be really time consuming, and if it was to be done manually it would require a large number of IT technicians.

Jamf’s software provides the IT department with an online dashboard where they can see the status of every device, and remotely install updates, apps and security fixes. By providing the tools to make the process of managing Apple products simple and easy, Jamf drives productivity within organizations and also frees up more IT resources that could be deployed to tackle more important problems.

For example, when a public school needed to shift to remote learning, Jamf helped to deploy thousands of iPads and Macs to its students. Instead of the school’s IT team spending weeks manually setting up every device, using Jamf they were able to create a software package and automatically install it on every device within a few hours. It connected students without access to the internet to WiFi hotspots provided by the school, installed remote collaboration apps and provided the students with access to learning materials, ensuring that they were able to continue learning remotely without an interruption.

Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Jamf competes with cross-platform enterprise providers such as VMware (NYSE:VMW) or Microsoft’s Intune (NASDAQ:MSFT) and smaller companies like Addigy and Kandji. Apple is also showing interest in the device management space via its Business Essentials offering targeted at small and medium sized businesses.

Sales Growth

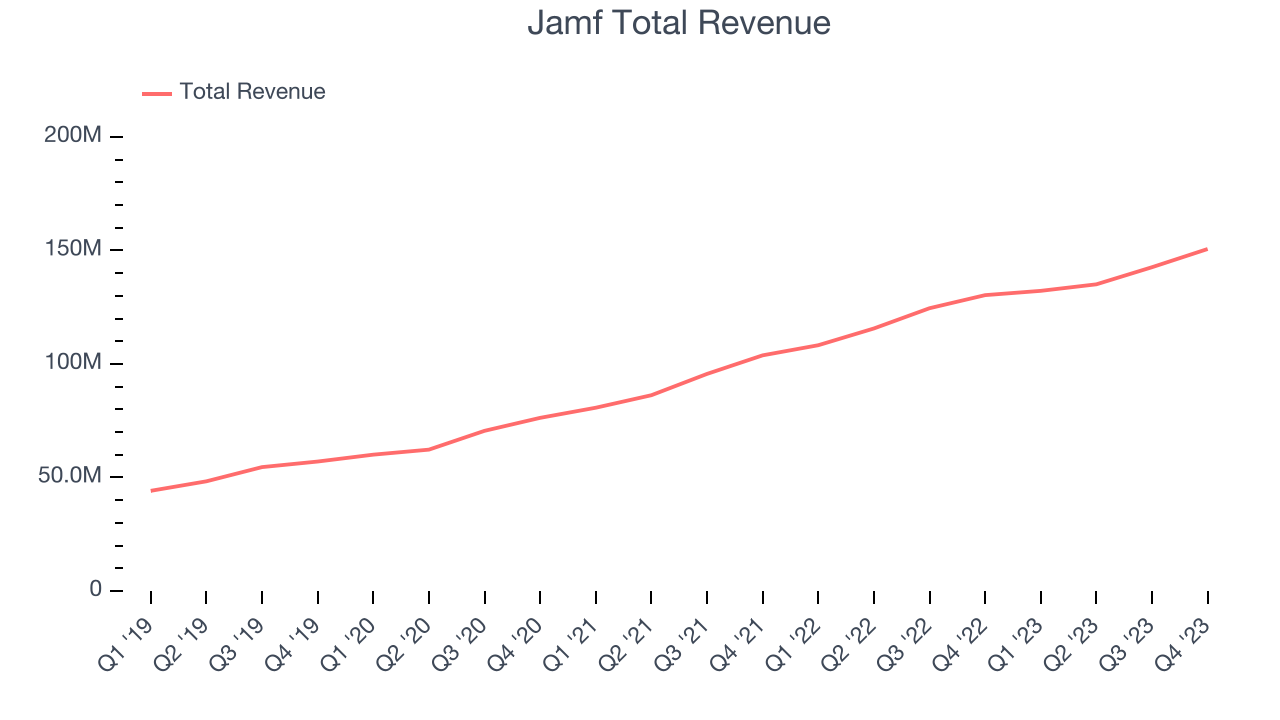

As you can see below, Jamf's revenue growth has been strong over the last two years, growing from $103.8 million in Q4 FY2021 to $150.6 million this quarter.

This quarter, Jamf's quarterly revenue was once again up 15.6% year on year. We can see that Jamf's revenue increased by $8.02 million in Q4, up from $7.54 million in Q3 2023. While we've no doubt some investors were looking for higher growth, it's good to see that quarterly revenue is re-accelerating.

Next quarter's guidance suggests that Jamf is expecting revenue to grow 12.7% year on year to $149 million, slowing down from the 22.1% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $617 million at the midpoint, growing 10.1% year on year compared to the 17.1% increase in FY2023.

Profitability

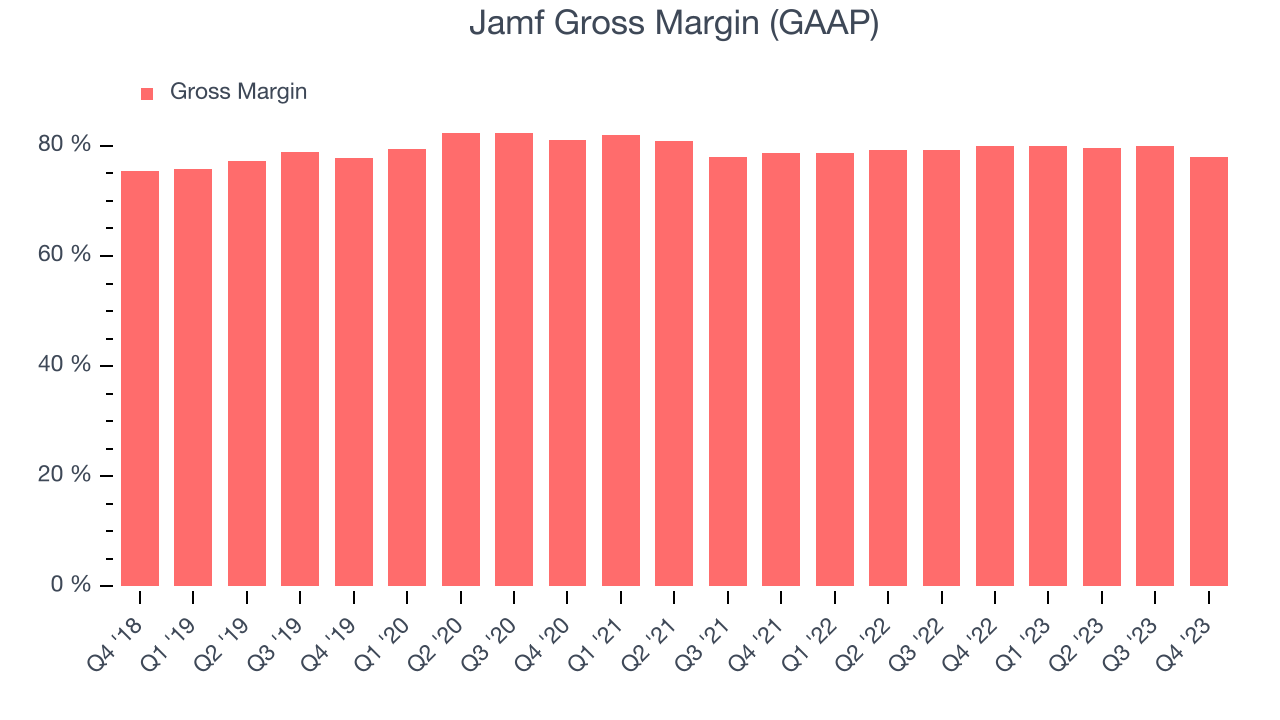

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Jamf's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 78% in Q4.

That means that for every $1 in revenue the company had $0.78 left to spend on developing new products, sales and marketing, and general administrative overhead. Despite its decline over the last year, Jamf's impressive gross margin allows it to fund large investments in product and sales during periods of rapid growth and achieve profitability when reaching maturity.

Cash Is King

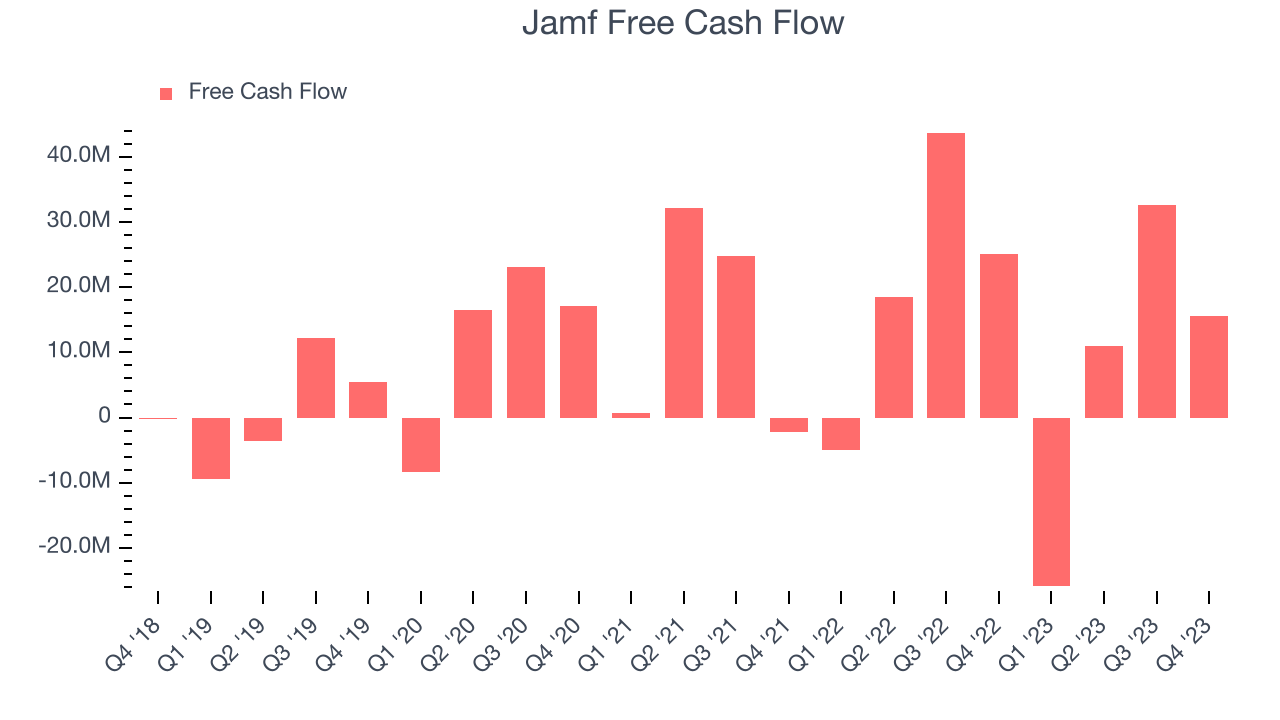

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Jamf's free cash flow came in at $15.51 million in Q4, down 38.2% year on year.

Jamf has generated $33.03 million in free cash flow over the last 12 months, or 5.9% of revenue. This FCF margin enables it to reinvest in its business without depending on the capital markets.

Key Takeaways from Jamf's Q4 Results

It was encouraging to see Jamf narrowly top analysts' revenue expectations this quarter. On the other hand, free cash flow was weaker and its full-year revenue guidance was below estimates and suggests a slowdown in demand. Overall, the results could have been better. The company is down 10.2% on the results and currently trades at $17.9 per share.

Is Now The Time?

When considering an investment in Jamf, investors should take into account its valuation and business qualities as well as what's happened in the latest quarter.

Although we have other favorites, we understand the arguments that Jamf isn't a bad business. We'd expect growth rates to moderate from here, but its . And while its low free cash flow margins give it little breathing room, the good news is its impressive gross margins indicate excellent business economics.

Jamf's price-to-sales ratio based on the next 12 months is 3.9x, suggesting that the market is expecting more moderate growth, relative to the hottest tech stocks. There are things to like about Jamf and there's no doubt it's a bit of a market darling, at least for some. But we are wondering whether there might be better opportunities elsewhere right now.

Wall Street analysts covering the company had a one-year price target of $22.75 per share right before these results (compared to the current share price of $17.90).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.