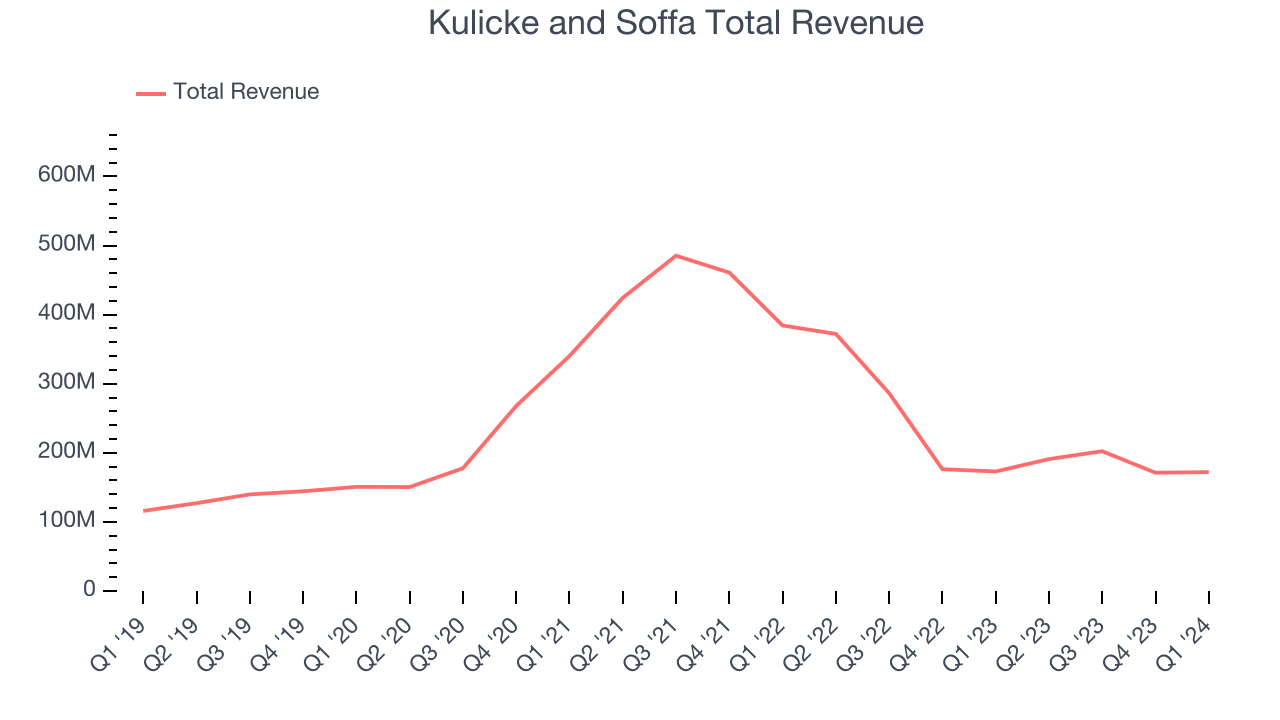

Semiconductor production equipment company Kulicke & Soffa (NASDAQ: KLIC) missed analysts' expectations in Q1 CY2024, with revenue flat year on year at $172.1 million. Next quarter's revenue guidance of $180 million also underwhelmed, coming in 11% below analysts' estimates. It made a non-GAAP loss of $0.95 per share, down from its profit of $0.38 per share in the same quarter last year.

Kulicke and Soffa (KLIC) Q1 CY2024 Highlights:

- Revenue: $172.1 million vs analyst estimates of $174.2 million (1.2% miss)

- EPS (non-GAAP): -$0.95 vs analyst estimates of $0.24 (-$1.19 miss)

- Revenue Guidance for Q2 CY2024 is $180 million at the midpoint, below analyst estimates of $202.3 million

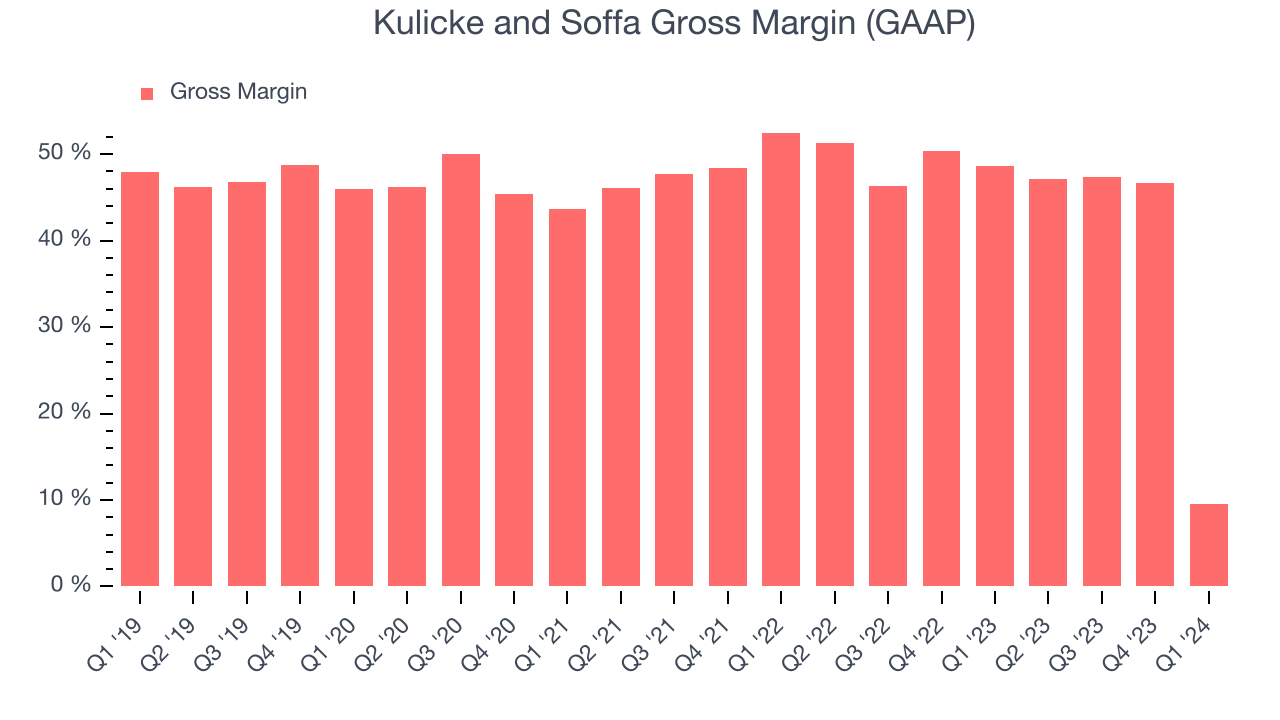

- Gross Margin (GAAP): 9.6%, down from 48.6% in the same quarter last year

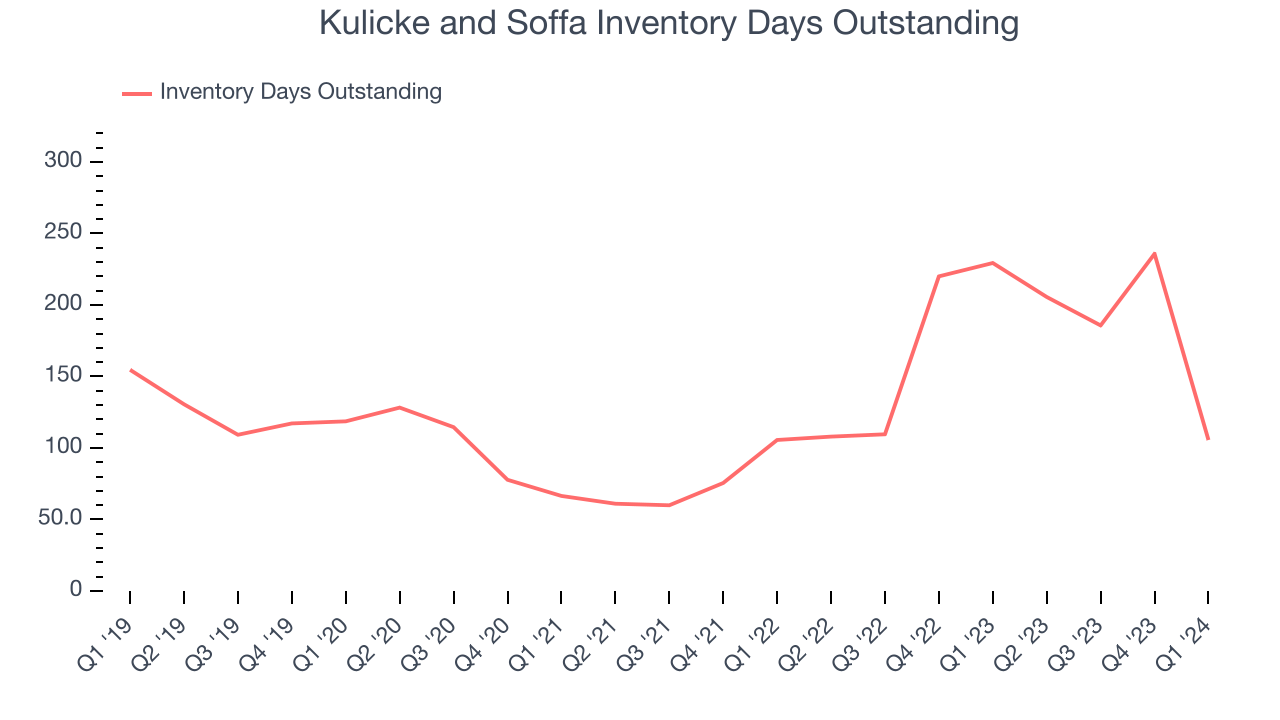

- Inventory Days Outstanding: 106, down from 236 in the previous quarter

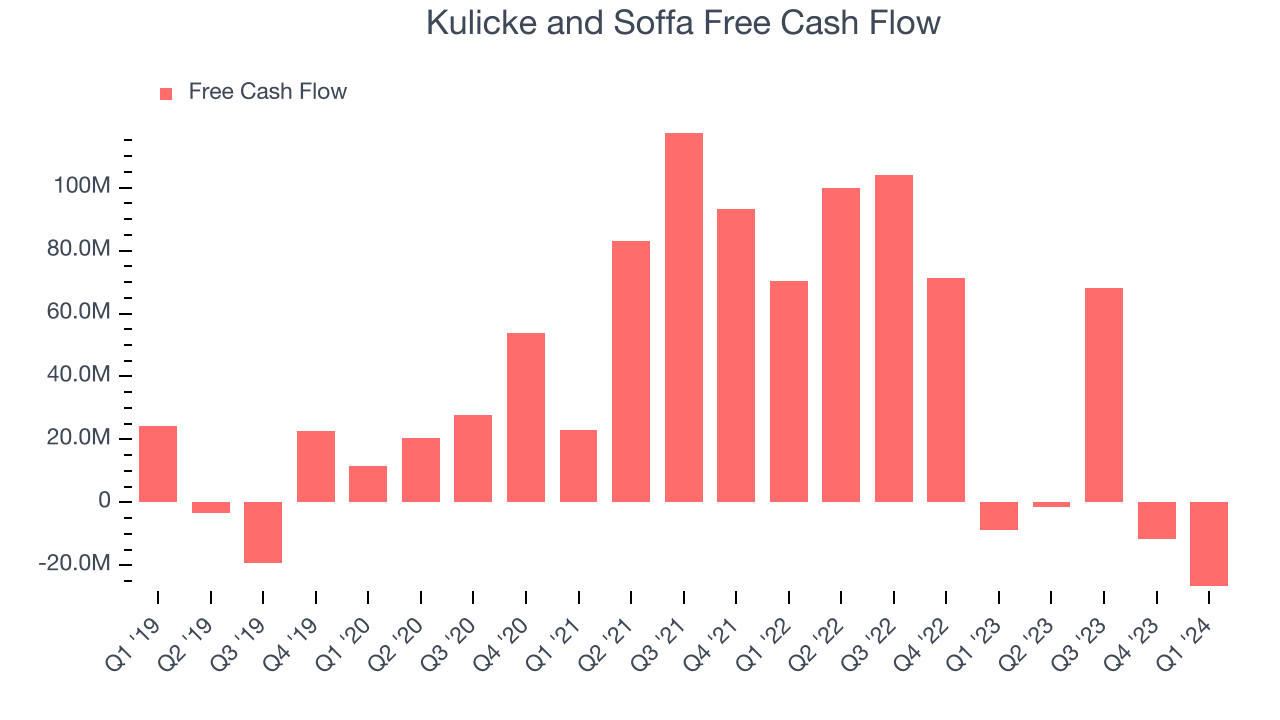

- Free Cash Flow was -$26.72 million compared to -$11.76 million in the previous quarter

- Market Capitalization: $2.61 billion

Headquartered in Singapore, Kulicke & Soffa (NASDAQ: KLIC) is a provider of production equipment and tools used to assemble semiconductor devices

Kulicke & Soffa was founded in 1951 by Frederick Kulicke Jr. and Albert Soffa, and the company was incorporated in 1956. With a 1971 NASDAQ listing, Kulicke & Soffa became one of the first technology companies on the exchange.

The company’s key products are equipment and tools used in the interconnect processes of semiconductor manufacturing. The interconnect process is the wiring system that connects transistors and other components on a chip. This step in manufacturing is important because these connections can be a limiting factor to chip performance, as electrical resistance of wires increases as they are made smaller and thinner to accommodate more transistors.

KLIC’s products therefore aim to improve performance and increase power efficiency amid smaller form factors. One example is the company’s ball bonder, which enables precise electrical interconnections between a bare silicon die and the lead frame of the package it is placed in during semiconductor fabrication. Another example is the company’s wedge bonder, which uses ultrasonic power and force to form resilient bonds.

Competitors offering semiconductor equipment and packaging materials products include ASM Pacific Technology (SEHK:522), BE Semiconductor Industries (ENXTAM:BESI), and Hanwha Precision Machinery.Sales Growth

Kulicke and Soffa's revenue growth over the last three years has been mediocre, averaging 15.7% annually. But as you can see below, its revenue declined from $173 million in the same quarter last year to $172.1 million. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Kulicke and Soffa had a difficult quarter as revenue dropped 0.5% year on year, missing analysts' estimates by 1.2%. This could mean that the current downcycle is deepening.

Kulicke and Soffa may be headed for an upturn. Although the company is guiding for a year-on-year revenue decline of 5.7% next quarter, analysts are expecting revenue to grow 19.5% over the next 12 months.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Kulicke and Soffa's DIO came in at 106, which is 23 days below its five-year average. At the moment, these numbers show no indication of an excessive inventory buildup.

Pricing Power

In the semiconductor industry, a company's gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor. Kulicke and Soffa's gross profit margin, which shows how much money the company gets to keep after paying key materials, input, and manufacturing costs, came in at 9.6% in Q1, down 39 percentage points year on year.

Kulicke and Soffa's gross margins have been trending down over the last 12 months, averaging 38.3%. This weakness isn't great as Kulicke and Soffa's margins are already far below other semiconductor companies and suggest shrinking pricing power and loose cost controls.

Profitability

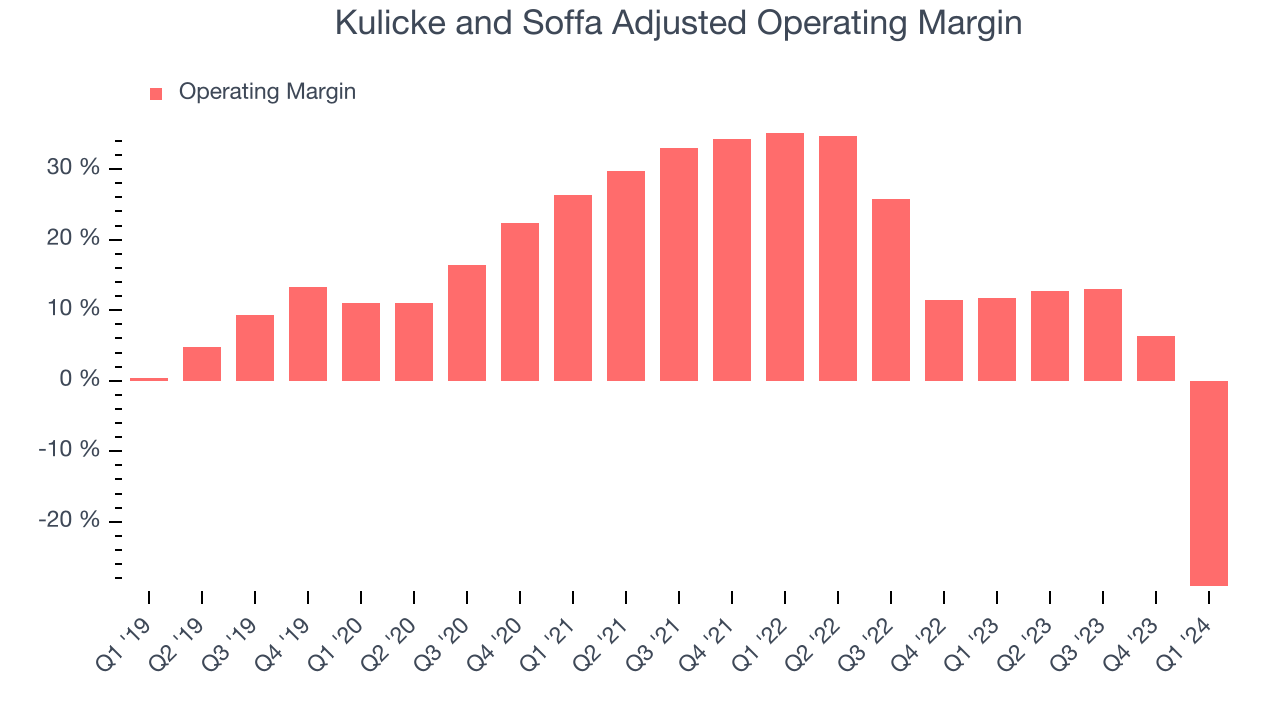

Kulicke and Soffa reported an operating margin of negative 29.2% in Q1, down 41 percentage points year on year. Operating margins are one of the best measures of profitability because they tell us how much money a company takes home after manufacturing its products, marketing and selling them, and, importantly, keeping them relevant through research and development.

Kulicke and Soffa's operating margins have been trending down over the last year, averaging 1.5%. This is a bad sign for Kulicke and Soffa, whose margins are already below average for semiconductor companies. To its credit, however, the company's margins suggest modest pricing power and cost controls.

Earnings, Cash & Competitive Moat

Analysts covering Kulicke and Soffa expect earnings per share to grow 65.7% over the next 12 months, although estimates will likely change after earnings.

Although earnings are important, we believe cash is king because you can't use accounting profits to pay the bills. Kulicke and Soffa's free cash flow came in at negative $26.72 million in Q1, down 203% year on year.

Kulicke and Soffa has generated $28.1 million in free cash flow over the last 12 months, or 3.8% of revenue. This FCF margin enables it to reinvest in its business without depending on the capital markets.

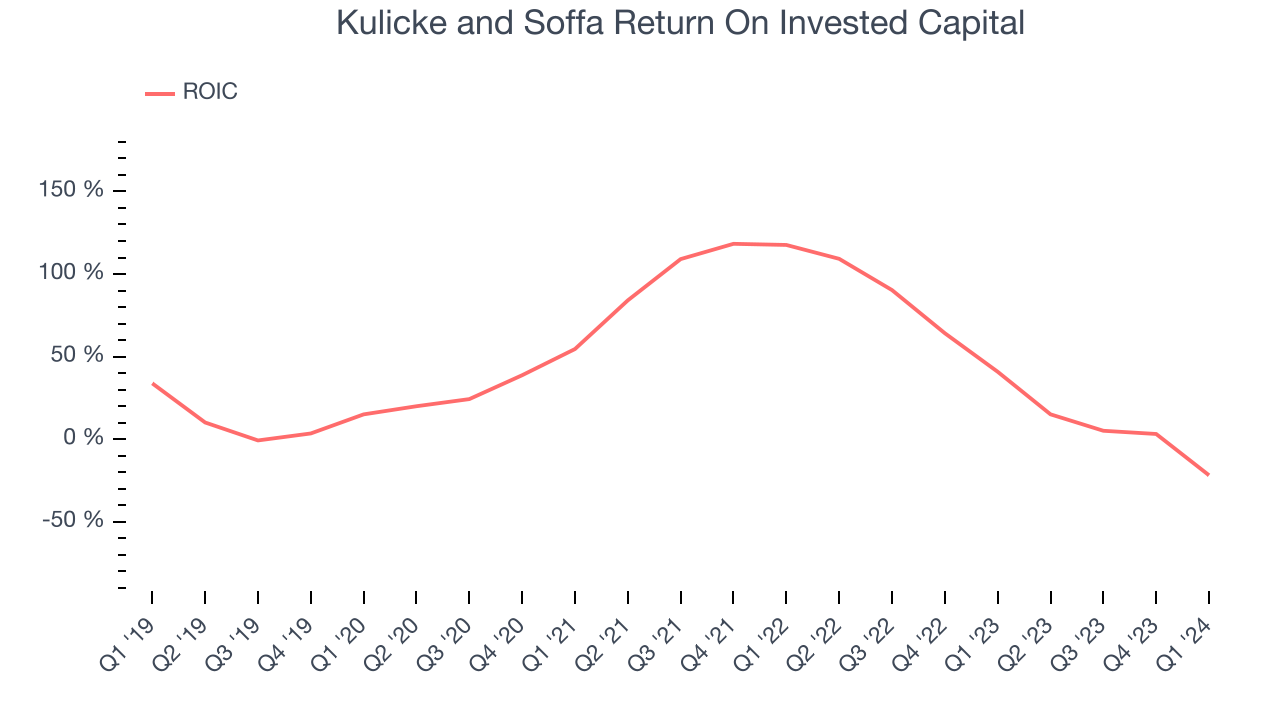

Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit a company makes compared to how much money the business raised (debt and equity).

Kulicke and Soffa's five-year average ROIC was 22.2%, slightly better than the broader sector. Just as you’d like your investment dollars to generate returns, Kulicke and Soffa's invested capital has produced decent profits.

The trend in its ROIC, however, is often what surprises the market and drives the stock price. Unfortunately, Kulicke and Soffa's ROIC significantly decreased over the last few years. We like what management has done historically but are concerned its ROIC is declining, perhaps a symptom of waning business opportunities to invest profitably.

Key Takeaways from Kulicke and Soffa's Q1 Results

We were impressed by Kulicke and Soffa's strong improvement in inventory levels. On the other hand, its revenue guidance for next quarter missed analysts' expectations and its revenue missed Wall Street's estimates. Overall, this was a mixed quarter for Kulicke and Soffa. The company is down 4% on the results and currently trades at $42.5 per share.

Is Now The Time?

Kulicke and Soffa may have had a bad quarter, but investors should also consider its valuation and business qualities when assessing the investment opportunity.

We cheer for everyone who's making the lives of others easier through technology, but in the case of Kulicke and Soffa, we'll be cheering from the sidelines. Although its revenue growth has been solid over the last three years, Wall Street expects growth to deteriorate from here. And while its above-average ROIC suggests its management team has made good investment decisions in the past, the downside is its operating margins reveal subpar cost controls compared to other semiconductor businesses. On top of that, its low free cash flow margins give it little breathing room.

Kulicke and Soffa's price-to-earnings ratio based on the next 12 months is 19.2x. While there are some things to like about Kulicke and Soffa and its valuation is reasonable, we think there are better opportunities elsewhere in the market right now.

Wall Street analysts covering the company had a one-year price target of $57.48 per share right before these results (compared to the current share price of $42.50).

To get the best start with StockStory check out our most recent Stock picks, and then sign up to our earnings alerts by adding companies to your watchlist here. We typically have the quarterly earnings results analyzed within seconds of the data being released, and especially for the companies reporting pre-market, this often gives investors the chance to react to the results before the market has fully absorbed the information.